Enlarge image

Vermont Department of Taxes

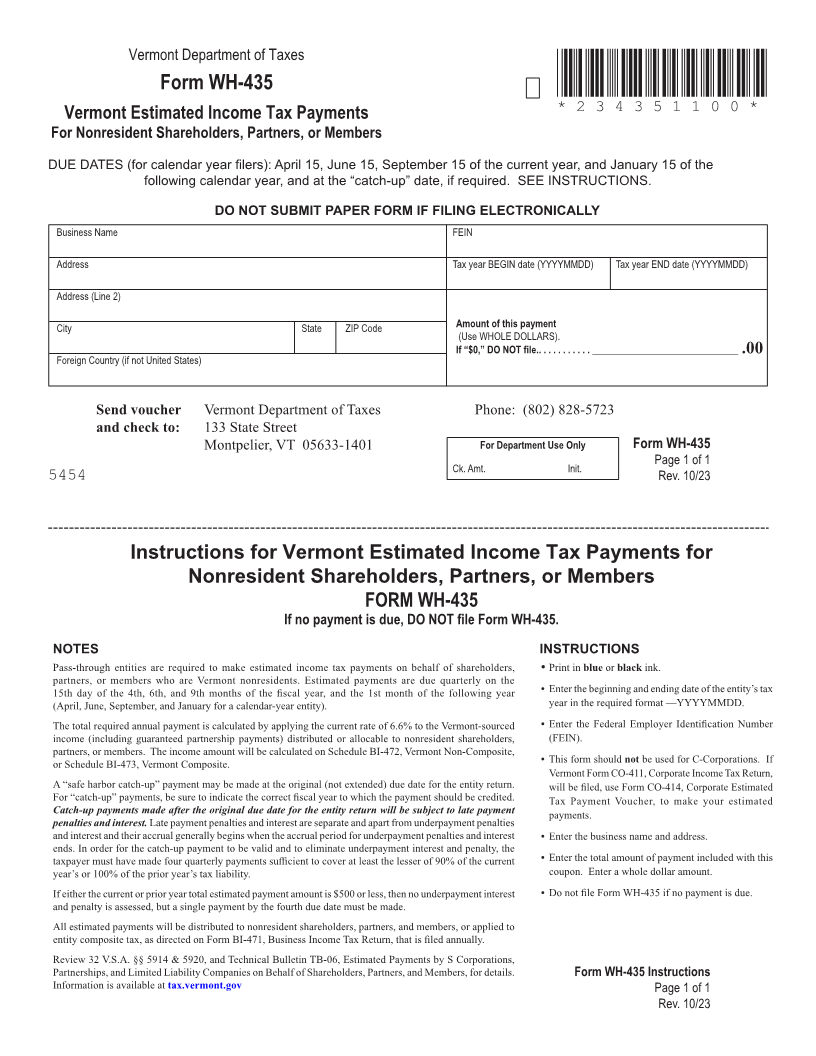

Form WH-435 *234351100*

Vermont Estimated Income Tax Payments *234351100*

For Nonresident Shareholders, Partners, or Members Page 1

DUE DATES (for calendar year filers): April 15, June 15, September 15 of the current year, and January 15 of the

following calendar year, and at the “catch-up” date, if required. SEE INSTRUCTIONS.

DO NOT SUBMIT PAPER FORM IF FILING ELECTRONICALLY

Business Name FEIN

Address Tax year BEGIN date (YYYYMMDD) Tax year END date (YYYYMMDD)

Address (Line 2)

City State ZIP Code Amount of this payment

(Use WHOLE DOLLARS).

If “$0,” DO NOT file. ........... ______________________________ .00

Foreign Country (if not United States)

FORM (Place at FIRST page)

Send voucher Vermont Department of Taxes Phone: (802) 828-5723 Form pages

and check to: 133 State Street

Montpelier, VT 05633-1401 For Department Use Only Form WH-435

Page 1 of 1

Ck. Amt. Init.

5454 Rev. 10/23

1 - 1

Instructions for Vermont Estimated Income Tax Payments for

Nonresident Shareholders, Partners, or Members

FORM WH-435

If no payment is due, DO NOT file Form WH-435.

NOTES INSTRUCTIONS

Pass-through entities are required to make estimated income tax payments on behalf of shareholders, • Print in blue or black ink.

partners, or members who are Vermont nonresidents. Estimated payments are due quarterly on the

15th day of the 4th, 6th, and 9th months of the fiscal year, and the 1st month of the following year • Enter the beginning and ending date of the entity’s tax

(April, June, September, and January for a calendar-year entity). year in the required format —YYYYMMDD.

The total required annual payment is calculated by applying the current rate of 6.6% to the Vermont-sourced • Enter the Federal Employer Identification Number

income (including guaranteed partnership payments) distributed or allocable to nonresident shareholders, (FEIN).

partners, or members. The income amount will be calculated on Schedule BI-472, Vermont Non-Composite,

or Schedule BI-473, Vermont Composite. • This form should not be used for C-Corporations. If

Vermont Form CO-411, Corporate Income Tax Return,

A “safe harbor catch-up” payment may be made at the original (not extended) due date for the entity return. will be filed, use Form CO-414, Corporate Estimated

For “catch-up” payments, be sure to indicate the correct fiscal year to which the payment should be credited. Tax Payment Voucher, to make your estimated

Catch-up payments made after the original due date for the entity return will be subject to late payment payments.

penalties and interest. Late payment penalties and interest are separate and apart from underpayment penalties

and interest and their accrual generally begins when the accrual period for underpayment penalties and interest • Enter the business name and address.

ends. In order for the catch-up payment to be valid and to eliminate underpayment interest and penalty, the

taxpayer must have made four quarterly payments sufficient to cover at least the lesser of 90% of the current • Enter the total amount of payment included with this

year’s or 100% of the prior year’s tax liability. coupon. Enter a whole dollar amount.

If either the current or prior year total estimated payment amount is $500 or less, then no underpayment interest • Do not file Form WH-435 if no payment is due. FORM (Place at LAST page)

and penalty is assessed, but a single payment by the fourth due date must be made. Form pages

All estimated payments will be distributed to nonresident shareholders, partners, and members, or applied to

entity composite tax, as directed on Form BI-471, Business Income Tax Return, that is filed annually.

Review 32 V.S.A. §§ 5914 & 5920, and Technical Bulletin TB-06, Estimated Payments by S Corporations,

Partnerships, and Limited Liability Companies on Behalf of Shareholders, Partners, and Members, for details. Form WH-435 Instructions

Information is available at tax.vermont.gov Page 1 of 1 1 - 1

Rev. 10/23