Enlarge image

Illinois Department of Revenue

2023 Schedule 1299-A Instructions

General Information

Complete this schedule if you are filing Form IL-1065, Partnership Replacement Tax Return or Form IL-1120-ST, Small Business Corporation

Replacement Tax Return and are entitled to any of the credits listed on Schedule 1299-I or any of the following subtractions:

• Dividends from river edge redevelopment zones

• Dividends from foreign trade zones (or sub-zones)

• Contribution to a zone organization (Form IL-1120-ST filers only)

• Interest income from a loan secured by river edge redevelopment zone or high impact business property (Form IL-1120-ST financial

organizations only)

If you are filing an Illinois combined unitary return, complete one Illinois Schedule 1299-A for the entire group. For each credit, you will need

to complete at least one row on Schedule 1299-A, Step 3 for each unitary group member who received the credit. If a specific unitary member

has received multiple, separate amounts of the same type of credit repeatedly over multiple tax years, complete multiple rows for that

member and that credit on Schedule 1299-A, Step 3, one row for each tax year in which a separate amount was received.

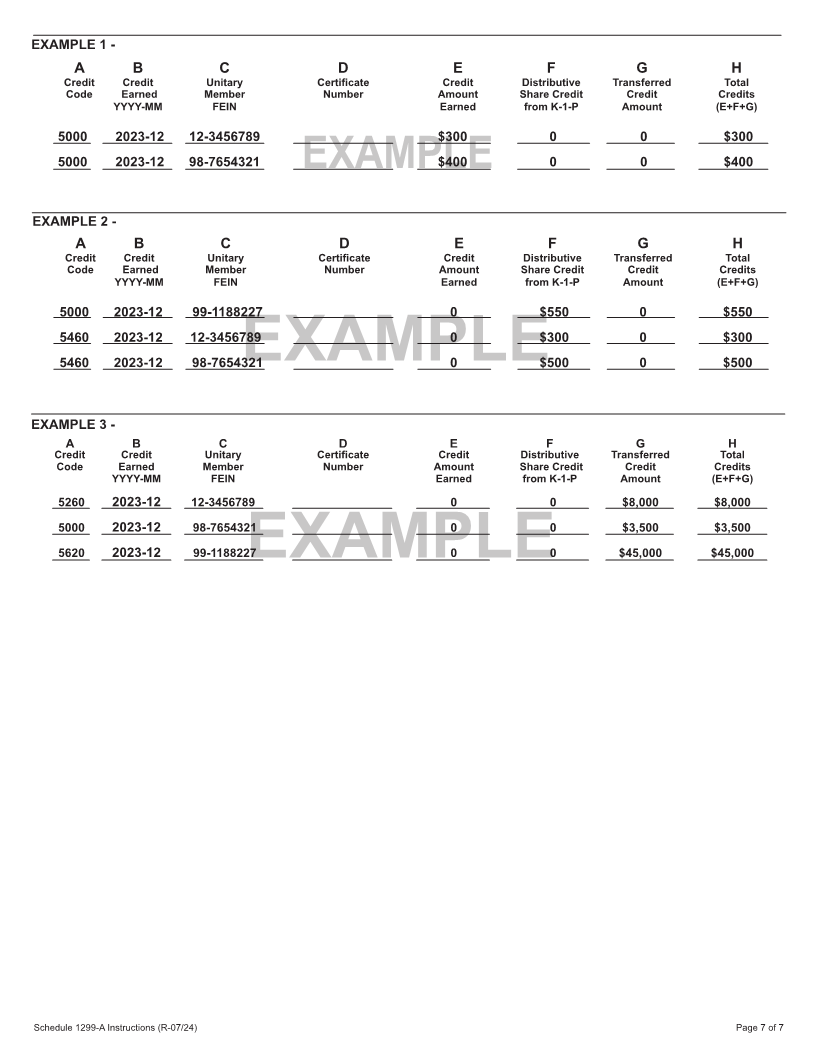

For example, unitary group member A (FEIN 12-3456789) earned $300 of Film Production Services credit during the tax year ending

12/31/23. Member B (FEIN 98-7654321) earned $400 of Film Production Services credit during the year ending 12/31/23. Complete

Schedule 1299-A, Step 3 as follows:

• enter “5000” in Column A, “2023-12” in Column B, “12-3456789” in Column C, and “$300” in Columns E and H

• enter “5000” in Column A, “2023-12” in Column B, “98-7654321” in Column C, and “$400” in Columns E and H

See Example 1 on Page 7.

What must I attach?

If applicable, you must attach

• Schedules K-1-P, Partner’s or Shareholder’s Share of Income, Deductions, Credits, and Recapture, received from a partnership or

S corporation,

• certificates issued by the Illinois Department of Commerce and Economic Opportunity (DCEO),

• certificates issued by the Illinois Department of Natural Resources (DNR),

• certificates issued by the Illinois Department of Agriculture (IDOA),

• certificates issued by the Illinois Department of Human Services (DHS),

• proof that credit was issued by the Illinois Housing Development Authority or the City of Chicago, and

• any other documents, including transfer documentation, required by the Illinois Department of Revenue (IDOR) and noted in these

instructions or Schedule 1299-I.

Note: Specific information about what to attach to your Schedule 1299-A can be found in Schedule 1299-I, Income Tax Credits Information

and Worksheets.

Failure to follow these instructions and attach required documentation will result in one or more of the following: a delay in the

processing of your return, processing delays for your partners or shareholders, the disallowance of the credit, or the issuance of

correspondence from IDOR. You also may be required to submit further information to support your filing.

Should I round?

You must round the dollar amounts on Schedule 1299-A to whole-dollar amounts. To do this, you should drop any amount less than 50 cents

and increase any amount of 50 cents or more to the next higher dollar.

What if I need additional assistance or forms?

• For assistance, forms, or schedules, visit our website at tax.illinois.gov or scan the QR code provided.

• Write us at:

ILLINOIS DEPARTMENT OF REVENUE

PO BOX 19001

SPRINGFIELD IL 62794-9001

• Call 1 800 732-8866 or 217 782-3336 (TTY at 1 800 544-5304).

• Visit a taxpayer assistance office - 8:00 a.m. to 5:00 p.m. (Springfield office) and 8:30 a.m. to 5:00 p.m.

(all other offices), Monday through Friday.

Schedule 1299-A Instructions (R-07/24) Printed by the authority of the state of Illinois. - electronic only - one copy. Page 1 of 7