Enlarge image

2022 WEST VIRGINIA CORPORATION NET INCOME TAX

Enlarge image | 2022 WEST VIRGINIA CORPORATION NET INCOME TAX |

Enlarge image |

C ONTENTS

IMPORTANT INFORMATION FOR 2022 3

TAX RATES 3

RETURNED PAYMENT CHARGE 3

TAXPAYER RESPONSIBILITIES 4

FILING YOUR CORPORATE RETURNS 4

PAYMENT OF THE TAX 4

REFUNDS 4

SELLING OR DISCONTINUING YOUR BUSINESS 4

GENERAL INFORMATION 5

ASSISTANCE 5

CORPORATION NET INCOME TAX 5

EXEMPT ORGANIZATIONS 5

PAYMENT OF TAX 5

EXTENSION OF TIME TO FILE 6

WHERE TO FILE 6

ESTIMATED TAXES 6

RETURN CHANGES 6

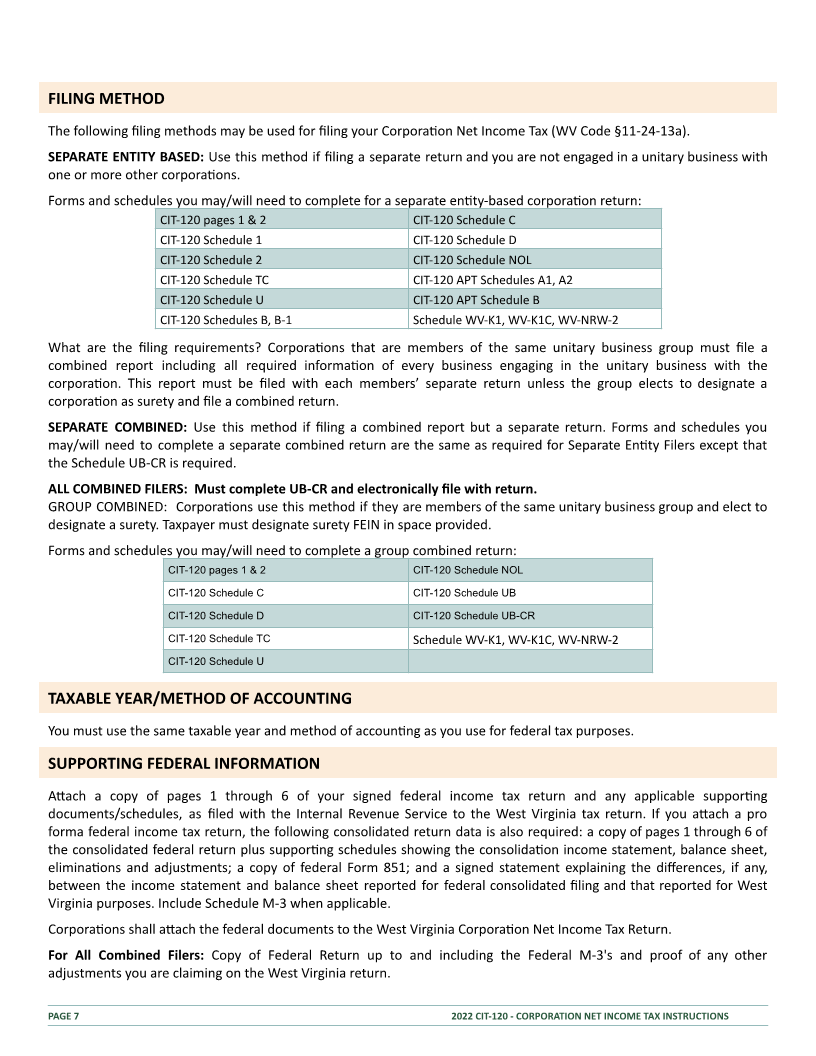

FILING METHOD 7

TAXABLE YEAR/METHOD OF ACCOUNTING 7

SUPPORTING FEDERAL INFORMATION 7

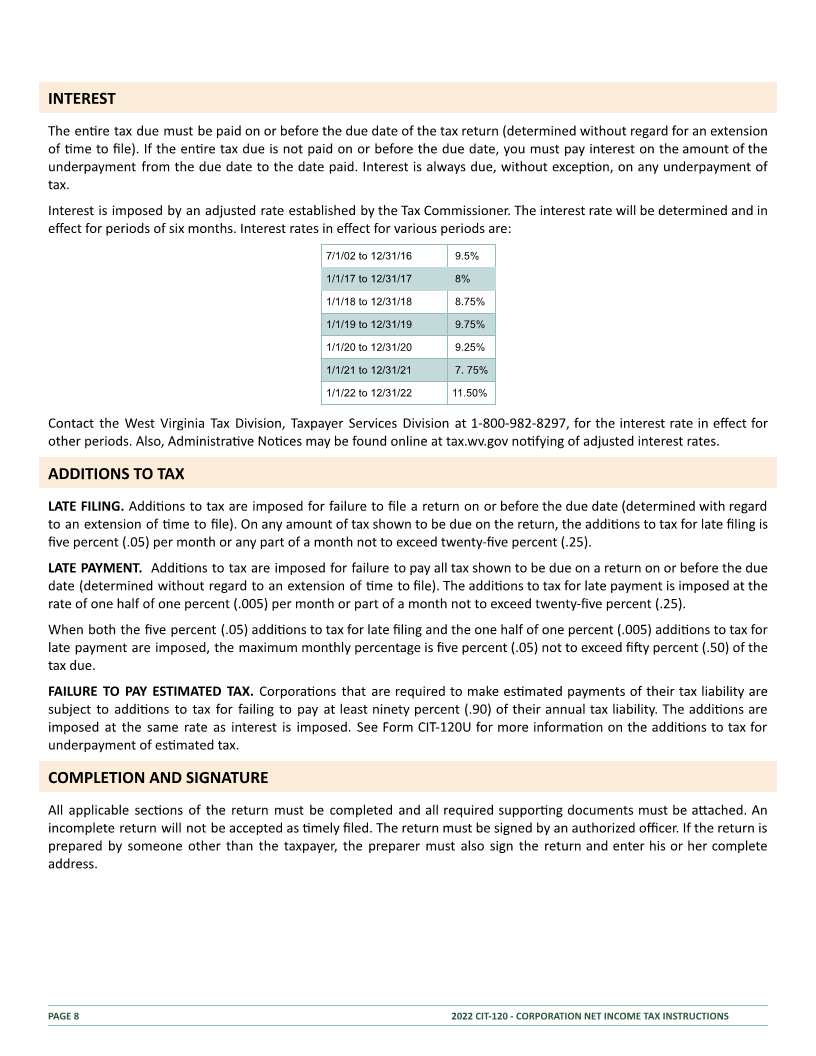

INTEREST 8

ADDITIONS TO TAX 8

COMPLETION AND SIGNATURE 8

CHANGES MADE BY THE IRS TO FEDERAL RETURN 9

CORPORATE AMENDED RETURNS 9

CONSISTENCY IN REPORTING 9

CONFIDENTIAL INFORMATION 9

REPORTING WEST VIRGINIA INCOME TAX WITHHOLDING CREDIT 1 0

FORM CIT-120 INSTRUCTIONS 1 1

SCHEDULE 1–SEPARATE ENTITY FILER WEST VIRGINIA CORPORATIONS WHOLLY IN WV 13

SCHEDULE 2 – SEPARATE ENTITY FILER WITH MULTISTATE ACTIVITY 1 2

CIT-120, PAGE 2 1 3

SCHEDULE B: ADJUSTMENTS TO FEDERAL TAXABLE INCOME 1 4

SCHEDULE B-1 ALLOWANCE FOR GOVERNMENTAL OBLIGATIONS/

OBLIGATIONS SECURED BY RESIDENTIAL PROPERTY (§ 11-24-6 (f)) 1 6

SCHEDULE C – SCHEDULE OF TAX PAYMENTS 1 6

SCHEDULE D – REPORTABLE ENTITIES 1 6

CIT-120TC: SUMMARY OF CORPORATION NET INCOME TAX CREDITS 1 7

SCHEDULE NOL: WV NET OPERATING LOSS CARRYFORWARD CALCULATION (§11-24-6(d)) 1 7

CIT-120 APT – ALLOCATION AND APPORTIONMENT FOR MULTISTATE CORPORATIONS 19

CIT-120U 2 4

COMBINED REPORTING 2 6

C OVER P HOTO P HOTOGRAPH BY K ASEY B AILES

PAGE 2 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

IMPORTANT INFORMATION FOR 2022

For periods beginning on or a er January 1, 2022, annual returns will have a due date of April 18, 2023 and an extended

due date of October 15, 2023. Fiscal and 52/53-week returns will be due on the 15th day of the fourth month following

the end of the period with an extension period of six months.

TAX RATES

● The Corpora on Net Income Tax Rate is 6.5% (§11-24-4).

● Effec ve January 1, 2019, taxpayers who had annual remi ance of any single tax equal to or greater than

$50,000 during the fiscal year are required to electronically file returns and make payments using Electronic

Funds Transfer (EFT) for periods beginning on or a er January 1.

● Failure to comply with the requirement to remit payments by EFT without first obtaining a waiver may result in

a civil penalty of three (3) percent of each payment which was to be paid by EFT. Visit our website

www.tax.wv.gov for addi onal informa on.

RETURNED PAYMENT CHARGE

The Tax Department will recover a $15.00 fee associated with any returned bank transac ons. These bank transac ons

include but are not limited to the following:

● Direct Debit (payment) transac ons returned for insufficient funds.

● Stopped payments.

● Bank refusal to authorize payment for any reason.

● Direct Deposit of refunds to closed accounts.

● Direct Deposit of refunds to accounts containing inaccurate or illegible account informa on.

Checks returned for insufficient funds will incur a $28.00 fee.

The fee charged for returned or rejected payments will be to recover only the amount charged to the Tax Division by

the financial ins tu ons.

