Enlarge image

Illinois Department of Revenue

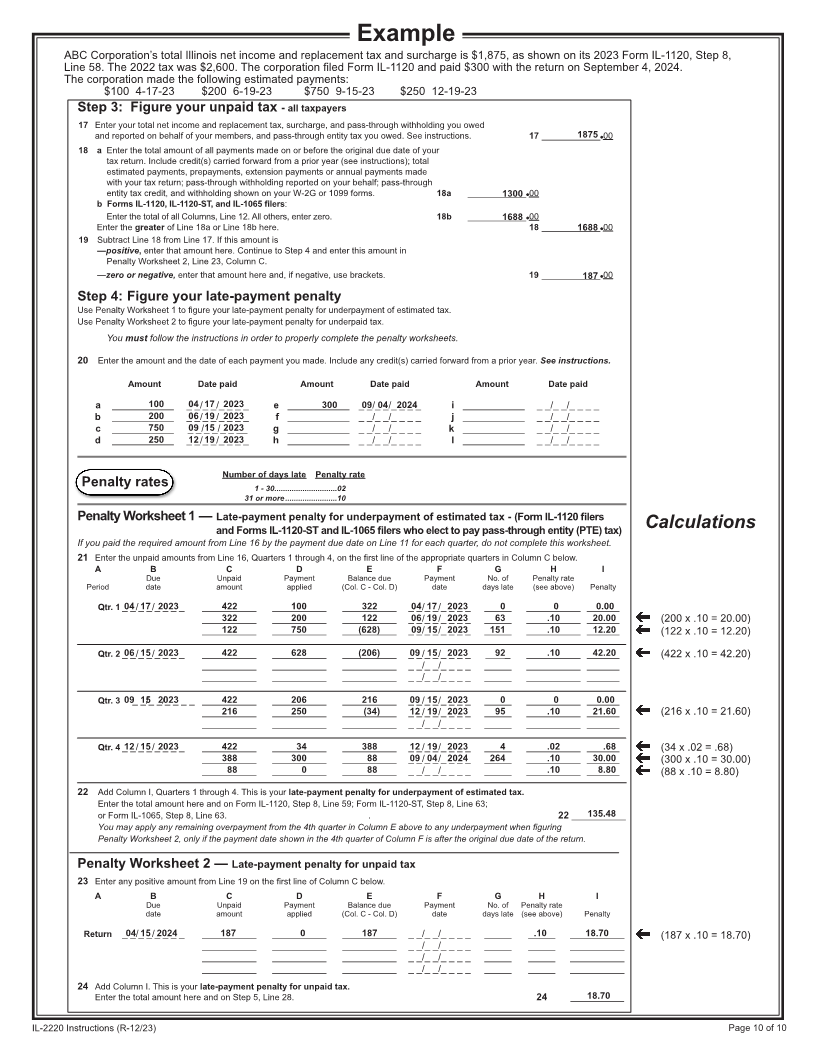

IL-2220 Instructions 2023

General Information

What is the purpose of this form?

This form allows you to calculate penalties you may owe if you did not

• make timely estimated payments,

• pay the tax you owe by the original due date, or

• file a processable return by the extended due date.

Note: The late-payment penalty for underpayment of estimated tax is based on the tax shown due on your original return.

Do not use the tax shown on an amended return filed after the extended due date of the return to compute your required

installments in Step 2.

In addition, this form must be used if your income was not received evenly throughout the year and you choose to annualize

your income. The annualized income installment method may be able to lower or eliminate the amount of your required

installments.

To use the annualized income installment method complete Form IL-2220, Computation of Penalties for Businesses, including

the annualization worksheet in Step 6. See the specific instructions for Step 6 for more information. If you fail to follow these

instructions, we may calculate your late-payment penalty for underpayment of estimated tax based on four equal installments.

Note: Check the box in Step 1 of your return and attach Form IL-2220 to your return if you are annualizing your income.

Should I round?

You must round the dollar amounts on Form IL-2220 to whole-dollar amounts. To do this, you should drop any amount less than

50 cents and increase any amount of 50 cents or more to the next higher dollar.

Do I need to complete this form if I owe penalties?

No, you do not need to complete this form if you owe penalties. We encourage you to let us figure your penalties and send you

a bill instead of completing and filing this form yourself. If you let us figure your penalties, complete your return as usual and do

not attach Form IL-2220.

You must complete this form if you are using the annualized income installment method for late-payment penalty for

underpayment of estimated tax in Step 6.

