Enlarge image

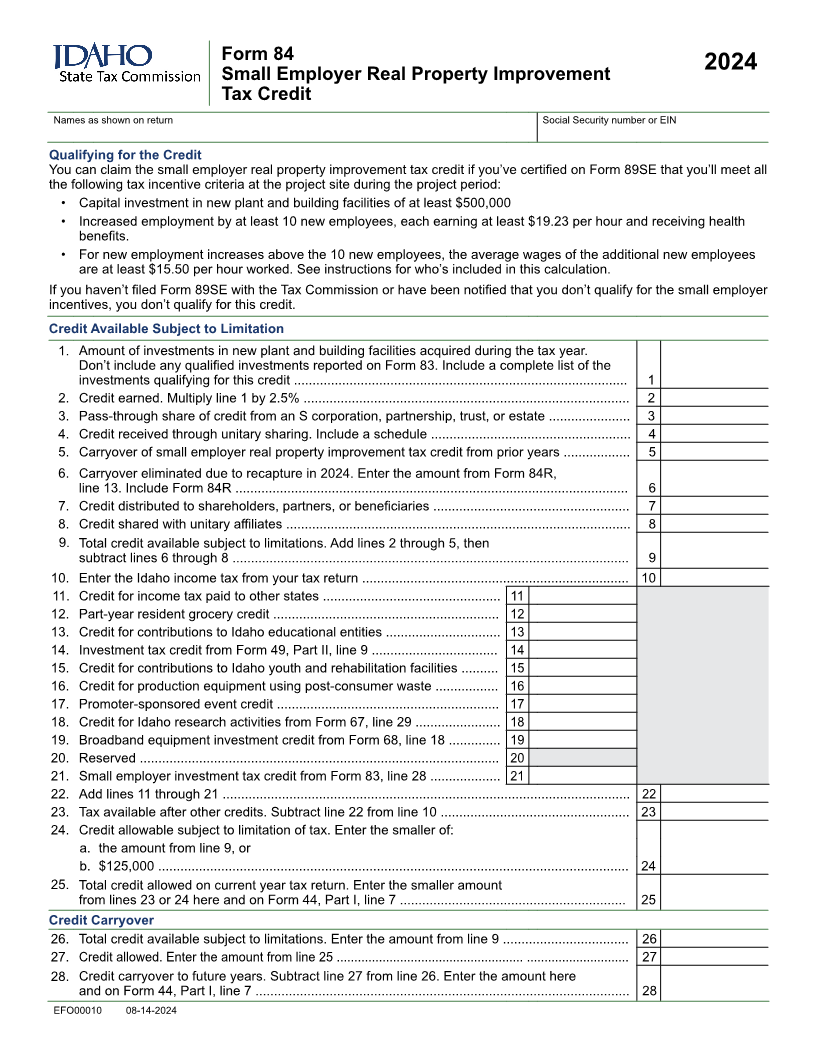

Form 84

2024

Small Employer Real Property Improvement

Tax Credit

Names as shown on return Social Security number or EIN

Qualifying for the Credit

You can claim the small employer real property improvement tax credit if you’ve certified on Form 89SE that you’ll meet all

the following tax incentive criteria at the project site during the project period:

• Capital investment in new plant and building facilities of at least $500,000

• Increased employment by at least 10 new employees, each earning at least $19.23 per hour and receiving health

benefits.

• For new employment increases above the 10 new employees, the average wages of the additional new employees

are at least $15.50 per hour worked. See instructions for who’s included in this calculation.

If you haven’t filed Form 89SE with the Tax Commission or have been notified that you don’t qualify for the small employer

incentives, you don’t qualify for this credit.

Credit Available Subject to Limitation

1. Amount of investments in new plant and building facilities acquired during the tax year.

Don’t include any qualified investments reported on Form 83. Include a complete list of the

investments qualifying for this credit .......................................................................................... 1

2. Credit earned. Multiply line 1 by 2.5% ........................................................................................ 2

3. Pass-through share of credit from an S corporation, partnership, trust, or estate ...................... 3

4. Credit received through unitary sharing. Include a schedule ...................................................... 4

5. Carryover of small employer real property improvement tax credit from prior years .................. 5

6. Carryover eliminated due to recapture in 2024. Enter the amount from Form 84R,

line 13. Include Form 84R .......................................................................................................... 6

7. Credit distributed to shareholders, partners, or beneficiaries ..................................................... 7

8. Credit shared with unitary affiliates ............................................................................................. 8

9. Total credit available subject to limitations. Add lines 2 through 5, then

subtract lines 6 through 8 ........................................................................................................... 9

10. Enter the Idaho income tax from your tax return ........................................................................ 10

11. Credit for income tax paid to other states ................................................ 11

12. Part-year resident grocery credit ............................................................. 12

13. Credit for contributions to Idaho educational entities ............................... 13

14. Investment tax credit from Form 49, Part II, line 9 .................................. 14

15. Credit for contributions to Idaho youth and rehabilitation facilities .......... 15

16. Credit for production equipment using post-consumer waste ................. 16

17. Promoter-sponsored event credit ............................................................ 17

18. Credit for Idaho research activities from Form 67, line 29 ....................... 18

19. Broadband equipment investment credit from Form 68, line 18 .............. 19

20. Reserved .................................................................................................20

21. Small employer investment tax credit from Form 83, line 28 ................... 21

22. Add lines 11 through 21 .............................................................................................................. 22

23. Tax available after other credits. Subtract line 22 from line 10 ................................................... 23

24. Credit allowable subject to limitation of tax. Enter the smaller of:

a. the amount from line 9, or

b. $125,000 ...............................................................................................................................24

25. Total credit allowed on current year tax return. Enter the smaller amount

from lines 23 or 24 here and on Form 44, Part I, line 7 ............................................................. 25

Credit Carryover

26. Total credit available subject to limitations. Enter the amount from line 9 .................................. 26

27. Credit allowed. Enter the amount from line 25 ..................................................... ............................. 27

28. Credit carryover to future years. Subtract line 27 from line 26. Enter the amount here

and on Form 44, Part I, line 7 ..................................................................................................... 28

EFO00010 08-14-2024