Enlarge image

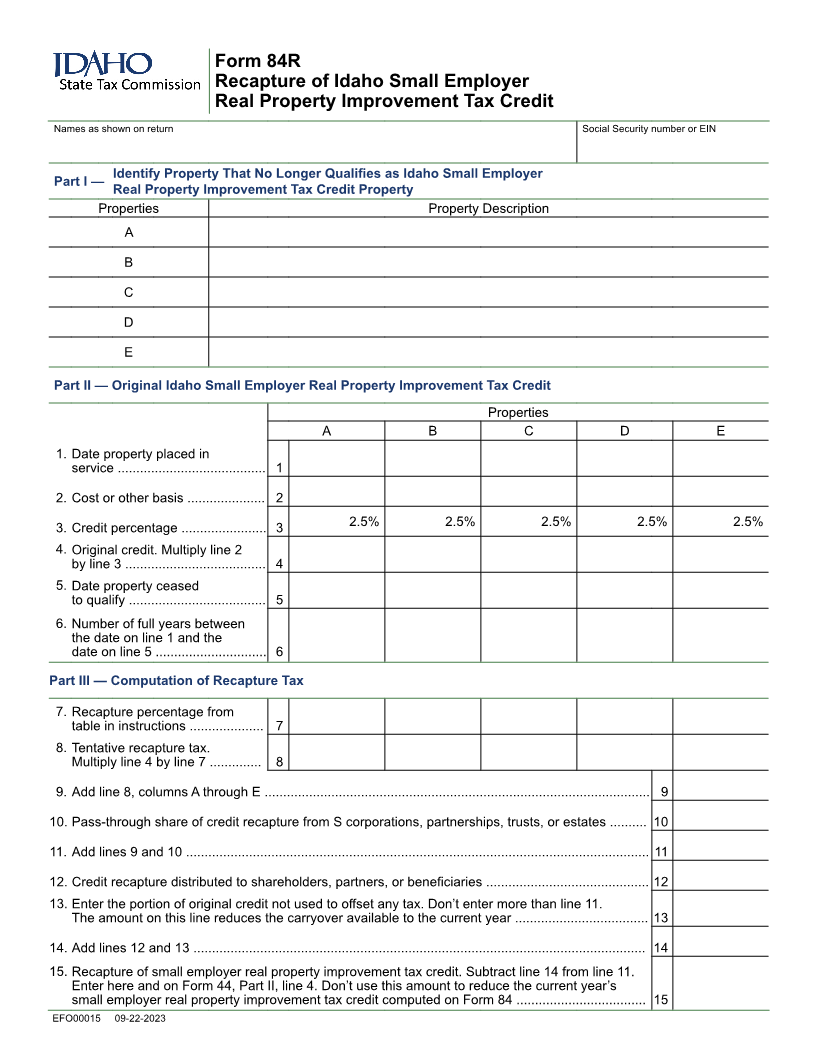

Form 84R

Recapture of Idaho Small Employer

Real Property Improvement Tax Credit

Names as shown on return Social Security number or EIN

Identify Property That No Longer Qualifies as Idaho Small Employer

Part I —

Real Property Improvement Tax Credit Property

Properties Property Description

A

B

C

D

E

Part II — Original Idaho Small Employer Real Property Improvement Tax Credit

Properties

A B C D E

1. Date property placed in

service ........................................ 1

2. Cost or other basis ..................... 2

3. Credit percentage ....................... 3 2.5% 2.5% 2.5% 2.5% 2.5%

4. Original credit. Multiply line 2

by line 3 ...................................... 4

5. Date property ceased

to qualify ..................................... 5

6. Number of full years between

the date on line 1 and the

date on line 5 .............................. 6

Part III — Computation of Recapture Tax

7. Recapture percentage from

table in instructions .................... 7

8. Tentative recapture tax.

Multiply line 4 by line 7 .............. 8

9. Add line 8, columns A through E ........................................................................................................ 9

10. Pass-through share of credit recapture from S corporations, partnerships, trusts, or estates .......... 10

11. Add lines 9 and 10 ............................................................................................................................. 11

12. Credit recapture distributed to shareholders, partners, or beneficiaries ............................................ 12

13. Enter the portion of original credit not used to offset any tax. Don’t enter more than line 11.

The amount on this line reduces the carryover available to the current year .................................... 13

14. Add lines 12 and 13 .......................................................................................................................... 14

15. Recapture of small employer real property improvement tax credit. Subtract line 14 from line 11.

Enter here and on Form 44, Part II, line 4. Don’t use this amount to reduce the current year’s

small employer real property improvement tax credit computed on Form 84 ................................... 15

EFO00015 09-22-2023