Enlarge image

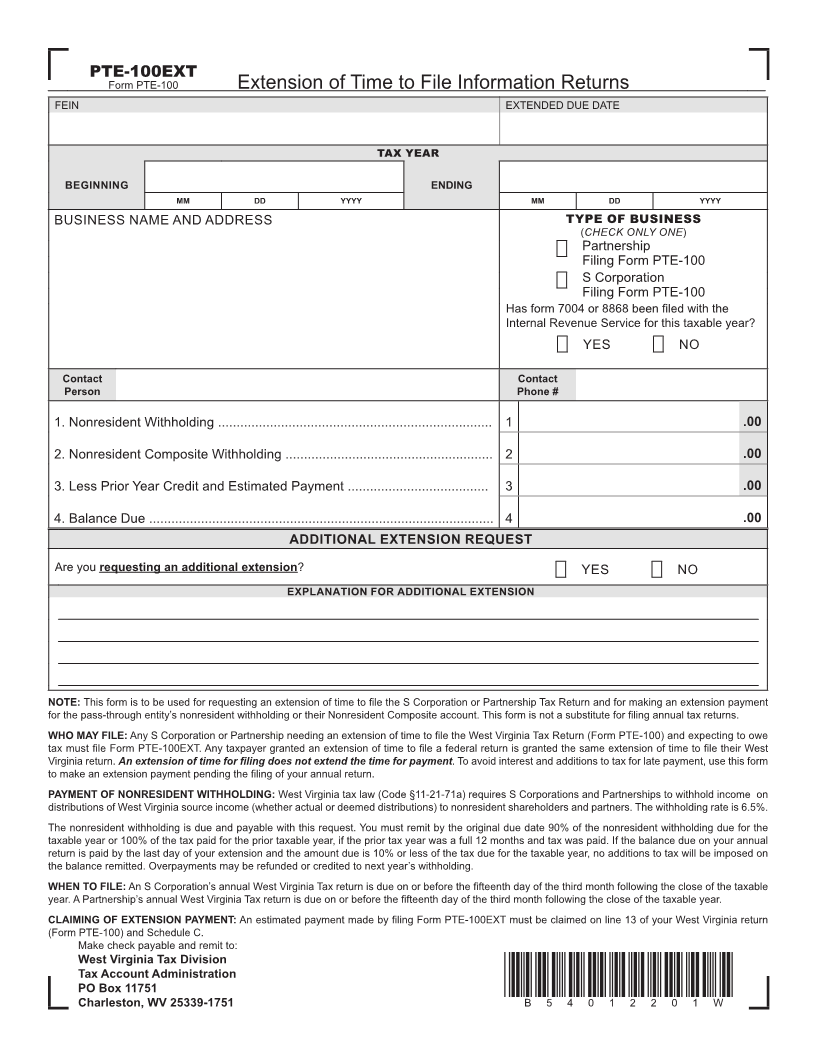

PTE-100EXT

Form PTE-100 Extension of Time to File Information Returns

FEIN EXTENDED DUE DATE

TAX YEAR

BEGINNING ENDING

MM DD YYYY MM DD YYYY

BUSINESS NAME AND ADDRESS TYPE OF BUSINESS

(CHECK ONLY ONE )

Partnership

Filing Form PTE-100

S Corporation

Filing Form PTE-100

Has form 7004 or 8868 been fi led with the

Internal Revenue Service for this taxable year?

YES NO

Contact Contact

Person Phone #

1. Nonresident Withholding .......................................................................... 1 .00

2. Nonresident Composite Withholding ........................................................ 2 .00

3. Less Prior Year Credit and Estimated Payment ...................................... 3 .00

4. Balance Due ............................................................................................. 4 .00

ADDITIONAL EXTENSION REQUEST

Are you requesting an additional extension? YES NO

EXPLANATION FOR ADDITIONAL EXTENSION

NOTE: This form is to be used for requesting an extension of time to file the S Corporation or Partnership Tax Return and for making an extension payment

for the pass-through entity’s nonresident withholding or their Nonresident Composite account. This form is not a substitute for filing annual tax returns.

WHO MAY FILE: Any S Corporation or Partnership needing an extension of time to fi le the West Virginia Tax Return (Form PTE-100) and expecting to owe

tax must file Form PTE-100EXT. Any taxpayer granted an extension of time to file a federal return is granted the same extension of time to fi le their West

Virginia return.An extension of time for filing does not extend the time for payment. To avoid interest and additions to tax for late payment, use this form

to make an extension payment pending the filing of your annual return.

PAYMENT OF NONRESIDENT WITHHOLDING: West Virginia tax law (Code §11-21-71a) requires S Corporations and Partnerships to withhold income on

distributions of West Virginia source income (whether actual or deemed distributions) to nonresident shareholders and partners. The withholding rate is 6.5%.

The nonresident withholding is due and payable with this request. You must remit by the original due date 90% of the nonresident withholding due for the

taxable year or 100% of the tax paid for the prior taxable year, if the prior tax year was a full 12 months and tax was paid. If the balance due on your annual

return is paid by the last day of your extension and the amount due is 10% or less of the tax due for the taxable year, no additions to tax will be imposed on

the balance remitted. Overpayments may be refunded or credited to next year’s withholding.

WHEN TO FILE: An S Corporation’s annual West Virginia Tax return is due on or before the fi fteenth day of the third month following the close of the taxable

year. A Partnership’s annual West Virginia Tax return is due on or before the fifteenth day of the third month following the close of the taxable year.

CLAIMING OF EXTENSION PAYMENT: An estimated payment made by fi ling Form PTE-100EXT must be claimed on line 13 of your West Virginia return

(Form PTE-100) and Schedule C.

Make check payable and remit to:

West Virginia Tax Division

Tax Account Administration

PO Box 11751 *B54012201W*

Charleston, WV 25339-1751 B54012201W