- 4 -

Enlarge image

|

Page 4

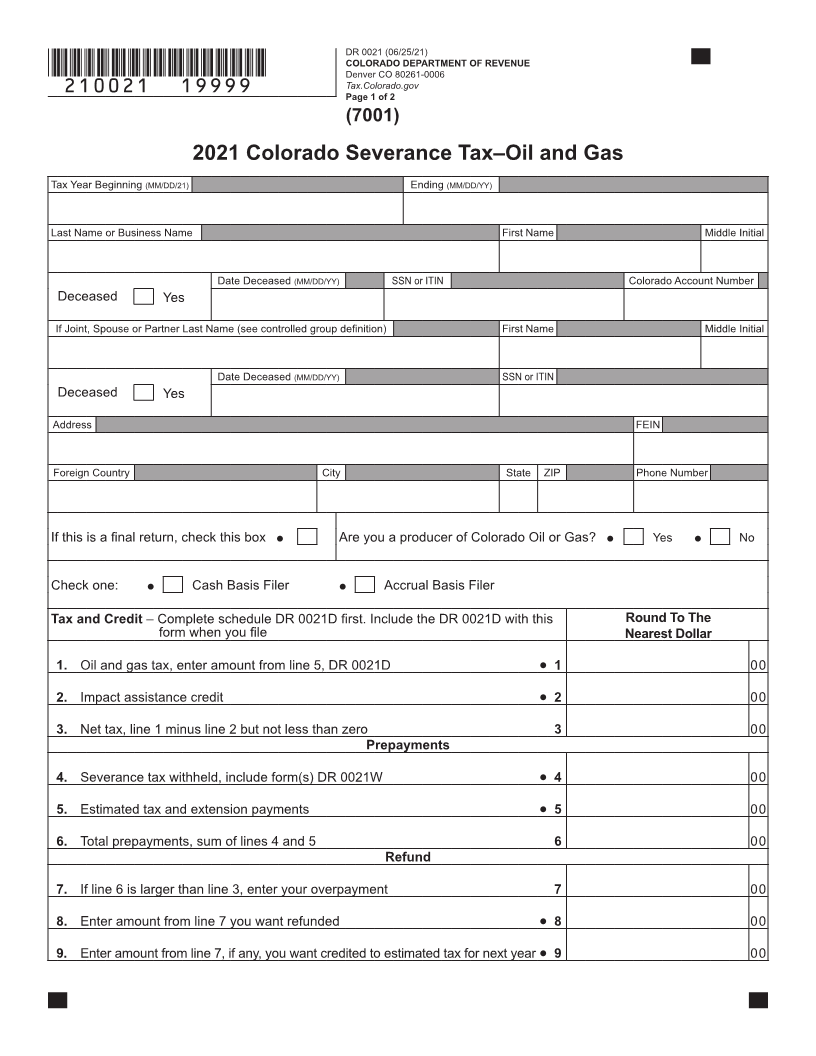

DR 0021 Instructions Line 4 Severance Tax Withheld

Enter the total amount shown on all of your oil and gas

Who Must File withholding statements (DR 0021W) as Colorado severance

Every individual, corporation, business trust, limited tax withheld. Add all amounts, then round to the nearest

partnership, LLC, partner in a general partnership, dollar. Be sure to include your DR 0021W forms with your

association, estate, trust or any other legal entity that return; missing DR 0021Ws will delay your refund. Do not

received income from oil and gas produced in Colorado must claim credit for conservation tax or ad valorem taxes

file a severance tax return. The return must be made for the on this line.

same tax year used for federal income tax purposes and is

Line 5 Estimated Tax and Extension Payments

due on or before the 15th day of the fourth month following Enter the total amount of your estimated tax and extension

the end of the taxable year. See General Information section payments made for the taxable year.

for exception. If you are an oil and gas producer you must

complete the DR 0021PD and retain for your records. Refund or Balance Due

Controlled group: corporations, family group, Line 7 Overpayment

or other type of group Subtract line 3 from line 6 and enter the difference on line 7.

In the case of a controlled group of corporations as Line 8 Refund

defined in section 613A of the Internal Revenue Code Enter the amount from line 7 that you wish to have refunded.

where more than one member of the group is subject to The Department can deposit your refund directly into your

the severance tax, the tax must be jointly computed and account at a U.S. bank or other financial institution (such as

the severance tax return must be jointly filed under the a mutual fund, brokerage firm, or credit union) in the United

name of the principal taxpaying corporation. DR 0021AS, States or the Department can send you a refund check.

available at Tax.Colorado.gov, must be included.

Line 9 Refund Applied to Future Period

Joint Returns Enter on line 9 the amount of overpayment, if any, you wish

When more than one member of a family is subject to the credited to estimated severance tax payment for next year.

severance tax, they shall compute the severance tax on one

combined return. Note: parties to a Civil Union should refer to Line 10 Tax You Owe

federal tax law to determine the correct filing status. If line 3 is more than line 6, you have additional tax to pay.

Subtract line 6 from line 3 and enter the difference on line

Social Security or Colorado Account Number 10. This is the amount you owe. Include with your return a

Individuals must use a Social Security number (SSN) or check or money order in this amount payable to the Colorado

Individual Taxpayer Identification number (ITIN) as the Department of Revenue. Be sure to write your Social

Colorado account number. Business entities must provide Security number or Colorado account number on your

the Colorado account number (CAN) and the Federal check or money order to ensure credit for your payment.

Employer Identification number (FEIN). Whether you are

an individual or a business entity, once you have been Line 11 Interest

assigned a Colorado account number by the Colorado If the return is filed after the due date, interest at the current

Department of Revenue, use the Colorado account number statutory rate will accrue on any balance of tax due until paid.

on all returns and correspondence submitted to the For the current interest rates, refer to publication FYI General

Department. See Tax.Colorado.gov for Privacy Act Notice. 11. The regular rate will apply if we bill you and your payment

is made more than 30 days after you receive your bill. If you

Tax and Credit pay your tax with your return or within 30 days of receiving a

First, complete schedule DR 0021D to calculate your bill, the discounted rate will apply. Enter the amount of late

severance tax. filing interest on line 11.

Line 1 Oil and Gas Severance Tax Line 12 Penalty

Enter your net tax from line 5 of schedule DR 0021D. The penalty on any late filed return with a balance of tax due

is $30 or 30% of the balance of tax due, whichever is greater.

Line 2 Impact Assistance Credit Enter the amount of late filing penalty on line 12.

A credit against the severance tax is allowed with respect

to contributions to local government that are deemed to be Line 13 Estimated Tax Penalty

necessary because of a new severance operation or the Corporations that underpay the estimated tax must enter the

increase in production at an existing operation. The amount penalty due from the DR 0206.

of the credit must be certified by the Executive Director of the

Department of Local Affairs. Enter your impact assistance Be sure to sign your return! If filing a joint return, both

credit for the year on line 2. parties must sign.

To ensure proper processing, please include your

Line 3 Net Tax account number on the return.

Subtract line 2 from line 1, and enter the difference on line 3.

If line 2 is larger than line 1, enter zero.

|