For more information, see Publication 103, Penalties and Interest for Illinois Taxes. To receive a copy of this publication, visit

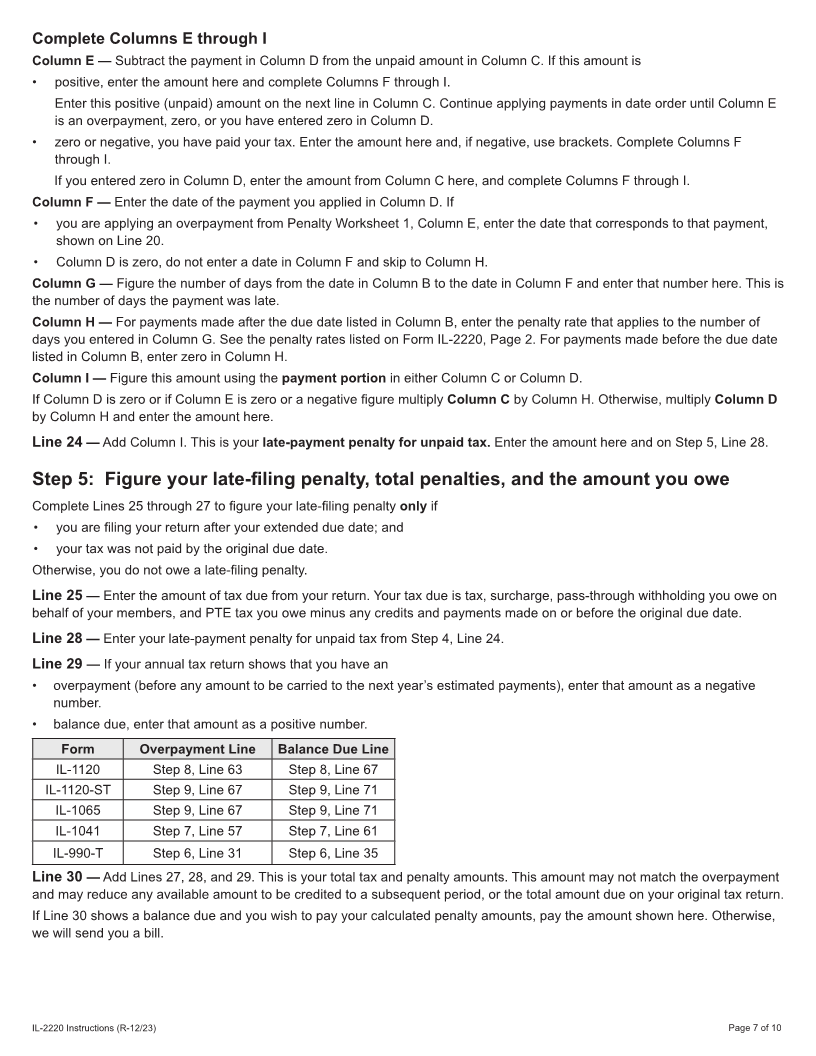

our website at tax.illinois.gov.

What is late-payment penalty?

A late-payment penalty is assessed when you fail to pay the tax you owe by the due date. This penalty could result from two

different underpayment situations and is assessed at either 2 percent or 10 percent of the unpaid liability based on the number

of days the payment is late. The penalty rates used on this form are for returns due on or after January 1, 2005. For returns

due before January 1, 2005, see Publication 103, Penalties and Interest for Illinois Taxes.

You will be assessed a late-payment penalty for unpaid tax if you do not pay the total tax you owe by the original due date of

the return. An extension of time to file your return does not extend the amount of time you have to make your payment.

You will be assessed a late-payment penalty for underpayment of estimated tax if you were required to make estimated tax

payments and failed to do so, or failed to pay the required amount by the payment due date.

Note: If in the previous taxable year you filed a short year return or a return showing no liability, you may still owe the

late-payment penalty for underpayment of estimated tax. See the specific instructions for details.

You do not owe the late-payment penalty for underpayment of estimated taxes if

• you are filing Form IL-1120, Corporation Income and Replacement Tax Return, and

• you were not required to file Form IL-1120 for last year; or

• your current year’s tax liability (Form IL-1120, Step 8, Line 58 minus Lines 61c, 61d, and 61e) is $400 or less; or

• you made timely estimated installment payments equaling at least 90 percent of this year’s tax liability or 100 percent of

the prior year’s tax liability (provided you reported a tax liability in the prior year and it was not a short taxable year).

• you are filing Form IL-1120-ST or Form IL-1065 and

• you were not required to file Form IL-1120-ST or Form IL-1065 last year; or

• you did not elect to pay pass-through entity (PTE) tax this year; or

IL-2220 Instructions (R-12/23) Printed by the authority of the state of Illinois - electronic only - one copy. Page 1 of 10