Important : There are steps that can be taken to minimize the likelihood of a rejected financial transac on occurring:

● Be sure that you are using the most current bank rou ng and account informa on.

● If you have your tax return professionally prepared, the financial informa on used from a prior year return

o en pre-populates the current return as a step saver. It is important that you verify this informa on with your

tax preparer by reviewing the bank rou ng and account informa on from a current check. This will ensure the

informa on is accurate and current in the event that a bank account previously used was closed or changed

either by you or the financial ins tu on.

● If you prepare your tax return at home using tax prepara on so ware, the financial informa on used from a

prior year return o en pre-populates the current return as a step saver. It is important that you verify this

informa on by reviewing the bank rou ng and account informa on from a current check. This will ensure the

informa on is accurate and current in the event that a bank account previously used was closed or changed

either by you or the financial ins tu on.

● If you prepare your tax return by hand using a paper return, be sure that all numbers reques ng a direct

deposit of refund entered are clear and legible.

● If making a payment using MyTaxes, be sure that the bank rou ng and account number being used is current.

● If scheduling a delayed debit payment for an electronic return filed prior to the due date, make sure that the

bank rou ng and account number being used will be ac ve on the scheduled date.

● Be sure that funds are available in your bank account to cover the payment when checks or delayed debit

payments are presented for payment.

PAGE 3 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image | TAXPAYER RESPONSIBILITIES FILING YOUR CORPORATE RETURNS Returns should be filed by the due date. You may obtain forms by calling 1-800-982-8297. Forms may also be obtained from any of our regional field offices or from the Tax Division website at tax.wv.gov. Failure to file returns will result in your account being referred to our Compliance Division for correc ve ac on. Please file all required tax returns even if you owe no tax for the repor ng period. All applicable pages of the return must be filed. PAYMENT OF THE TAX The full amount of tax owed is due and payable on the original due date of the tax return. Failure to pay the full amount of tax by the due date will result in interest and penal es being added to any unpaid amount of tax. If you are unable to pay the full amount of tax on the due date, you should file your tax return along with a wri en explana on of why you are unable to pay and when you will pay the tax due. REFUNDS You are en tled to a refund of any amount that you overpaid. All or part of any overpayment may be applied as a credit against your liability for such tax for other periods. A claim for refund (usually a tax return showing an overpayment) must be filed within three years of the due date of the return or two years from the date the tax was paid, whichever expires later. The overpayment will be used by the Tax Department against other tax liabili es due. If the Tax Department does not respond to your request within six months of the due date or the extended due date on overpayment of Corpora on Net Income Tax, you may submit in wri ng a request for an administra ve hearing to present your reasons why you feel you are en tled to the refund. Interest is allowed and paid on any refund upon which the Department has failed to mely act and which is final and conclusive. If the Tax Department denies or reduces a request for a refund, a wri en request for an administra ve hearing may be submi ed. Failure to respond to a denial or reduc on within sixty days will result in the denial/reduc on becoming final and conclusive and not subject to further administra ve or judicial review. SELLING OR DISCONTINUING YOUR BUSINESS If you sell or discon nue your business, no fy the Tax Department in wri ng as soon as possible a er your business is sold or discon nued. All final tax returns should be filed. PAGE 4 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS |

Enlarge image | GENERAL INFORMATION The informa on in this booklet is for calendar year 2022 returns and for fiscal year returns beginning in 2022 and ending in 2023. The informa on in this book is intended to help you complete your returns and is not a subs tute for tax laws and regula ons. Star ng in tax year 2020, the forms have been redesignated, changing “CNF” to “CIT”. ASSISTANCE Address ques ons to the West Virginia Tax Division, Taxpayer Services, PO Box 3784, Charleston, WV 25337-3784 or by telephone at (304) 558-3333, toll free at 1-800-982-8297. CORPORATION NET INCOME TAX The Corpora on Net Income Tax is a tax on the West Virginia taxable income of every domes c or foreign corpora on which enjoys the benefits and protec ons of the government and laws in the State of West Virginia or derives income from property, ac vity or other sources in West Virginia. The term “corpora on” includes a joint stock company and any associa on or other organiza on which is taxable as a corpora on under federal income tax laws. The West Virginia Corpora on Net Income Tax is a federal conformity tax in that the star ng point in compu ng West Virginia taxable income is the federal taxable income of the corpora on. Certain increasing and decreasing adjustments, as required by state law, must be made to federal taxable income to arrive at West Virginia taxable income. Corpora ons are required to allocate certain types of nonbusiness income to West Virginia and appor on their remaining income. The Corpora on Net Income Tax rate is six and one-half percent (.065). EXEMPT ORGANIZATIONS Any corpora on exempt from federal income tax is also exempt from West Virginia Corpora on Net Income Tax. In addi on, certain insurance companies, certain produc on credit associa ons, trusts established under 29 U.S.C. 186, and other organiza ons specifically exempt under the laws of West Virginia are also exempt. If you are a tax-exempt organiza on with unrelated business income that is subject to federal tax, you must pay the West Virginia Corpora on Net Income Tax. PAYMENT OF TAX DUE DATE: A corpora on’s annual West Virginia Corpora on Net Income Tax Return is due on or before the 15th day of the fourth month a er the close of the taxable year. The filing of returns is required whether any tax is due. A tax-exempt organiza on’s annual West Virginia Corpora on Net Income Tax Return is due on or before the 15th day of the fi h month a er the close of the taxable year. Make your remi ance payable to the West Virginia Tax Division. PAYMENT OPTIONS: Effec ve January 1, 2022, taxpayers who had annual remi ance of any single tax equal or greater than $50,000 during calendar year 2020 or fiscal year 2019 are required to electronically file returns and make payments using Electronic Funds Transfer (EFT) for periods beginning on or a er January 1, 2022. Returns filed with a balance due may use any of the following payment op ons: Check or Money Order made payable to the West Virginia Tax Division, Electronic Funds Transfer or Payment by Credit Card. Visit tax.wv.gov for addi onal payment informa on. Return Filer's filing as a Combined Separate or Combined Group must pay with EFT to the Surety account not to each separate member within the group. PAGE 5 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS |

Enlarge image |

EXTENSION OF TIME TO FILE

An extension of me to file a federal return is automa cally accepted by West Virginia as an extension of me to file the

West Virginia return. A copy of the federal extension form must be a ached to the West Virginia return when filed and

the extended due date must be entered on top of the return. Returns filed a er the due date, without suppor ng

documents and extended due date entered on the top of the return, will be processed as late filed and interest and

penal es will be assessed.

A state extension of me to file may be obtained, even if a federal extension has not been requested. An extension of

me to file does not extend the me for payment of any tax due. If you have an extension of me to file, payment of any

tax due may be made by filing a West Virginia extension form (see instruc ons for Form CIT-120EXT). To avoid interest

and penal es, payment must be received on or before the due date of the return.

WHERE TO FILE

West Virginia Tax Division

Tax Account Administra on

Corporate Tax Unit

PO Box 1202

Charleston, WV 25324-1202

ESTIMATED TAXES

Es mated Corpora on Net Income Tax payments are required for any corpora on which can reasonably expect its West

Virginia taxable income to be more than $10,000 (which equals a tax liability a er tax credits of more than $650) and are

due in four equal installments on the 15th day of the fourth, sixth, ninth, and twel h months of the tax year.

RETURN CHANGES

The following Schedules are new or have been updated in the 2022 tax period:

● Revised – UB-CR

● New Credits added to CIT-120TC

PAGE 6 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

FILING METHOD

The following filing methods may be used for filing your Corpora on Net Income Tax (WV Code §11-24-13a).

SEPARATE ENTITY BASED: Use this method if filing a separate return and you are not engaged in a unitary business with

one or more other corpora ons.

Forms and schedules you may/will need to complete for a separate en ty-based corpora on return:

CIT-120 pages 1 & 2 CIT-120 Schedule C

CIT-120 Schedule 1 CIT-120 Schedule D

CIT-120 Schedule 2 CIT-120 Schedule NOL

CIT-120 Schedule TC CIT-120 APT Schedules A1, A2

CIT-120 Schedule U CIT-120 APT Schedule B

CIT-120 Schedules B, B-1 Schedule WV-K1, WV-K1C, WV-NRW-2

What are the filing requirements? Corpora ons that are members of the same unitary business group must file a

combined report including all required informa on of every business engaging in the unitary business with the

corpora on. This report must be filed with each members’ separate return unless the group elects to designate a

corpora on as surety and file a combined return.

SEPARATE COMBINED: Use this method if filing a combined report but a separate return. Forms and schedules you

may/will need to complete a separate combined return are the same as required for Separate En ty Filers except that

the Schedule UB-CR is required.

ALL COMBINED FILERS: Must complete UB-CR and electronically file with return.

GROUP COMBINED: Corpora ons use this method if they are members of the same unitary business group and elect to

designate a surety. Taxpayer must designate surety FEIN in space provided.

Forms and schedules you may/will need to complete a group combined return:

CIT-120 pages 1 & 2 CIT-120 Schedule NOL

CIT-120 Schedule C CIT-120 Schedule UB

CIT-120 Schedule D CIT-120 Schedule UB-CR

CIT-120 Schedule TC Schedule WV-K1, WV-K1C, WV-NRW-2

CIT-120 Schedule U

TAXABLE YEAR/METHOD OF ACCOUNTING

You must use the same taxable year and method of accoun ng as you use for federal tax purposes.

SUPPORTING FEDERAL INFORMATION

A ach a copy of pages 1 through 6 of your signed federal income tax return and any applicable suppor ng

documents/schedules, as filed with the Internal Revenue Service to the West Virginia tax return. If you a ach a pro

forma federal income tax return, the following consolidated return data is also required: a copy of pages 1 through 6 of

the consolidated federal return plus suppor ng schedules showing the consolida on income statement, balance sheet,

elimina ons and adjustments; a copy of federal Form 851; and a signed statement explaining the differences, if any,

between the income statement and balance sheet reported for federal consolidated filing and that reported for West

Virginia purposes. Include Schedule M-3 when applicable.

