Enlarge image

Illinois Department of Revenue

2023 Schedule 1299-I

Income Tax Credits Information and Worksheets

What’s New for 2023?

• Public Act 102-1053 created the Recovery and Mental Health income tax credit (Credit Code 0180) effective for tax years beginning on or

after January 1, 2023.

• Public Act 102-0700 increased the maximum K-12 Instructional Materials and Supplies credit (Credit Code 5740) amount allowed for

Form IL-1040 filers. For tax years beginning on or after January 1, 2023, the maximum credit allowed for a single taxpayer is $500 or

$1000 for taxpayers married, filing jointly.

• No new credits will be allowed for the:

• Agritourism Liability Insurance income tax credit (Credit Code 5440) for tax years ending after December 31, 2023; and

• Invest in Kids credit (Credit Code 5660) for tax years ending after December 31, 2023.

NOTE: These credits may still be carried forward according to their provisions. See each credit’s specific instructions for more information.

• Public Act 103-0009 extended the following income tax credits

• Historic Preservation tax credit (Credit Code 1030) until tax years ending on or before December 31, 2028; and

• New Markets Development tax credit (Credit Code 5500) until tax years ending on or before June 30, 2031.

• Public Act 103-0592 extended the following income tax credits

• Adoption credit (Credit Code 5780) until tax years ending on or before December 31, 2029; and

• Student-Assistance Contributions tax credit (Credit Code 5420) until tax years ending on or before December 31, 2029.

• Public Act 103-0268 created the Hydrogen Fuel Replacement tax credit effective for tax years ending on or after December 31, 2027.

• Public Act 103-0595

• created the Quantum Computing Campuses tax credit (Credit Code 5480) effective for tax years ending on or after June 26, 2024; and

• extended the Research and Development tax credit (Credit Code 5340) until tax years ending on or before December 31, 2031.

General Information

If you earned any of the following income tax credits:

• TECH-PREP Youth Vocational Programs,

• Dependent Care Assistance Program,

• Film Production Services,

• Employee Child Care (Corporate filers only),

• Enterprise Zone Investment,

• Enterprise Zone Construction Jobs,

• High Impact Business Construction Jobs,

• High Impact Business Investment,

• REV Illinois Investment,

• Affordable Housing Donations,

• Economic Development for a Growing Economy (EDGE),

• New Construction EDGE,

• Research and Development,

• Wages Paid to Ex-Felons,

• Student-Assistance Contributions,

• Angel Investment,

• Quantum Computing Campuses,

• New Markets Development,

• River Edge Historic Preservation,

• River Edge Construction Jobs,

• Live Theater Production,

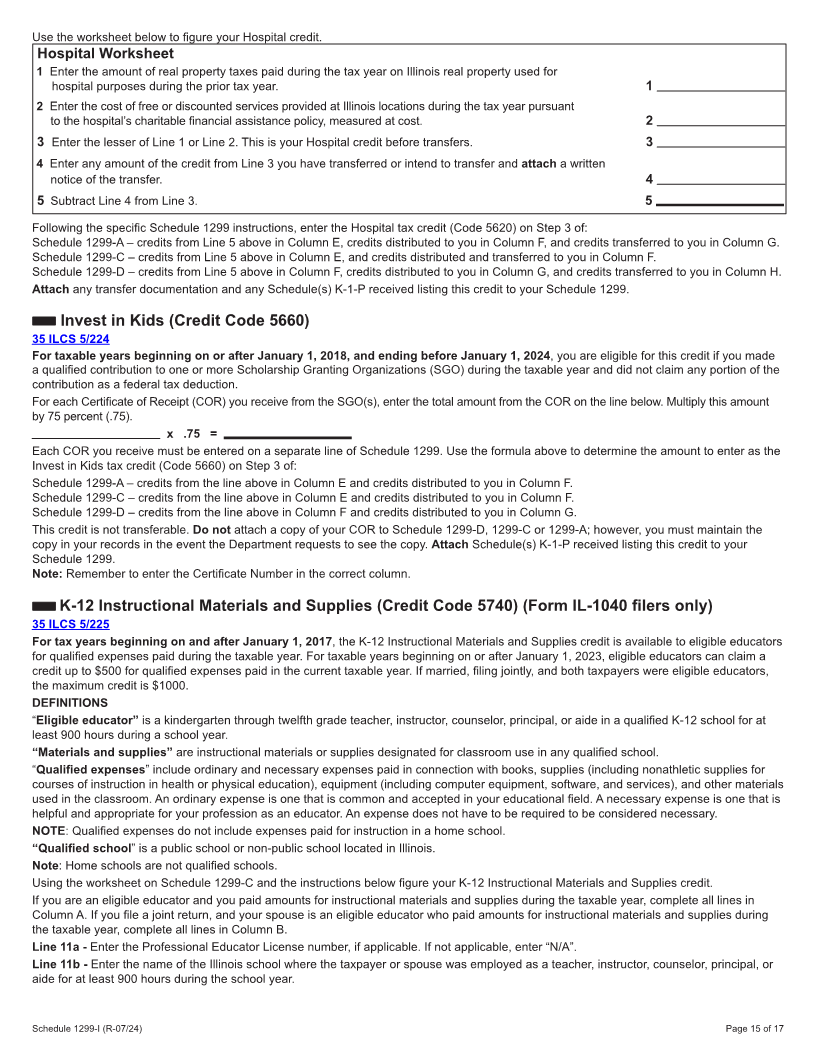

• Hospital,

• Invest in Kids,

• K-12 Instructional Materials and Supplies (Form IL-1040 filers),

• Adoption (Form IL-1040 filers),

• Data Center Construction Employment ,

• Historic Preservation,

• Apprenticeship Education Expense,

• Agritourism Liability Insurance,or

• Recovery and Mental Health,

Schedule 1299-I (R-07/24) Printed by the authority of the state of Illinois - electronic only - one copy.Page 1 of 17