Enlarge image

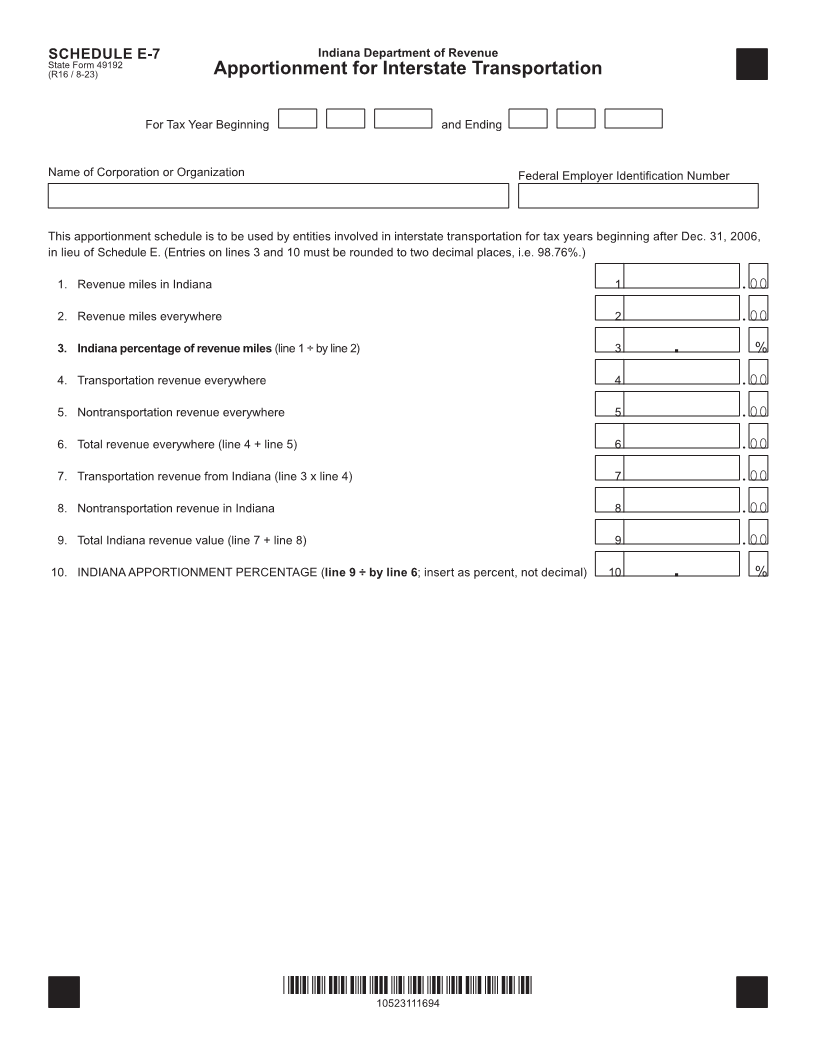

SCHEDULE E-7 Indiana Department of Revenue

State Form 49192

(R16 / 8-23) Apportionment for Interstate Transportation

For Tax Year Beginning and Ending

Name of Corporation or Organization Federal Employer Identification Number

This apportionment schedule is to be used by entities involved in interstate transportation for tax years beginning after Dec. 31, 2006,

in lieu of Schedule E. (Entries on lines 3 and 10 must be rounded to two decimal places, i.e. 98.76%.)

1. Revenue miles in Indiana 1 .00

2. Revenue miles everywhere 2 .00

3. Indiana percentage of revenue miles (line 1 ÷ by line 2) 3 . %

4. Transportation revenue everywhere 4 .00

5. Nontransportation revenue everywhere 5 .00

6. Total revenue everywhere (line 4 + line 5) 6 .00

7. Transportation revenue from Indiana (line 3 x line 4) 7 .00

8. Nontransportation revenue in Indiana 8 .00

9. Total Indiana revenue value (line 7 + line 8) 9 .00

10. INDIANA APPORTIONMENT PERCENTAGE (line 9 ÷ by line 6; insert as percent, not decimal) 10 . %

*10523111694*

10523111694