Corpora ons shall a ach the federal documents to the West Virginia Corpora on Net Income Tax Return.

For All Combined Filers: Copy of Federal Return up to and including the Federal M-3's and proof of any other

adjustments you are claiming on the West Virginia return.

PAGE 7 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

INTEREST

The en re tax due must be paid on or before the due date of the tax return (determined without regard for an extension

of me to file). If the en re tax due is not paid on or before the due date, you must pay interest on the amount of the

underpayment from the due date to the date paid. Interest is always due, without excep on, on any underpayment of

tax.

Interest is imposed by an adjusted rate established by the Tax Commissioner. The interest rate will be determined and in

effect for periods of six months. Interest rates in effect for various periods are:

7/1/02 to 12/31/16 9.5%

1/1/17 to 12/31/17 8%

1/1/18 to 12/31/18 8.75%

1/1/19 to 12/31/19 9.75%

1/1/20 to 12/31/20 9.25%

1/1/21 to 12/31/21 7. 75%

1/1/22 to 12/31/22 11.50%

Contact the West Virginia Tax Division, Taxpayer Services Division at 1-800-982-8297, for the interest rate in effect for

other periods. Also, Administra ve No ces may be found online at tax.wv.gov no fying of adjusted interest rates.

ADDITIONS TO TAX

LATE FILING. Addi ons to tax are imposed for failure to file a return on or before the due date (determined with regard

to an extension of me to file). On any amount of tax shown to be due on the return, the addi ons to tax for late filing is

five percent (.05) per month or any part of a month not to exceed twenty-five percent (.25).

LATE PAYMENT. Addi ons to tax are imposed for failure to pay all tax shown to be due on a return on or before the due

date (determined without regard to an extension of me to file). The addi ons to tax for late payment is imposed at the

rate of one half of one percent (.005) per month or part of a month not to exceed twenty-five percent (.25).

When both the five percent (.05) addi ons to tax for late filing and the one half of one percent (.005) addi ons to tax for

late payment are imposed, the maximum monthly percentage is five percent (.05) not to exceed fi y percent (.50) of the

tax due.

FAILURE TO PAY ESTIMATED TAX. Corpora ons that are required to make es mated payments of their tax liability are

subject to addi ons to tax for failing to pay at least ninety percent (.90) of their annual tax liability. The addi ons are

imposed at the same rate as interest is imposed. See Form CIT-120U for more informa on on the addi ons to tax for

underpayment of es mated tax.

COMPLETION AND SIGNATURE

All applicable sec ons of the return must be completed and all required suppor ng documents must be a ached. An

incomplete return will not be accepted as mely filed. The return must be signed by an authorized officer. If the return is

prepared by someone other than the taxpayer, the preparer must also sign the return and enter his or her complete

address.

PAGE 8 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

CHANGES MADE BY THE IRS TO FEDERAL RETURN

Any corpora on whose reported income or deduc ons are changed or corrected by the Internal Revenue Service or

through renego a on of a contract with the United States is required to report the change or correc on to the West

Virginia Tax Division. This report must be made within ninety days of the final determina on by filing an amended/RAR

return and a aching a copy of the revenue agent’s report detailing such adjustments.

For All Combined Filers: Amended/ RAR Returns MUST be E-Filed and a Complete new return with all new schedules, a

copy of the prior return is not required.

CORPORATE AMENDED RETURNS

A corpora on that filed an amended return with the Internal Revenue Service must file an amended return with the

West Virginia Tax Division within ninety days of filing the amended federal return.

● File Form CIT-120, pages 1 and 2, comple ng all appropriate lines and checking the Amended box under

“Return Type” on page 1. Because WV uses barcodes on tax forms it is important to use the appropriate forms

for the tax year being amended.

Example : If amending a tax return for the period ending 12-31-2018; use the 2018 CNF-120 forms.

Note: Tax forms for different years may use different line numbers; read the line instruc ons carefully.

● If you received a refund, or had an amount credited on the original return, enter that amount on Line 14 of

Form CIT-120, page 2. For 2022, years prior to 2020 should file CNF-120, and enter any refund or amount

credited on line 14, page 2.

● A ach all schedules that have amended figures in order to verify the changes made to the return.

Example: There was a change made to your Adjustments to Federal Taxable Income; be sure to a ach

Schedule B with the amended figures.

Amended Returns filed for the purpose of obtaining a refund of an overpayment must be filed within three years of the

due date of the return (with regard to an extension of me to file), or two years from the date the tax was paid,

whichever expires later. If your Amended Return has a balance due, send the payment along with the tax return.

CONSISTENCY IN REPORTING

In comple ng your West Virginia Corpora on Net Income Tax Return, if you depart from or modify past procedures for

classifying business income and nonbusiness income, valuing property or including or excluding property in the property

factor, trea ng compensa on paid in the payroll factor, including or excluding gross receipts in the sales factor, you must

disclose by a aching a separates schedule detailing the nature and extent of the variances or modifica ons.

If a corpora on makes sales of tangible personal property which are shipped into a state in which the corpora on is not

taxable, you must iden fy the state to which the property is shipped and report the total amount of sales assigned to

such state.

CONFIDENTIAL INFORMATION

Tax informa on which is disclosed to the West Virginia Tax Division, whether through returns or through department

inves ga on, is held in strict confidence by law. The Tax Division, the United States Internal Revenue Service and other

states have agreements under which tax informa on is exchanged. This is to verify the accuracy and consistency of

informa on reported on federal, other state, and West Virginia tax returns.

PAGE 9 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image | REPORTING WEST VIRGINIA INCOME TAX WITHHOLDING CREDIT A West Virginia Income Tax Withholding Credit is created when a payment is made by another en ty for the benefit of the Corpora on filing this return. ELECTRONIC FILED RETURNS If you are claiming a withholding credit you must submit Form WVK-1C, WVK-1, NRW-2, or 1099 as part of your electronic return. Only electronically submi ed data is acceptable. No PDF a achments will be accepted for claiming a withholding credit. These documents will be used to verify the withholding credits claimed on your return. If withholding is claimed as a result of the Nonresident Sale of Real Estate, the form WV/NRSR and all suppor ng documenta on should be on file with the Tax Division prior to filing the CIT-120. No PDF a achments will be accepted for claiming a NRSR withholding credit. Failure to file the required WV/NRSR, federal Schedule D and other suppor ng documents prior to filing the CIT-120 will result in return processing delays. PAPER FILED RETURNS Enter the total amount of West Virginia tax withheld on your behalf by another en ty on your return. A completed Form WVK-1C, WVK-1, NRW-2, or 1099 must be enclosed with your paper return. Failure to submit these documents will result in the disallowance of the withholding credit claimed. Note: Local or municipal fees cannot be claimed as West Virginia income tax withheld. If the withholding source is for a nonresident sale of real estate transac on, a form WV/NRSR must be completed and on file with the Tax Division prior to submi ng a tax return. Addi onally, a Federal Schedule D must be submi ed. If withholdings are related to form WV/NRSR, please indicate in the box provided on line 12. PAGE 10 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS |

Enlarge image |

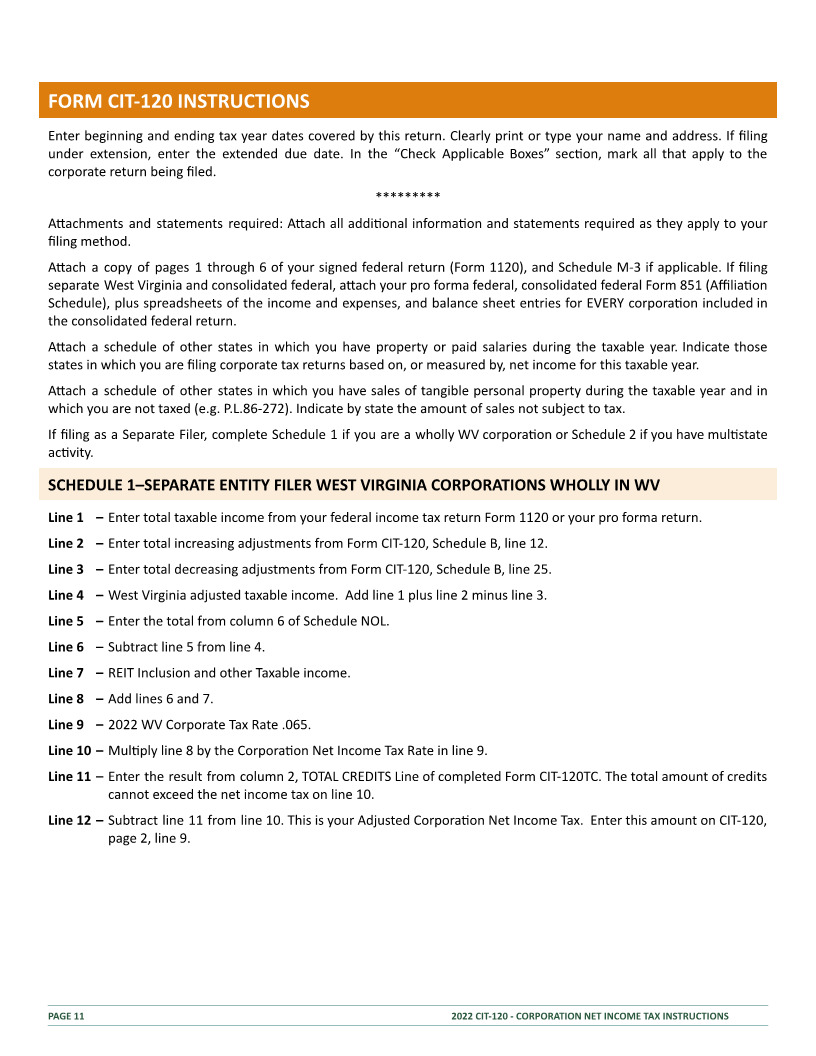

FORM CIT-120 INSTRUCTIONS

Enter beginning and ending tax year dates covered by this return. Clearly print or type your name and address. If filing

under extension, enter the extended due date. In the “Check Applicable Boxes” sec on, mark all that apply to the

corporate return being filed.

