Enlarge image

DR 0205 (11/21/22)

COLORADO DEPARTMENT OF REVENUE

Tax.Colorado.gov

*DO=NOT=SEND*

Tax Year Ending Computation of Penalty Due Based on

Underpayment of Colorado Corporate Estimated Tax

Instructions

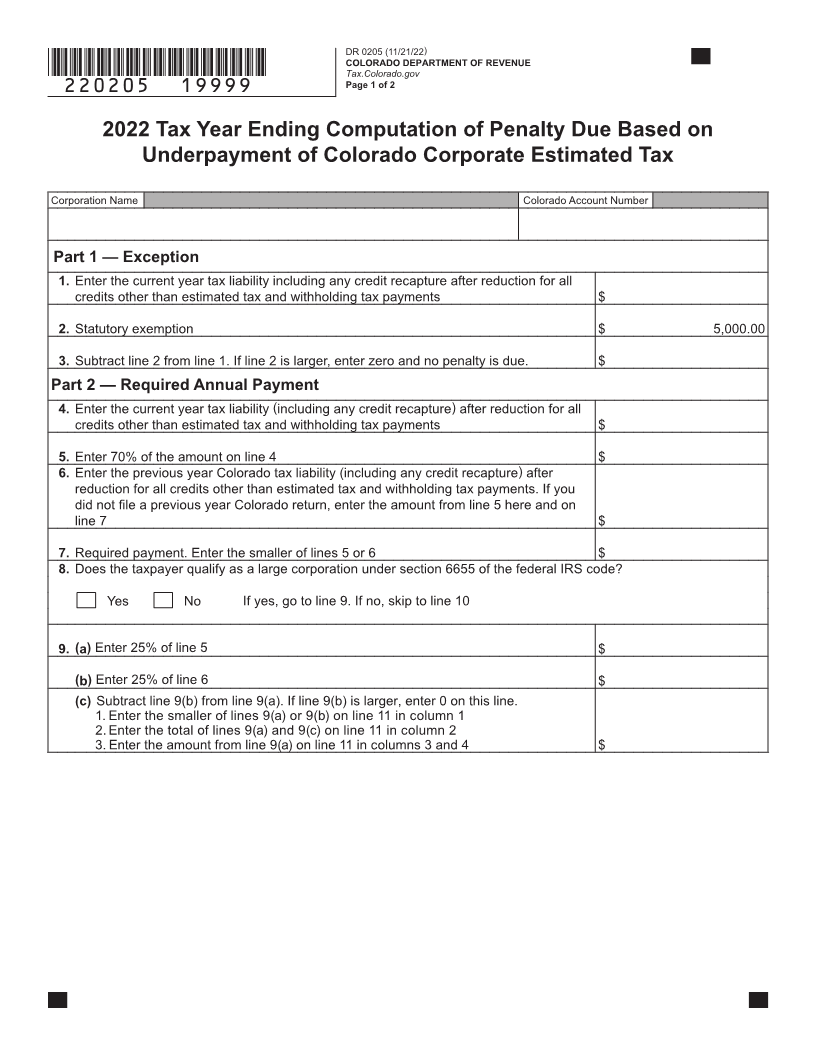

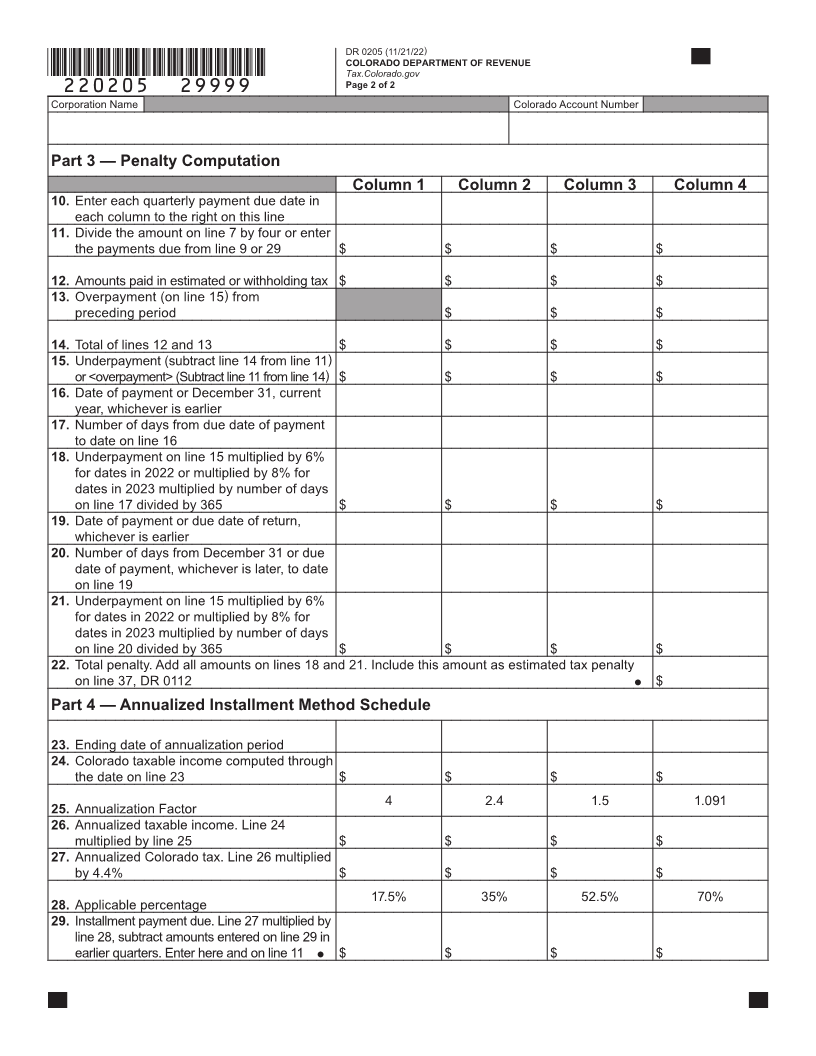

Part 1: Generally you are subject to an estimated tax Part 3: Compute the penalty on lines 10 through 22 of

penalty if your current year estimated tax payments are not DR 0205. Complete each column before going to the next

paid in a timely manner. The estimated tax penalty will not column. The dates to be entered on line 10 are the 15th

be assessed if the Colorado tax liability is less than $5,000. day of the fourth, sixth, ninth and twelfth month of the

Part 2: The required annual amount to be paid is the lesser of: taxable year. Large corporations must complete line 11

based on the computations from line 9 or, if calculating

1. 70% of actual net Colorado tax liability, or

estimated payments using the annualized installment

2. 100% of preceding year's Colorado tax liability only method, line 29.

applies if:

Corporations filing for a short tax year must adjust lines

● The preceding year was 12-month tax year, and 9, 10 and 11 accordingly. For more information about

● The corporation filed a Colorado return, and filing for short tax years, see the Corporate Income Tax

Guide, available at Tax.Colorado.gov

● The corporation is not defined under section 6655 of

the federal IRS code as a large corporation.* Part 4: Taxpayers who do not receive income evenly

during the year may elect to use the annualized income

*Large corporations can base their first quarter estimated

installment method to compute their estimated tax payments

tax payment on 25% of the previous year's tax liability.

if they elected annualized installments or adjusted seasonal

However, future payments must be based on the actual

installments for the payment of their federal income tax.

tax liability for the current tax year and any underpayment

Complete the annualized installment method schedule to

occurring in the first quarter as a result of this estimation

compute the amounts to enter on line 11.

must be paid with the second quarterly payment.

This form should be included with your completed DR 0112 form.

Visit Tax.Colorado.gov for additional information regarding the estimated tax penalty.