Enlarge image

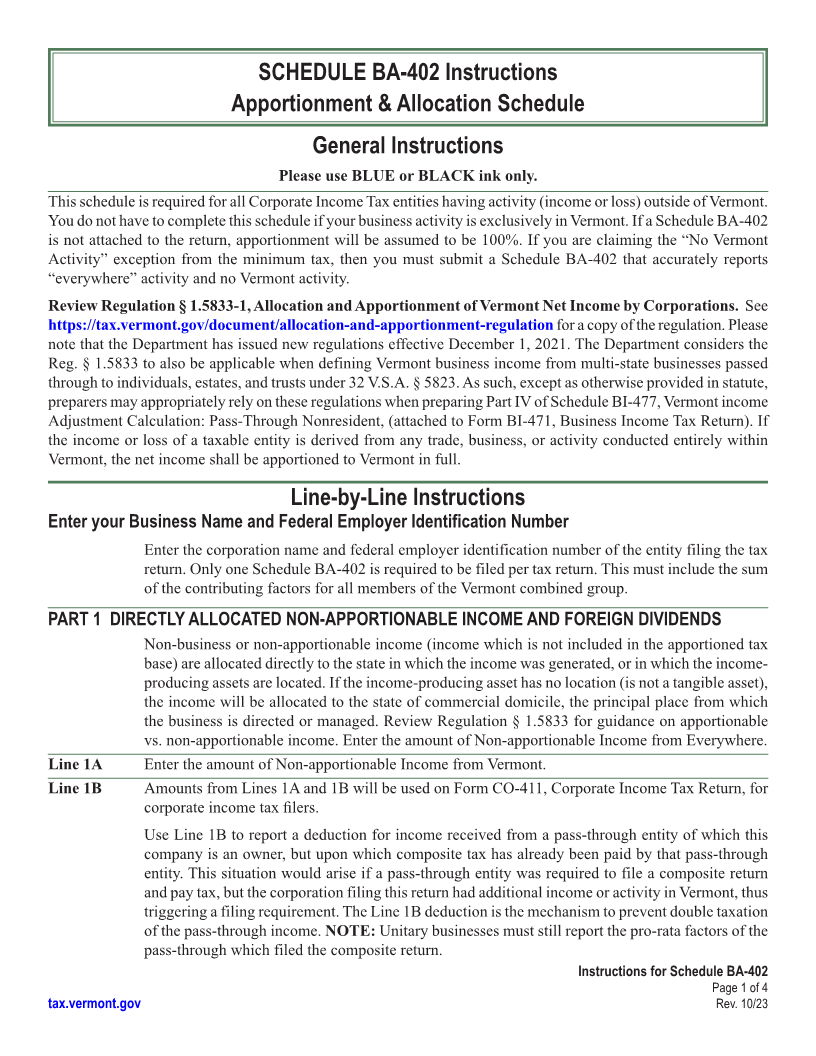

SCHEDULE BA-402 Instructions

Apportionment & Allocation Schedule

Page 1

General Instructions

Please use BLUE or BLACK ink only.

This schedule is required for all Corporate Income Tax entities having activity (income or loss) outside of Vermont.

You do not have to complete this schedule if your business activity is exclusively in Vermont. If a Schedule BA‑402

is not attached to the return, apportionment will be assumed to be 100%. If you are claiming the “No Vermont

Activity” exception from the minimum tax, then you must submit a Schedule BA‑402 that accurately reports

“everywhere” activity and no Vermont activity.

Review Regulation § 1.5833-1, Allocation and Apportionment of Vermont Net Income by Corporations. See

https://tax.vermont.gov/document/allocation-and-apportionment-regulation for a copy of the regulation. Please

note that the Department has issued new regulations effective December 1, 2021. The Department considers the

Reg. § 1.5833 to also be applicable when defining Vermont business income from multi‑state businesses passed

through to individuals, estates, and trusts under 32 V.S.A. § 5823. As such, except as otherwise provided in statute,

INSTR (Place at FIRST page)

preparers may appropriately rely on these regulations when preparing Part IV of Schedule BI‑477, Vermont income Instr. pages

Adjustment Calculation: Pass‑Through Nonresident, (attached to Form BI‑471, Business Income Tax Return). If

the income or loss of a taxable entity is derived from any trade, business, or activity conducted entirely within

Vermont, the net income shall be apportioned to Vermont in full.

1 - 4

Line-by-Line Instructions

Enter your Business Name and Federal Employer Identification Number

Enter the corporation name and federal employer identification number of the entity filing the tax

return. Only one Schedule BA‑402 is required to be filed per tax return. This must include the sum

of the contributing factors for all members of the Vermont combined group.

PART 1 DIRECTLY ALLOCATED NON-APPORTIONABLE INCOME AND FOREIGN DIVIDENDS

Non‑business or non‑apportionable income (income which is not included in the apportioned tax

base) are allocated directly to the state in which the income was generated, or in which the income‑

producing assets are located. If the income‑producing asset has no location (is not a tangible asset),

the income will be allocated to the state of commercial domicile, the principal place from which

the business is directed or managed. Review Regulation § 1.5833 for guidance on apportionable

vs. non‑apportionable income. Enter the amount of Non‑apportionable Income from Everywhere.

Line 1A Enter the amount of Non‑apportionable Income from Vermont.

Line 1B Amounts from Lines 1A and 1B will be used on Form CO‑411, Corporate Income Tax Return, for

corporate income tax filers.

Use Line 1B to report a deduction for income received from a pass‑through entity of which this

company is an owner, but upon which composite tax has already been paid by that pass‑through

entity. This situation would arise if a pass‑through entity was required to file a composite return

and pay tax, but the corporation filing this return had additional income or activity in Vermont, thus

triggering a filing requirement. The Line 1B deduction is the mechanism to prevent double taxation

of the pass‑through income. NOTE: Unitary businesses must still report the pro‑rata factors of the

pass‑through which filed the composite return.

Instructions for Schedule BA-402

Page 1 of 4

tax.vermont.gov Rev. 10/23