*********

A achments and statements required: A ach all addi onal informa on and statements required as they apply to your

filing method.

A ach a copy of pages 1 through 6 of your signed federal return (Form 1120), and Schedule M-3 if applicable. If filing

separate West Virginia and consolidated federal, a ach your pro forma federal, consolidated federal Form 851 (Affilia on

Schedule), plus spreadsheets of the income and expenses, and balance sheet entries for EVERY corpora on included in

the consolidated federal return.

A ach a schedule of other states in which you have property or paid salaries during the taxable year. Indicate those

states in which you are filing corporate tax returns based on, or measured by, net income for this taxable year.

A ach a schedule of other states in which you have sales of tangible personal property during the taxable year and in

which you are not taxed (e.g. P.L.86-272). Indicate by state the amount of sales not subject to tax.

If filing as a Separate Filer, complete Schedule 1 if you are a wholly WV corpora on or Schedule 2 if you have mul state

ac vity.

SCHEDULE 1–SEPARATE ENTITY FILER WEST VIRGINIA CORPORATIONS WHOLLY IN WV

Line 1 – Enter total taxable income from your federal income tax return Form 1120 or your pro forma return.

Line 2 – Enter total increasing adjustments from Form CIT-120, Schedule B, line 12.

Line 3 – Enter total decreasing adjustments from Form CIT-120, Schedule B, line 25.

Line 4 – West Virginia adjusted taxable income. Add line 1 plus line 2 minus line 3.

Line 5 – Enter the total from column 6 of Schedule NOL.

Line 6 – Subtract line 5 from line 4.

Line 7 – REIT Inclusion and other Taxable income.

Line 8 – Add lines 6 and 7.

Line 9 – 2022 WV Corporate Tax Rate .065.

Line 10 – Mul ply line 8 by the Corpora on Net Income Tax Rate in line 9.

Line 11 – Enter the result from column 2, TOTAL CREDITS Line of completed Form CIT-120TC. The total amount of credits

cannot exceed the net income tax on line 10.

Line 12 – Subtract line 11 from line 10. This is your Adjusted Corpora on Net Income Tax. Enter this amount on CIT-120,

page 2, line 9.

PAGE 11 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

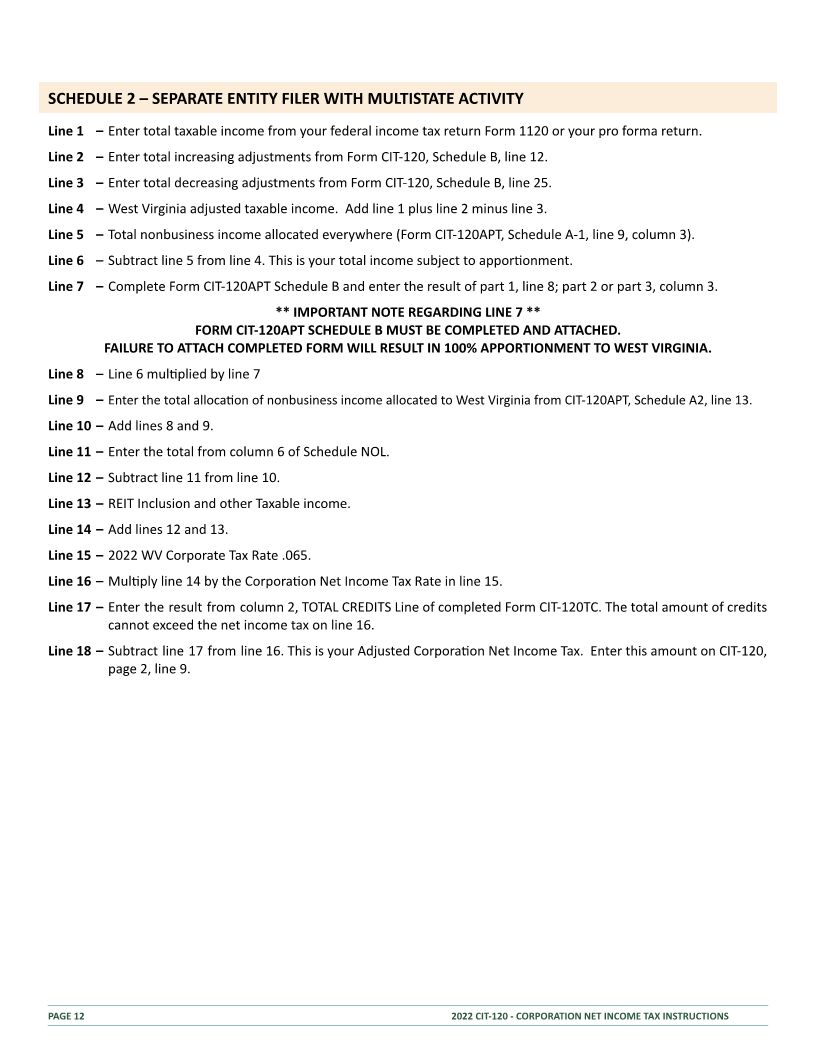

SCHEDULE 2 – SEPARATE ENTITY FILER WITH MULTISTATE ACTIVITY

Line 1 – Enter total taxable income from your federal income tax return Form 1120 or your pro forma return.

Line 2 – Enter total increasing adjustments from Form CIT-120, Schedule B, line 12.

Line 3 – Enter total decreasing adjustments from Form CIT-120, Schedule B, line 25.

Line 4 – West Virginia adjusted taxable income. Add line 1 plus line 2 minus line 3.

Line 5 – Total nonbusiness income allocated everywhere (Form CIT-120APT, Schedule A-1, line 9, column 3).

Line 6 – Subtract line 5 from line 4. This is your total income subject to appor onment.

Line 7 – Complete Form CIT-120APT Schedule B and enter the result of part 1, line 8; part 2 or part 3, column 3.

** IMPORTANT NOTE REGARDING LINE 7 **

FORM CIT-120APT SCHEDULE B MUST BE COMPLETED AND ATTACHED.

FAILURE TO ATTACH COMPLETED FORM WILL RESULT IN 100% APPORTIONMENT TO WEST VIRGINIA.

Line 8 – Line 6 mul plied by line 7

Line 9 – Enter the total alloca on of nonbusiness income allocated to West Virginia from CIT-120APT, Schedule A2, line 13.

Line 10 – Add lines 8 and 9.

Line 11 – Enter the total from column 6 of Schedule NOL.

Line 12 – Subtract line 11 from line 10.

Line 13 – REIT Inclusion and other Taxable income.

Line 14 – Add lines 12 and 13.

Line 15 – 2022 WV Corporate Tax Rate .065.

Line 16 – Mul ply line 14 by the Corpora on Net Income Tax Rate in line 15.

Line 17 – Enter the result from column 2, TOTAL CREDITS Line of completed Form CIT-120TC. The total amount of credits

cannot exceed the net income tax on line 16.

Line 18 – Subtract line 17 from line 16. This is your Adjusted Corpora on Net Income Tax. Enter this amount on CIT-120,

page 2, line 9.

PAGE 12 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

CIT-120, PAGE 2

Line 9 – Enter the adjusted Corpora on Net Income Tax amount from either Schedule 1, line 12, Schedule 2, line 18 or

Schedule UB-CR, total of all groups.

Line 10 – Prior year carry forward credit from your previous Corpora on Net Income Tax return.

Line 11 – Enter total es mated tax payments and any extension payment made with Form CIT-120EXT.

Line 12 – Enter the total amount of withholding credit from Form WVK-1C, NRW-2, and/or 1099. Check box if

withholding is from NRSR (nonresident sale of real estate).

Line 13 – Add lines 10 through 12. This total MUST match the total payments on Schedule C.

Line 14 – If this is an amended return, enter the amount of any overpayment previously refunded or credited.

Line 15 – Subtract line 14 from line 13. This is your company’s total payments.

Line 16 – If line 15 is larger than line 9 enter your overpayment here.

Line 17 – Enter the amount of the overpayment on line 16 to be credited to next year’s taxes.

Line 18 – Enter the amount of the overpayment on line 16 to be refunded (subtract line 17 from line 16).

Line 19 – If line 15 is smaller than line 9, enter the tax due on this line.

Line 20 – Determine the amount of interest due. For informa on regarding interest, see the general informa on on page

8 of this instruc on booklet.

Line 21 – Determine addi ons to tax due. For informa on regarding addi ons to tax, see the general informa on on

page 8 of this instruc on booklet.

Line 22 – Enter the amount of penalty for underpayment of es mated tax from Form CIT-120U, line 6.

Line 23 – Add lines 19 through 22. This is the balance due with this return. Make checks payable to the West Virginia Tax

Division or see www.tax.wv.gov for other payment op ons.

PAGE 13 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

SCHEDULE B: ADJUSTMENTS TO FEDERAL TAXABLE INCOME

ADJUSTMENTS INCREASING FEDERAL TAXABLE INCOME

Line 1 – Enter exempt interest or dividends from any state or local bonds or securi es from your federal return Form

1120, Schedule K or on Schedule M-1.

Line 2 – Enter the amount of US Government obliga on interest or dividends not exempt from state tax, less any

related expenses not deducted on the federal return. A ach suppor ng documenta on.

Line 3 – A ach an itemized schedule of taxes based upon income from line 17 of your federal income tax return, Form

1120 or pro forma Form 1120.

Line 4 – Taxpayers can elect to expense the cost of certain air and water pollu on control facili es located in West

Virginia in the year in which the cost of acquisi on, construc on or development was paid or incurred. Eligible

air and water pollu on control facili es are those located in West Virginia that are “cer fied pollu on control

facili es” as defined by Sec on 169 of the Internal Revenue Code. If this elec on is made, the total amount of

any federal deduc on for deprecia on or amor za on of such facili es is disallowed. The elec on is made on

the return for the year in which the cost is paid or incurred. Once made, the elec on or non-elec on is

irrevocable.

