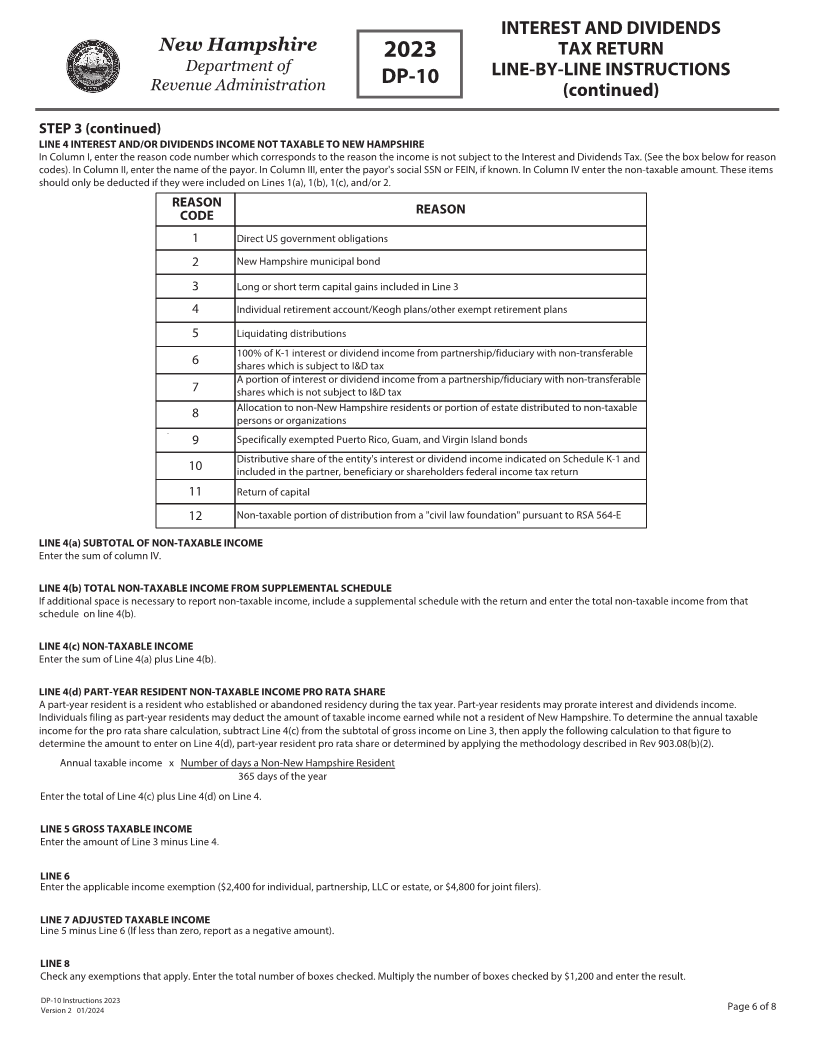

Enlarge image

New Hampshire INTEREST AND DIVIDENDS

2023

Department of TAX RETURN

Revenue Administration DP-10

GENERAL INSTRUCTIONS

WHO AND WHAT IS TAXABLE

Taxable income is income received from interest and dividends during the tax year prior to the assessment date by:

(a)Individuals who are inhabitants or residents of this state for any part of the taxable year whose gross interest and dividend income from all sources, including

income from a qualified investment company pursuant to RSA 77:4, V, exceeds $2,400 during the taxable period.

Note:

- Income received by trusts and foundations treated as grantor trusts under Section 671 of the United States Internal Revenue Code shall be included in the

return of their grantor, to the extent that the grantor is an inhabitant or resident of New Hampshire.

- Income reported by, and taxed federally as interest or dividends to, a trust or foundation beneficiary shall be included as interest or dividends in the return of

such beneficiary, to the extent that the beneficiary is an individual inhabitant or resident of New Hampshire.

(b) Partnerships, Limited Liability Companies (LLCs), and Associations, the beneficial interest in which is not represented by transferable shares, whose gross

interest and dividend income from all sources exceeds $2,400 during the taxable year, but not including a qualified investment company as defined in RSA 77-A:1,

XXI, or a trust comprising a part of an employee benefit plan, as defined in the Employee Retirement Income Security Act of 1974, Section 3.

