- 2 -

Enlarge image

|

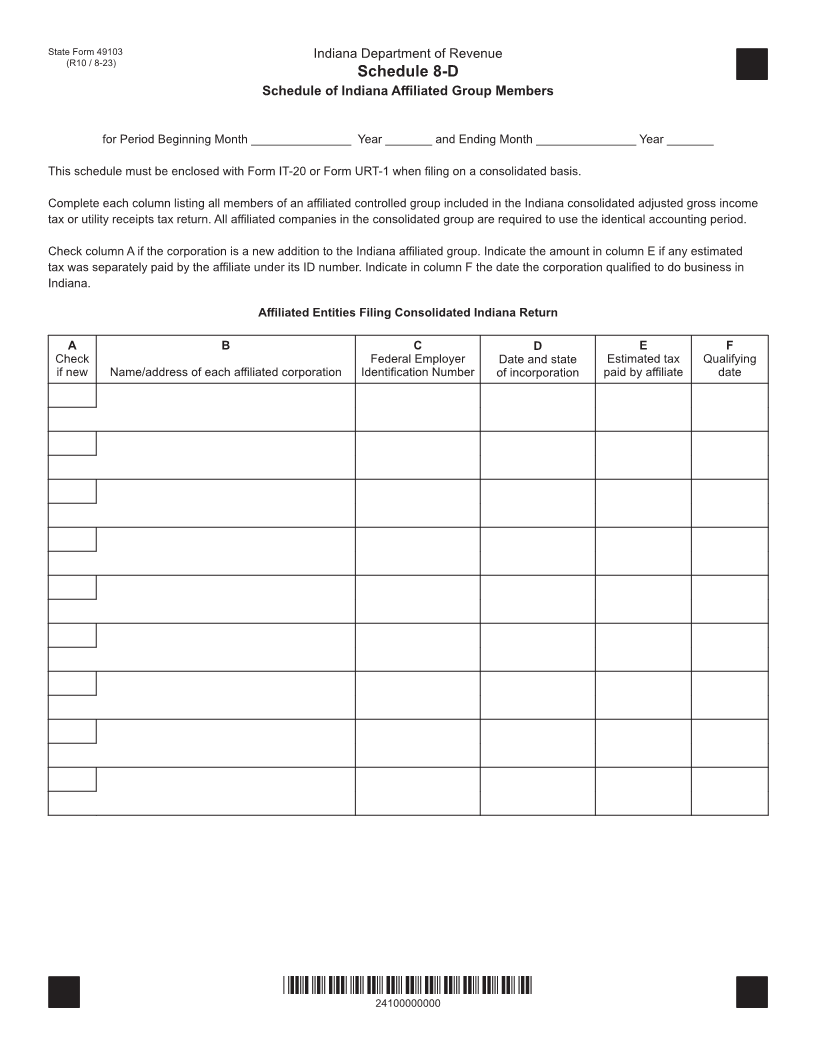

Instructions for Completing Schedule 8-D

Who May File a Consolidated Tax Return Example:

An election must be made by an affiliated group wishing to file (1) Corporation A owns 80% of the voting stock

a consolidated income tax return. An annual return, including of Corporation B. Corporation B owns 80% of

Schedule 8-D or an acceptable substitute schedule, is deemed Corporation C. Corporations A, B, and C are

an election to file a consolidated return by the corporations members of an affiliated group.

listed in the return. Prior permission from the department to file (2) Corporation A owns 80% of Corporation B.

a consolidated return is not necessary. However, an affiliated Corporation A also owns 80% of Corporation C.

group must obtain permission in writing from the department Corporations A, B, and C are members of an

to discontinue filing on a consolidated basis. In such a case, affiliated group.

the group must make a separate application showing good

cause why the filing change should be permitted on or before Each member of an affiliated group is deemed affiliated with

the date the returns are filed. The request for permission to every other member. Brother-sister corporations (having a

discontinue filing consolidated must include the reasons for common owner that is not a parent corporation but themselves

desiring the discontinuance and should be addressed to: owning no stock in each other) do not satisfy the 80%

ownership requirement and are therefore not permitted to file

Indiana Department of Revenue a consolidated return.

Tax Policy Division

100 N Senate Ave, N248, MS 102 Liability of Each Corporate Member for Returns and Tax

Indianapolis, IN 46204-2253 The fact that a certain member corporation is designated

and approved to make the consolidated return for the group

Adjusted Gross Income Tax Act will not relieve any member of liability for filing the return and

An affiliated group (as defined under I.R.C. Sec. 1504) has paying tax for the group. The group and each member thereof

the privilege of filing a consolidated adjusted gross income is jointly and severally liable. The corporation chosen to file

tax return as provided in Indiana Code (IC) 6-3-4-14. The the affiliated group's first consolidated return will continue

Indiana consolidated adjusted gross income tax return must to file the return and pay the tax due with the return unless

include any member of the affiliated group having income or permission is granted by the department to change filing

loss attributed to Indiana during the year. members.

Utility Receipts Tax Act Enclose completed Schedule 8-D when filing a consolidated

The utility receipts tax was repealed effective July 1, tax return with Form IT-20 or Form URT-1.

2022. However, this form may be used to file or amend a

consolidated utility receipts tax returns for tax years that

include periods prior to that date.

Corporations may file a consolidated utility receipts tax

return if they are incorporated or qualified to do business in

Indiana, are affiliated as defined in IC 6-2.3-6-5, and elect

to file a consolidated return at the time the first annual return

is filed. Affiliated for utility receipts tax purposes means 1

corporation owns at least 80% of the voting stock of another

corporation, exclusive of directors' qualifying shares. An

affiliated group is a group of such corporations linked together

by the 80% ownership of 1 with another. This definition does

not include an S corporation.

*24100000000*

24100000000

|