A taxpayer who reports all income to this state will make the adjustments for the cost of the facili es on

CIT-120 Schedule B, line 20. The deprecia on or amor za on on the facili es, including that a ributable to

cost expensed this year as well as prior years, deducted on the federal return, is entered on CIT-120 Schedule

B, line 4. A taxpayer who is subject to alloca on and appor onment makes the adjustment for the cost of the

facili es on Form CIT-120APT Schedule A-2, line 10, column 3. The deprecia on or amor za on on the facili es

deducted on the federal return for this year as well as previous years, is entered on Form CIT-120APT Schedule

A-2, lines 11 and 12 of column 3.

Line 5 – Corpora ons which are exempt from federal income tax are also exempt from West Virginia Corpora on Net

Income Tax. If such a corpora on has unrelated business taxable income (as defined by Sec on 512 of the

Internal Revenue Code), they must pay West Virginia Corpora on Net Income Tax on the unrelated business

taxable income. Enter the unrelated business taxable income as reported on Federal Form 990T.

Line 6 – Enter the amount of Federal Net Opera ng Loss from Federal Form 1120, line 29a.

Line 7 – I f you claim the West Virginia Neighborhood Investment Program Tax Credit, any deduc on, decreasing

adjustment, or decreasing modifica on taken on your federal return for any charitable contribu on made to

such Neighborhood Investment Program and for which the West Virginia credit is claimed, must be added back

on this line.

Line 8 – Taxpayers with foreign source income must adjust their federal taxable income by the amount of their taxable

income or loss from sources outside the United States. In determining foreign source income, the provisions of

Sec ons 861, 862, and 863 of the Internal Revenue Code apply.

Complete the following worksheet.

FOREIGN SOURCE INCOME WORKSHEET PETITIONING FOR AN ALTERNATIVE METHOD OF APPORTIONMENT

1. Taxable income from sources outside the United States

2. LESS foreign dividend gross-up

3. LESS subpart F income

4. West Virginia adjustment

PAGE 14 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

If the amount on line 4 of the worksheet is a posi ve figure, enter it on CIT-120, Schedule B, line 19. If it is a nega ve

figure, enter the amount of the loss on CIT-120, Schedule B, line 8 without the nega ve sign.

A ach copies of Federal Form 1118 to support your calcula on. If you did not file Federal Form 1118, you must prepare

and file a pro forma Federal Form 1118 to support your adjustment. If you filed a consolidated Federal Form 1118 and

file separate or unitary West Virginia returns, a ach both the true consolidated and a pro forma Federal Form 1118 to

support your adjustment.

Line 9 – Enter the amount of foreign taxes as deducted on your Federal Form 1120.

Line 10 – Add back for expenses related to certain REIT’s and regulated investment companies and certain interest and

intangible expenses (WV Code §11-24-4b).

Line 11 – Other increasing adjustments. Enter a brief descrip on of any adjustment in the space provided.

Submit a statement for any adjustment entered.

Line 12 – Add lines 1 through 11. Enter the total on Form CIT-120, Schedule 1, line 2 or CIT-120, Schedule 2, line 2.

ADJUSTMENTS DECREASING FEDERAL TAXABLE INCOME

Line 13 – Enter the amount of refund or credit of income taxes or taxes based upon net income imposed by this state or any

other jurisdic on included in federal taxable income. A ach suppor ng documenta on.

Line 14 – Enter the amount of interest expense on obliga ons or securi es of any state or its poli cal subdivisions disallowed

in determining federal taxable income. A ach suppor ng documenta on.

Line 15 – Enter the amount of US Government obliga on interest or dividends included in federal but exempt from state tax,

less related expenses deducted on your federal return. A ach suppor ng documenta on.

Line 16 – Enter total salary expense not allowed on your federal return due to claiming the federal jobs credit and include a

copy of Federal Form 3800 or 5884. Note: this decreasing adjustment is only applicable to the Work Opportunity

Credit from Federal Form 5884.

Line 17 – Enter the total foreign dividend gross-up (IRC Sec on 78) from Federal Form 1120.

Line 18 – Enter the total subpart F income (IRC Sec on 951) from Federal Form 1120.

Line 19 – See instruc ons for CIT-120 Schedule B, line 8. If Foreign Source Income from worksheet line 4 is posi ve, enter the

amount here.

Line 20 – See instruc ons for CIT-120 Schedule B, line 4. Mul state corpora ons must use CIT-120APT, Schedule A2, line 10.

Line 21 – A decreasing adjustment to federal taxable income is allowed for employer contribu ons to a medical savings

account established pursuant to WV Code §33-16-15, to the extent included in federal taxable income, less any

por on of the employer’s contribu ons withdrawn for purposes other than payment of medical expenses. The

amount taken as a decreasing adjustment may not exceed the maximum amount that would have been deducted

from the corpora on’s federal taxable income if the aggregate amount of the corpora on’s contribu ons to

individual medical savings accounts established under WV Code §33-16-15 had been contribu ons to a qualified

plan as defined under the Employee Re rement Income Security Act of 1974 (ERISA), as amended.

Line 22 – Qualified Opportunity Zone business income. You must include a copy of IRS 8996.

Line 23 – Other decreasing adjustments. Enter a brief descrip on of any adjustment in the space provided.

Submit a statement for any adjustment entered.

Line 24 – Taxpayers that own certain tax-exempt government obliga ons and/or obliga ons secured by certain residen al

property located in West Virginia can take a special allowance that further reduces federal taxable income.

Complete Form CIT-120, Schedule B-1 to determine the amount of the allowance.

Line 25 – Add lines 13 through 24. Enter the amount here and on CIT-120, Schedule 1, line 3 or CIT-120, Schedule 2, line 3.

PAGE 15 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

SCHEDULE B-1 ALLOWANCE FOR GOVERNMENTAL OBLIGATIONS/

OBLIGATIONS SECURED BY RESIDENTIAL PROPERTY (§ 11-24-6 F ( ))

Taxpayers that own certain tax-exempt government obliga ons and obliga ons secured by certain residen al property

located in West Virginia can take a special allowance that further reduces federal taxable income. Complete CIT-120

Schedule B-1 to determine the amount of the allowance. The value of these obliga ons and loans is determined using

the average of the monthly beginning and ending account balances. These account balances are determined at cost in

the same manner that such obliga ons, investments and loans are reported on the balance sheet of your federal tax

return.

Lines 1 through 4 - A ach copy of worksheets suppor ng the calcula on of average monthly balance.

Line 6 – Average the beginning and ending balance of Federal Form 1120, Schedule L, line 15.

Line 8 – CIT-120, Schedule 1, line 1 or Schedule 2, line 1 plus CIT-120, Schedule B, line 12 minus the sum of lines 13

through 23, plus Form CIT-120APT, Schedule A2, lines 10, 11, and 12.

SCHEDULE C – SCHEDULE OF TAX PAYMENTS

If the number of payments reported on Schedule C exceeds 10, you must file electronically.

Column 1 – Enter the name of the en ty making the payment or issuing the withholding credit.

Column 2 – Enter the FEIN of the en ty making the payment or issuing the withholding credit.

Column 3 – Enter the date of any payments made by, or on behalf of, the en ty.

Column 4 – Enter a descrip on of the type of payment made by, or on behalf of, the en ty,

Column 5 – Enter the amount of the payment made by, or on behalf of, the en ty.

Total Line – Sum of the payments shown in Column 5.

The total amount of payments must equal the amount reported on Form CIT-120, line 13.

SCHEDULE D – REPORTABLE ENTITIES

If any box is checked in the Reportable En es Sec on of page 1, the name and FEIN of each reportable en ty must be

entered on Schedule D.

If the number of en es exceeds ten (10) you must file electronically.

Column 1 – Enter the name of the reportable en ty.

Column 2 – Enter the FEIN of the reportable en ty.

Column 3 – Enter the name of the reportable en ty’s parent.

Column 4 – Enter the FEIN of the parent.

Column 5– Enter the Alpha Character designa on for the explana on of the rela onship between reportable en ty and

en ty submi ng this West Virginia Return.

A Pass through en ty you are a partner, member, or shareholder doing business in WV

B En ty you own 80% of vo ng stock

C En ty that owned more than 80% of your stock

D Disregarded en ty or QSUB

E Controlled Foreign Corpora on

If the number of en es reported on Schedule D exceeds 10, you must file electronically.