(c) Executors deriving their appointment from a court of this state whose gross interest and dividend income from all sources exceeds $2,400 during the taxable

year.

WHO MUST FILE A RETURN

INDIVIDUALS Individuals who are residents or inhabitants of New Hampshire for any part of the tax year must file if they received more than $2,400 of gross interest

and/or dividend income for a single individual or $4,800 of such income for a married couple filing a joint New Hampshire return. (Part year residents see below.)

JOINT FILERS To ensure your payments are credited to your account, the sequence of names and social security numbers must be consistent on all Interest

and Dividends Tax estimates, extensions and returns.

PARTNERSHIPS, LLCs, AND ESTATES See separate tables on pages 6 and 7 of these instructions regarding "WHO" and “WHAT” is taxable.

NEW HAMPSHIRE RESIDENT/INHABITANT To determine if you are a New Hampshire resident/inhabitant, refer to Rev 902.01, wherein an individual's intent to

establish residency by an ongoing physical presence within New Hampshire which is not transitory in nature, shall be evidenced by the following factors:

• Maintaining a home or other living quarters in New Hampshire;

• Spending a greater percentage of time in New Hampshire than in any other state;

• Having family living with them in New Hampshire;

• Advising any federal, state, or local agency that the individual considers herself or himself a resident of New Hampshire;

• Being employed or conducting business activity within New Hampshire or at a place to which the individual can readily commute from New Hampshire; or

• Registering to vote in New Hampshire.

PART YEAR RESIDENT For New Hampshire Interest and Dividends Tax purposes, a “part year resident” is someone who has permanently established residency in New

Hampshire during the year or who has permanently abandoned residency in New Hampshire during the year.

A temporary absence for any length of time does not change your state of residency.

Part year residents shall be liable for the tax upon that portion of income earned when they were a resident of New Hampshire. The taxable portion of income is

determined by multiplying the annual taxable income received by a fraction, the numerator of which shall be the number of days the person was a resident of New

Hampshire and the denominator of which shall be 365 days orby providing convincing evidence. Refer to Rev. 903.08 (b)(2) for details. Part year residents are entitled to

the full $2,400 exemption (or $4,800 for joint filers) and the full amount for the exemptions shown on Line 8 of the return. Part year residents must file a return if, during

the entire year, their gross taxable income was over $2,400 (or over $4,800 for joint filers). Refer to Rev.903.08.

WHEN TO FILE

Calendar Year: If your return is based on a calendar year, it must be postmarked on or before April 15th. If the 15th falls on a weekend or a recognized State holiday, the

return is due on the next business day.

Fiscal Year: If your return is based on a taxable period other than a calendar year, it must be postmarked on or before the 15th day of the fourth month following the end

of your taxable period. If the 15th falls on a weekend or a recognized State holiday, the return is due on the next business day. When reporting an IRS adjustment,

submission must be received within 6 months from the date of final determination.

FORMS SHALL NOT BE FILED BY FAX OR EMAIL

WHERE TO FILE

File on-line using Granite Tax Connect at www.revenue.nh.gov/gtc or mail to NH DRA, PO Box 637, Concord, NH 03302-0637.

EXTENSION TO FILE

If you have paid 100% of the Interest and Dividends Tax determined to be due by the due date of the tax, you will be granted an automatic 7-month extension to file your

New Hampshire Interest & Dividends Tax return. If you meet this requirement, you may file your New Hampshire Interest & Dividends Tax return up to 7 months beyond

the original due date of the return and you will not be subject to the late filing penalty.

Note: An extension of time to file your return is not an extension of time to pay the tax.

If you need to make an additional payment, file a Form DP-59-A Extension along with the payment. File on-line using Granite Tax Connect at www.revenue.nh.gov/gtc or

mail to NH DRA, PO Box 1265, Concord, NH 03302-1265. This application and payment must be postmarked on or before the due date of the tax. Failure to pay 100% of

the tax due by the original due date will result in the assessment of interest and may result in the assessment of penalties. You are not required to attach a copy of your

federal extension to your return. Filing a federal extension does not automatically extend your New Hampshire filing requirements.

DP-10 Instructions 2023 Page 1 of 8

Version 1 2 0 /2024