Enlarge image

01

0000000000111111111122222222223333333333444444444455555555556666666666777777777788888

1234567890123456789012345678901234567890123456789012345678901234567890123456789012345

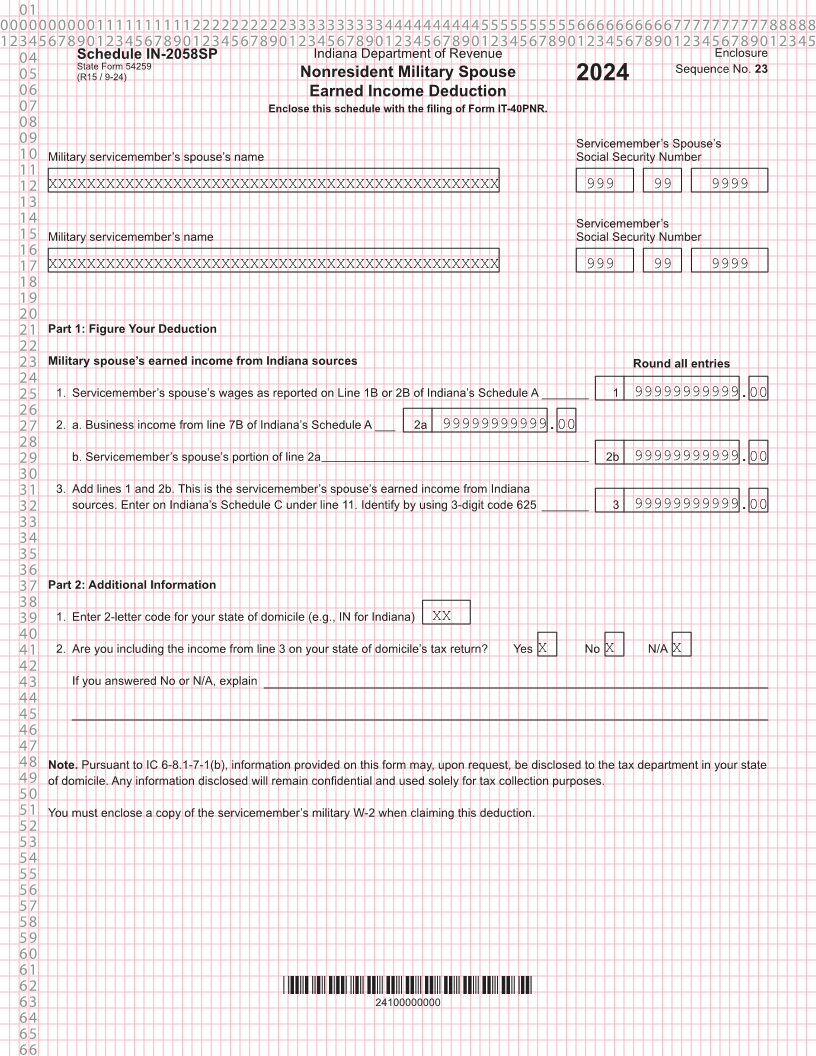

04 Schedule IN-2058SP Indiana Department of Revenue Enclosure

State Form 54259 Sequence No. 23

05 (R15 / 9-24) Nonresident Military Spouse 2024

06 Earned Income Deduction

07 Enclose this schedule with the filing of Form IT-40PNR.

08

09 Servicemember’s Spouse’s

10 Military servicemember’s spouse’s name Social Security Number

11

12 XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX 999 99 9999

13

14 Servicemember’s

15 Military servicemember’s name Social Security Number

16

17 XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX 999 99 9999

18

19

20

21 Part 1: Figure Your Deduction

22

23 Military spouse’s earned income from Indiana sources Round all entries

24

25 1. Servicemember’s spouse’s wages as reported on Line 1B or 2B of Indiana’s Schedule A _______ 1 99999999999.00

26

27 2. a. Business income from line 7B of Indiana’s Schedule A ___ 2a 99999999999.00

28

29 b. Servicemember’s spouse’s portion of line 2a ________________________________________ 2b 99999999999.00

30

31 3. Add lines 1 and 2b. This is the servicemember’s spouse’s earned income from Indiana

32 sources. Enter on Indiana’s Schedule C under line 11. Identify by using 3-digit code 625 _______ 3 99999999999.00

33

34

35

36

37 Part 2: Additional Information

38

39 1. Enter 2-letter code for your state of domicile (e.g., IN for Indiana) XX

40

41 2. Are you including the income from line 3 on your state of domicile’s tax return? Yes X No X N/A X

42

43 If you answered No or N/A, explain

44

45

46

47

48 Note. Pursuant to IC 6-8.1-7-1(b), information provided on this form may, upon request, be disclosed to the tax department in your state

49 of domicile. Any information disclosed will remain confidential and used solely for tax collection purposes.

50

51 You must enclose a copy of the servicemember’s military W-2 when claiming this deduction.

52

53

54

55

56

57

58

59

60

61

62 *24100000000*

63 24100000000

64

65

66