PAGE 16 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image | CIT-120TC: SUMMARY OF CORPORATION NET INCOME TAX CREDITS The CIT-120TC, Summary of Corpora on Net Income Tax Credits, is a form used by corpora ons to summarize the tax credits that they claim against their Corpora on Net Income Tax liability. In addi on to comple ng the CIT-120TC, each tax credit has a schedule or form that is used to determine the amount of credit that can be claimed. Please note that some tax credit schedules require a completed applica on to be submi ed and approved before the tax credit schedule can be filed. Both the CIT-120TC and the appropriate credit calcula on schedule(s) or form(s) must be a ached to your return in order to claim a tax credit. Line 19 – Total credits: Add column 2, lines 1 through 18. Note: The amount of credit used cannot be greater than the Corpora on Net Income Tax assessed on the return. For addi onal informa on and a copy of the tax credit schedules and applica ons please visit tax.wv.gov. If you are claiming the Neighborhood Investment Program Credit, you are no longer required to enclose the WV NIPA-2 credit schedule with your return. You must maintain the schedule in your files. SCHEDULE NOL: WV NET OPERATING LOSS CARRYFORWARD CALCULATION (§11-24-6( )) D WHO SHOULD COMPLETE SCHEDULE NOL? All corpora ons claiming a West Virginia net opera ng loss carry forward deduc on on Form CIT-120, Schedule 1, line 5, CIT-120, Schedule 2, line 11 or Schedule UB-CR, column 16 must complete this schedule to support their net opera ng loss deduc on. Schedule NOL is not a claim for refund. It is a calcula on schedule to support the net opera ng loss carryforward deduc on. Any amount claimed as a federal net opera ng loss deduc on must be added back to federal taxable income on West Virginia Form CIT-120, Schedule B, line 6 for a separate filer or column 2f (en ty specific of applicable group) if a combined filer. The West Virginia net opera ng loss carryforward deduc on is entered on Form CIT-120, Schedule 1, line 5, Schedule 2, line 11 or Schedule UB-CR, column 16 of each applicable group. West Virginia NOL generated in periods a er 2017 can be carried forward indefinitely. Any WV Net Opera ng Loss deduc on is limited to 80% of taxable income star ng in the 2022 taxable year. Note that rules for pre-2018 WV NOL remain the same. A net opera ng loss deduc on of a mul state corpora on is subject to West Virginia alloca on and appor onment rules. The West Virginia net opera ng loss deduc on is limited to net opera ng losses incurred by a corpora on which performed business in West Virginia and filed Corpora on Net Income Tax Returns in prior taxable years. The amount of net opera ng loss deduc on available to an affiliated group, which elects for the first me to file a consolidated return for a taxable year ending a er July 1, 1988, is limited to the net opera ng losses incurred by members of the affiliated group which did business in West Virginia and filed separate West Virginia returns in prior years. A West Virginia net opera ng loss deduc on will not be allowed for net opera ng losses of those members of the affiliated group which did no business in West Virginia in prior taxable years and were not required to file West Virginia Corpora on Net Income Tax Returns. SRLY RULES. The separate return limita on years (SRLY) rules set forth in Treasury Regula on §1.1502 apply in determining the allowable West Virginia net opera ng loss deduc on. When the SRLY rules apply, a member of an affiliated group’s net opera ng loss carried forward from its separate return year can only offset that por on of the taxable income a ributable to that member of the group. PAGE 17 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS |

Enlarge image |

Schedule NOL is designed to support the claiming of a West Virginia net opera ng loss carryforward deduc on by

providing informa on on the year of the loss and how the loss was/is being used. Enter the year of loss for each NOL in

Column 1 and the FEIN of the en ty incurring the loss in Column 2. Columns 3 through 6 will determine current available

amounts and amounts eligible for carryforward.

Column 1 – Year of loss. Enter in column 1 the applicable tax year ending date(s) for the year(s) that you had net

opera ng loss(es).

Column 2 – Enter name and FEIN of the Consolidated Parent Corpora on if you filed a consolidated return prior to 2009

and had a West Virginia Net Opera ng Loss or enter name and FEIN of all separate members’ West Virginia

net opera ng losses that filed separately prior to 2009.

Column 3 – Amount of West Virginia net opera ng loss. Enter the amount of West Virginia net opera ng loss that

corresponds to the year of the loss shown in Column 1.

Column 4 – Amount carried back to years prior to loss year. Enter the total amount of loss for the taxable year entered

in column 1 that was carried back to a year, or years prior to the year of the actual loss.

Column 5 – Amount carried forward to years prior to this year. Enter the total amount of loss for the taxable year

entered in column 1 that was carried forward to a year, or years, prior to the current taxable year.

Column 6 – Amount being used this year. Enter the amount of loss for the taxable year entered in column 1 that is being

used to offset West Virginia taxable income for the current taxable year.

Column 7 – Remaining unused net opera ng loss. Enter the amount of loss for the tax year entered in column 1 that

remains to be carried to a taxable year subsequent to the current taxable year.

TOTAL NET OPERATING LOSS CARRYFORWARD DEDUCTION FOR CURRENT TAXABLE YEAR.

The amount of the West Virginia net opera ng loss carryforward deduc on claimed on Form CIT-120, Schedule 1,

Schedule 2 or Schedule UB-CR of the current year’s tax return must equal the sum of Form CIT-120, Schedule NOL,

column 6. The West Virginia net opera ng loss carryforward deduc on cannot reduce West Virginia taxable income

below zero.

PAGE 18 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

CIT-120 APT – ALLOCATION AND APPORTIONMENT FOR MULTISTATE CORPORATIONS

SCHEDULES A1 & A2 – ALLOCATION OF NONBUSINESS INCOME

If the corpora on’s business ac vi es take place both within and without West Virginia and the corpora on is also taxable in

another state, certain items of nonbusiness income that are included in federal taxable income are directly allocated. All other

income must be appor oned.

Business income arises from transac ons and ac vi es in the regular course of the corpora on’s trade or business and

includes income from tangible and intangible property if the acquisi on, management or disposi on of the property

cons tutes integral parts of the corpora on’s trade or business.

Nonbusiness income includes all income that is not properly classified as business income less all expenses a ributable to the

produc on of this income. Nonbusiness income is allocated to West Virginia if (1) the corpora on’s commercial domicile, the

principal place from which the trade or business is managed is located in West Virginia; or (2) property crea ng the

nonbusiness income is u lized in West Virginia. Nonbusiness income from real property is allocated to West Virginia if the

corpora on’s commercial domicile is located in West Virginia, or, in the case of patents or copyrights, if they are used in West

Virginia.

For addi onal informa on regarding the nonbusiness income, you may request a copy of Publica on TSD-392, “Corpora on

Net Income Tax Nonbusiness Income”, by contac ng our Taxpayer Services Division or online at tax.wv.gov.

Determine nonbusiness income allocated to West Virginia and outside West Virginia by comple ng Form CIT-120APT,

Schedules A1 and A2. Only those types of nonbusiness income listed on Form CIT-120APT, Schedules A1 and A2 can be

allocated. Any other types of income that the corpora on classifies as nonbusiness must be appor oned.

Line 9 – Enter the amount from Form CIT-120APT, Schedule A1, column 3, line 9 on Form CIT-120, Schedule 2, line 5.

Line 13 – Enter the amount from Form CIT-120APT, Schedule A2, column 3, line 13 to Form CIT-120, Schedule 2, line 9.

SCHEDULE B – APPORTIONMENT FORMULA

If the corpora on’s business ac vi es take place both within and without West Virginia and the corpora on is also taxable in

another state, all net income, a er deduc ng those items of nonbusiness income allocated on Form CIT-120APT, Schedules A1

and A2 must be appor oned to West Virginia by using the appropriate appor onment formula. Comple on of CIT-120APT,

Schedule B is required even if appor onment is zero.

Special appor onment formulas apply to motor carriers and to financial organiza ons. If you are filing for a financial

organiza on, follow the appor onment instruc ons for Form CIT-120APT, Schedule B, Part 3. If you are filing for a motor

carrier, follow the appor onment instruc ons for Form CIT-120APT Schedule B, Part 2.

MULTISTATE CORPORATIONS – SINGLE SALES FACTOR

PART 1

To determine your West Virginia appor onment percentage, first determine the following factors:

SALES FACTOR.

The term “sales” means all gross receipts of the taxpayer that are business income. The sales factor includes all gross

receipts derived from transac ons and ac vity in the regular course of your trade or business, less returns and

allowances. Do not include interest or dividends from obliga ons of the United States government, which are exempt

from taxa on in West Virginia, or gross receipts from an ac vity that produced nonbusiness income.

The numerator (column 1) of the sales factor includes all gross receipts a ributable to West Virginia and derived from

transac ons and ac vity in the regular course of your trade or business. All interest income, service charges

or me-price differen al charges incidental to such gross receipts must be included regardless of the place

where the accoun ng records are maintained or the loca on of the contract or other evidence of

indebtedness.

PAGE 19 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

The denominator (column 2) of the sales factor includes all gross receipts derived from transac ons and ac vity in the

regular course of your trade or business that was reflected in your gross income reported and as appearing on

your federal income tax return unless otherwise excluded. Sales of tangible personal property delivered or

shipped to a purchaser within a state in which the corpora on is not taxed (e.g. under Public Law 86-272) are

no longer to be excluded from the denominator.

Divide column 1 by column 2 and enter the result in column 3. State the result as a decimal frac on and round to six (6)

places a er the decimal. Enter the six (6) digit decimal frac on from column 3 on CIT-120, Schedule 2, line 7.

MOTOR CARRIERS – SPECIAL SINGLE FACTOR FORMULA

PART 2 – VEHICLE MILES.

Motor carriers of property or passengers are subject to special appor onment rules. Motor carriers must appor on their

business income by using a single factor formula of vehicle miles.

A motor carrier is any person engaged in the transporta on of passengers and/or property for compensa on by a motor

propelled vehicle over roads in West Virginia, whether on a scheduled route or otherwise. The term “vehicle miles”

means the opera ons of a motor carrier over one mile.

The special appor onment formula for motor carriers does NOT apply if:

a. The motor carrier neither owns nor rents any real or tangible personal property located in West Virginia, has

made no pickups or deliveries within West Virginia, and has traveled less than 50,000 miles in West Virginia

during the taxable year; or

b. The motor carrier neither owns nor rents any tangible personal property located in West Virginia except vehicles

and makes no more than 12 trips into or through West Virginia during the taxable year.

Under either (A) or (B), the mileage traveled in West Virginia may not be more than five percent (.05) of the total vehicle

miles traveled in all states during the taxable year.

Determine the appor onment factor by entering the appropriate vehicle miles for West Virginia in column 1, and vehicle

miles everywhere in column 2.

Divide column 1 by column 2 and enter the result in column 3. State the result as a decimal frac on and round to six (6)

places a er the decimal. Enter the six (6) digit decimal frac on from column 3 on CIT-120, Schedule 2, line 7.

FINANCIAL ORGANIZATIONS – SPECIAL SINGLE FACTOR FORMULA

PART 3 – GROSS RECEIPTS.

Financial organiza ons subject to appor onment must appor on their business income by using a single factor gross

receipts formula.

A financial organiza on is any holding company or regulated financial corpora on or subsidiary thereof, or any

corpora on deriving more than fi y percent (.5) of its gross receipts from one or more of the following:

1. Making, acquiring, selling, or servicing loans or extensions of credit.

2. Leasing or ac ng as an agent, broker, or advisor in connec on with leasing real and personal property that is the economic

equivalent of an extension of credit.

3. Opera ng a credit card business.

4. Rendering estate or trust services.

5. Receiving, maintaining, or otherwise handling deposits.

6. Engaging in any other ac vity with an economic effect comparable to any of the above.

Financial organiza ons regularly engaging in business in West Virginia shall appor on their business income by means

of a single factor of gross receipts appor onment formula. A financial organiza on not having its commercial domicile in

West Virginia is presumed to be regularly engaging in business in West Virginia if during any year it obtains or solicits

PAGE 20 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

business with 20 or more persons within West Virginia, or the sum of its gross receipts a ributable to sources in West

Virginia equals or exceeds $100,000.00.

Gross receipts from the following ownership interest (and certain related ac vi es) will not be considered in determining

whether a financial organiza on is subject to taxa on.

1. An interest in a real estate mortgage investment conduit, a real estate investment, or a regulated investment company;

2. An interest in a loan backed security represen ng ownership or par cipa on in a pool of promissory notes or cer ficates or

interest that provide for payments in rela on to payments or reasonable projec ons of payments on the notes or

cer ficates;

3. An interest in a loan or other asset from which the interest is a ributed to a consumer loan, a commercial loan or a secured

commercial loan, and in which the payment obliga ons were solicited and entered into by a person that is independent and

not ac ng on behalf of the owner; or an interest in the right to service or collect income from such a loan or asset; or

4. An amount held in an escrow or trust account with respect to property described above.

However, if a financial organiza on is subject to taxa on when gross receipts from these interests are not considered,

such receipts must then be included when determining the amount of taxes owed.

Neither the numerator nor the denominator of the gross receipts factor should include gross receipts from obliga ons

and certain loans on which you claim the special allowance on Form CIT-120, Schedule B-1.

Divide column 1 by column 2 and enter in column 3. State the result as a decimal frac on and round to six places a er

the decimal. Enter the six (6) digit decimal frac on from column 3 on Form CIT-120, Schedule 2, line 7.

PETITIONING FOR AN ALTERNATIVE METHOD OF APPORTIONMENT

To use an alternate method of alloca on and appor onment ro determine your taxable net income, you must pe on

the Tax Commissioner. Your pe on for an alternate method must be filed no later than the normal due date of your

return. You must have wri en permission to use an alternate appor onment method before filing your return.

Permission will only be granted if you can show that the statutory formula does not properly reflect your taxable income,

and if the alternate method properly and fairly shows your West Virginia taxable income.

Your pe on should include your name and address, state of incorpora on and principal place of business, a descrip on

of the kind(s) of business in which you are engaged, a detailed statement of how sales are made in West Virginia, a

computa on of your West Virginia taxable income using the statutory appor onment formula and using your proposed

alternate formula, and a summary of the facts that support your posi on.

Send your pe on to the West Virginia Tax Division, Tax Account Administra on Division, Corporate Tax Unit, PO Box

1202, Charleston, WV 25324-1202.

CIT-120U

Use this form to determine if any penalty for underpayment of es mated West Virginia Corpora on Net Income Tax is

due.

Who must pay the penalty? A corpora on is required to file a declara on of es mated corpora on net income tax and

make es mated tax payments on Form WV/CIT-120ES if its West Virginia taxable income can reasonably be expected to

exceed $10,000.00, which equals a tax liability a er tax credits of more than $650.00 (Code §11-24-16). Es mated tax is

a corpora on’s expected income tax liability minus its tax credits. A taxpayer is required to remit, in equal installments on

the 15th day of the 4th, 6th, 9th, and 12th months of their taxable year, at least ninety percent (.90) of the tax due for

the filing period.

If a corpora on did not pay enough es mated tax by the due dates, it will be assessed the penalty. The penalty is figured

separately for each installment due date. The corpora on may owe the penalty for an earlier installment due date, even

if it paid enough tax later to make up the underpayment. The underpayment of es mated tax penalty rate will be 9.25%

in 2022.

PART 1: ALL FILERS MUST COMPLETE THIS PART

PAGE 21 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

Line 1 – Enter your Corpora on Net Income Tax a er credits (Form CIT-120, line 9). If this amount is less than $650.00,

skip lines 2 and 3 and enter 0 on line 5.

Line 2 – Mul ply the amount on line 1 by ninety percent (.9) and enter the result here. This is the amount the

corpora on should have paid in es mated tax for this taxable year.

Line 3 – Enter the Corpora on Net Income Tax a er credits from your 2019 return. If the corpora on did not file a 2019

return leave this line blank.

Line 4 – Enter the smaller of line 2 or line 3. If line 3 is blank enter the amount from line 2. This is the amount the

corpora on should have paid in es mated tax for this taxable year.

Line 5 – Enter the amount from line 4. This is the amount of es mated Corpora on Net Income Tax that should have

been paid.

DETERMINE THE PENALTY BY COMPLETING PART II, III, AND IV

Part II: Annualized Installment Worksheet

If the taxable income varied during the year, the corpora on may be able to lower or eliminate the amount of one or

more required installments by using the annualized installment worksheet. To use the annualized installment method to

figure the penalty, complete Part I, Part II, Part III, and Part IV of Form CIT-120U. Follow the line by line instruc ons

entered on Form CIT-120U.

PART III: CALCULATE THE UNDERPAYMENT

Line 23 – In column A, enter the es mated tax payments deposited by the 15th day of the 4th month of your tax year.

In column B, enter payments made a er the 15th day of the 4th month through the 15th day of the 6th month

of your tax year.

In column C, enter payments made a er the 15th day of the 6th month through the 15th day of the 9th month

of your tax year.

In column D, enter payments made a er the 15th day of the 9th month through the 15th day of the 12th

month of the tax year.

Line 29 – If any of the columns in line 29 shows an underpayment, complete Part IV to figure the penalty for that period.

PART IV: CALCULATE THE PENALTY

Complete lines 31 through 42 to determine the amount of the penalty. The penalty is figured for the period of

underpayment determined under West Virginia Code §11-10-18a using the rate of interest determined under West

Virginia Code §11- 10-17 or 17a, whichever is appropriate for the taxable year. For underpayments involving periods a er

January 1, 2023, see the instruc ons for lines 39 and 40.

Line 31 – Enter the date on which the installment payment was made or the original due date of the annual return,

whichever is earlier. The due date of the return is the 15th day of the 4th month following the close of the

taxable year for corpora ons. The due date of the annual return of an exempt organiza on with unrelated

business taxable income is the 15th day of the 5th month following the close of the taxable year. The payment

of es mated tax is applied against underpayments of required installments in the order that installments are

required to be paid, regardless of which installment the payment pertains to.

For example, a corpora on has an underpayment for the April 15th installment of $1,000. The June 15th installment

requires a payment of $2,500. On June 10th, the corpora on deposited $2,500 to cover the June 15th installment.

$1,000 of this payment is considered to be for the April 15th installment. The penalty for April 15th installment is figured

to June 10th (56 days). The payment to be applied to the June 15th installment will then be $1,500.

PAGE 22 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

If the corpora on made more than one payment for a required installment, a ach a separate computa on for each

payment.

Lines 39 & 40 - For underpayments involving periods a er January 1, 2023, use the interest rate established by the State

Tax Commissioner. You can contact the West Virginia Tax Division, Taxpayer Services Division, at

1-800-982-8297 to get rate informa on. Administra ve No ces adjus ng interest rates may also be found

online at tax.wv.gov.

Line 42 – If you have completed this form to determine the penalty for underpaying the corpora on’s es mated

Corpora on Net Income Tax, enter the amount on line 6 on Form CIT-120, line 22.

PAGE 23 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

COMBINED REPORTING

COMBINED CORPORATION NET INCOME REPORTING REQUIRED (§11-24-13 ( )). A J

For tax years beginning on or a er January 1, 2009, any taxpayer engaged in a unitary business with one or more other

corpora ons shall file a combined report which includes the income, alloca on, and appor onment of income of all

corpora ons that are members of the unitary business. Notwithstanding any provision to the contrary in this ar cle, the

income of an insurance company, the alloca on or appor onment related thereto, and the appor onment factors of an

insurance company shall not be included in a combined report filed under this ar cle unless specifically required to be

included by the Tax Commissioner.

Net opera ng loss (NOL) carryovers earned during a year in which the taxpayer filed a consolidated tax return (§11-24-13c).

West Virginia computes net opera ng losses on a post-appor onment basis, including business and nonbusiness income

adjustments. NOLs can only be carried forward (or backwards) to be applied against West Virginia source income of the

combined group members to which it is a ributable. NOL’s that were incurred by an en ty in a period in which the en ty filed

separately, cannot be used by other members of the combined group. There is an excep on for NOL’s earned when the

taxpayer was filing on a consolidated basis. Those NOL’s can be carried over and applied against the income of any former

member of the consolidated (controlled) group. (see NOL Calcula on instruc ons on page 14)

WATER’S-EDGE REPORTING.

Water’s-Edge Repor ng is mandated absent an affirma ve elec on to report based upon a worldwide unitary combined

report. Members of the Water’s-Edge Repor ng group include:

1. Any unitary member incorporated in the United States or formed under the laws of any state, the District of Columbia

or any territory or possession of the United States;

2. Any unitary member whose average property, payroll and sales factors within the United States is twenty percent or more;

3. Any unitary member which is a domes c interna onal sales corpora on, a foreign sales corpora on, or an export

trade corpora on as defined by federal law;

4. Any unitary member with effec vely connected income with the conduct of a trade or business within the United

States to the extent of that effec vely connected income;

5. Any unitary member that is a “controlled foreign corpora on”, to the extent of the members’ Subpart F income, unless

that income is subject to an effec ve rate of tax that is greater than ninety percent of the maximum federal rate;

6. Any unitary member that earns more than twenty percent of its income from intangible property or service-related

ac vi es that are deduc ble against the business income of other members of the Water’s-Edge group; and

7. Any unitary member doing business in a tax haven.

Worldwide Unitary Combined Repor ng: A corpora on may choose to file Worldwide Unitary Combined Repor ng. To do so,

please fill out and sign West Virginia Form CIT-120 OPT and a ach to your return. This elec on is binding for 10 years unless a

wri en request to withdraw for reasonable cause has been sent to the commissioner and granted.

GENERAL INFORMATION

What is the purpose of the UB Schedules? The purpose of the UB Schedules is to enable a unitary business group to

determine the amount of its unitary business income that is a ributable to West Virginia. A unitary business group’s business

income includes all income that may be appor oned by formula among the states in which the group is doing business without

viola ng the Cons tu on of the United States.

What is a unitary business group ? The term “unitary business group” means a group of persons related through common

ownership whose business ac vi es are integrated with, dependent upon, and contribute to each other. In the case of a

corpora on, common ownership is defined as the direct or indirect ownership or control of more than fi y percent (.5) of the

outstanding vo ng stock. For further instruc ons see WV Code 11-24-13f (a) waters-edge repor ng-subdivision (1) through (7) .

What are the filing requirements? Corpora ons that are members of the same unitary business group must file a combined

report including all required informa on of every business engaging in the unitary business with the corpora on. This report

must be filed with each member’s separate return unless the group elects to designate a corpora on as surety and file a

combined return.

PAGE 24 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

SPECIFIC INSTRUCTIONS

SCHEDULE UB – LIST OF MEMBERS IN A UNITARY COMBINED GROUP.

List all members of the unitary business group including group number (1-3), name, FEIN, month and year ending, total tax

from UB-CR, total payments, and prior year credits. Make copies of the blank Schedule UB as needed. The following list defines

the group numbers:

Group 1 – Regular en es

Group 2 – Motor carriers

Group 3 – Financial organiza ons

SCHEDULE UB-CR. COMBINED REPORT.

The purpose of the Schedule UB-CR Combined Report is to provide a method of repor ng the separate business income of

mul ple companies within a unitary group onto one statement. The business income is reported and appor oned for each

company as if it were filed separately. The income for all companies is then combined, a er elimina ons, to allow the business

income of the unitary group to be filed on one CIT-120 return.

The UB-CR MUST be used when filing a combined report and/or combined return. Taxpayers who file combined returns must

file their West Virginia CIT-120 return electronically. The UB-CR must be supported within the electronic filing so ware in

order to file a combined return.

For most filers, the unitary business structure will be in one of the following groups: Regular En es, Motor Carriers, or

Financial Organiza ons. Therefore, the Combined row of the appropriate WV Net Income Tax group from Schedule UB-CR will

be what is transferred to the CIT-120, page 2, line 9. In the event of mul ple groups, add the Taxable Income from each group

together and enter on CIT-120, page 2, line 9.

Group 1 - Regular En es

Group 2 – Motor Carriers

Group 3 – Financial Organiza ons

Note: The spreadsheet for each Group type is the same except for the way the WV appor onment is calculated.

Enter Name of each en ty on the appropriate Group tab

Enter the FEIN of each en ty on the appropriate Group tab

Column 1 – Enter the Federal taxable income for each en ty in the appropriate group

PAGE 25 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

PART 1 – INCREASING ADJUSTMENTS TO FEDERAL INCOME

Column 2a Enter the interest or dividends on obliga ons or securi es from any state or poli cal subdivision not exempt from

state tax.

Column 2b Enter US obliga on interest/dividends not exempt from state tax

Column 2c Enter income/other taxes based upon net income, imposed by this state or any other jurisdic on, deducted on

your federal return

Column 2d Enter federal deprecia on/amor za on for wholly WV corpora on water/air pollu on facili es

Column 2e Enter unrelated business taxable income of a corpora on exempt from federal tax (IRC Sec 512)

Column 2f Enter federal net opera ng loss

Column 2g Enter contribu ons to NIPA

Column 2h Enter net opera ng losses from sources outside the US

Column 2i Enter foreign taxes deducted on your federal return

Column 2j Enter add back for expenses related to certain REIT’s and Regulated Investment Companies and certain interest

and intangible expenses (WV Code §11-24-4b)

Column 2k Enter other increasing adjustments (you must include a statement of explana on with your return)

Column 3 Sum of the increasing adjustments

PART 2 – DECREASING ADJUSTMENTS TO FEDERAL INCOME

Column 4a Enter refund/credit on taxes based upon net income included in federal taxable income

Column 4b Enter interest expense on obliga ons/securi es of any state or poli cal subdivision disallowed in determining

federal taxable income

Column 4c Enter salary expense not allowed on federal return due to claiming Work Opportunity Credit

Column 4d Enter foreign dividend gross-up (IRC Sec 78)

Column 4e Enter Subpart F income (IRC Sec 951)

Column 4f Enter taxable income from sources outside the US

Column 4g Enter cost of wholly WV water/air pollu on control facili es

Column 4h Enter federal taxable income employer contribu ons to medical savings accounts withdrawn for nonmedical purposes

Column 4i Qualified Opportunity Zone business income

Column 4j Enter allowance for obliga ons/investments

Column 4k Enter other decreasing adjustments (you must include a state of explana on with your return)

Column 5 Sum of the decreasing adjustments

PART 3 – TAXABLE INCOME CALCULATION

Column 6 Adjusted taxable income of each en ty

Column 7 Total nonbusiness income from everywhere of each en ty

Column 8 Total non-unitary business income everywhere of each en ty

Column 9 Income subject to appor onment per en ty

Column 10 Group income subject to appor onment

Column 11 WV appor onment factor per en ty

Column 12 WV appor oned income

Column 13 Enter nonbusiness income allocated to WV

Column 14 Enter total non-unitary business income appor oned to WV

Column 15 WV Taxable Income

PAGE 26 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

APPORTIONMENT FACTOR CALCULATIONS

GROUP 1 - REGULAR ENTITIES

WV Sales Enter the amount of WV sales for each en ty

Everywhere Sales – Enter the amount of the Sales by each en ty in all loca ons (WV plus all others). All sales are to be

included (Throw-out rule is no longer valid) unless otherwise excluded on the federal return . That sum will be

used as the denominator in the appor onment factor calcula on.

GROUP 2 – MOTOR CARRIERS

WV Vehicle Mileage – Enter the WV vehicle mileage for each en ty

Everywhere Vehicle Mileage – Enter the amount of vehicle mileage in all loca ons (WV and all others). This amount will be

summed in the “Combined en es” row. That sum is the amount that will be used in the appor onment factor

calcula on.

GROUP 3 – FINANCIAL ORGANIZATIONS

WV Gross Receipts – Enter the WV gross receipts for each en ty

Every Gross Receipts – Enter the amount of gross receipts in all loca ons (WV and all others). This amount will be summed in

the “Combined en es” row. That sum is the amount that will be used in the appor onment factor calcula on.

PART 4 – WV NOL SECTION

NOL1 NOL generated as the result of filing a consolidated return prior to 2009

NOL 2 NOL carryforward generated by the en ty from an individual return or a combined report from 2009 to 2017

NOL 3 NOL carryforward generated by the en ty from an individual return or a combined report a er 2017

NOL 4 Total WV NOL available for use in the tax period per en ty

NOL 5 NOL generated by en ty in this period

NOL 6 NOL available for use in future periods by en ty

Column 16 (NOL 7) WV Net Opera ng Loss used this tax period per en ty

Column 17 Subtotal (See NOL pg 8)

Column 18 REIT inclusion and other WV taxable income

Column 19 WV net taxable income per en ty

Column 20 Tax rate in 2022 tax period (.065)

Column 21 WV income tax before credits per en ty

PART 5 – CREDITS SECTION

C1. a Economic Opportunity Tax Credit (§11-13Q) Schedule WV/EOTC-1

C1. b High Technology Manufacturing Business (§11-13Q-10a) Schedule EOTC-HTM

C1. c Manufacturing Investment Tax Credit (§11-13S) Schedule WV/MITC-1

C1. d Historic Rehabilitated Buildings Investment Credit (§11-24-23a) Schedule RBIC

C1. e West Virginia Neighborhood Investment Program Credit (§11-13J) Form WV/NIPA-2

C1. f Environmental Agricultural Equipment Tax Credit (§11-13k) Form WV/AG-1

C1. g Electric, Gas, and Water U li es Rate Reduc on Credit (§11-24-11) Schedule L

C1. h West Virginia Military Incen ve Credit (§11-24-12) Schedule J

C1. i Appren ce Training Tax Credit (§11-13w) Schedule WV/ATTC-1

PAGE 27 2022 CIT-120 - CORPORATION NET INCOME TAX INSTRUCTIONS

|

Enlarge image |

C1. j Manufacturing Property Tax Adjustment Credit (§11-13Y) Schedule WV/MPTAC-1

C1. k Alterna ve Fuel Tax Credit (§11-6d) Schedule AFTC-1

C1. l Innova ve Mine Safety Technology Tax Credit (§11-13BB) Schedule IMSTTC-1

C1.m Farm to Food Bank Tax Credit (§11-13DD)

C1.n Post Coal Mine Site Business Credit (§11-28) Schedule PCM-1

C1.0 Downstream Natural Gas Manufacturing Investment Tax Credit (§11-13GG) Schedule DNG-1

C1.p Natural Gas Liquids (§11-13HH) Schedule NGL-1

C1.q Dona on or Sale of Vehicle to charitable Organiza ons (§11-13FF) Schedule DSV-1

C1.r Small Arms And Ammuni on Manufacturers Credit (§11-13KK) Schedule SAAM-1

C1.s Capital Investment in Child-Care Property Tax Credit (§11-21-97) Schedule CICCP-1

C1.t Opera ng Costs of Child Care Property Tax Credit (§11-21-97) Schedule CICCP-2

C2. Total credits claimed

C3. Total credits available for use by each en ty this period

PART 5 – WV NET INCOME

C4 WV Net Income Tax per en ty (enter the sum of the Combined Total row of this column for Regular En es,