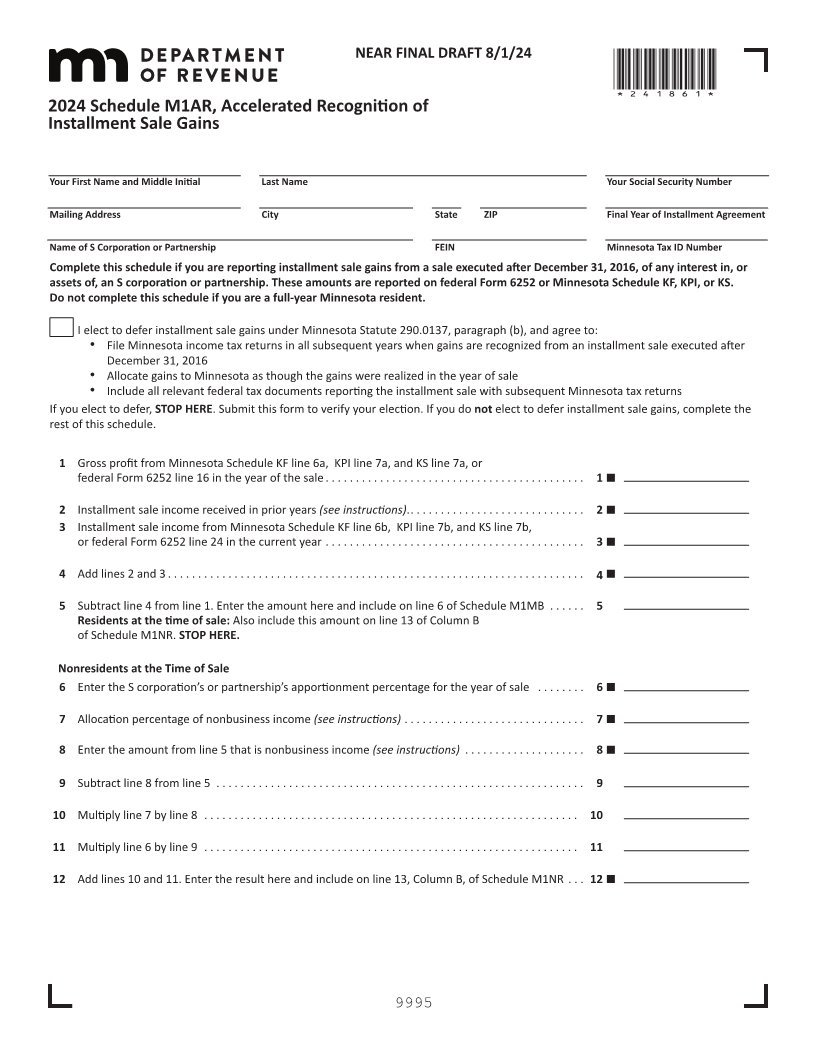

Enlarge image

NEAR FINAL DRAFT 8/1/24

*241861*

2024 Schedule M1AR, Accelerated Recognition of

Installment Sale Gains

Your First Name and Middle Initial Last Name Your Social Security Number

Mailing Address City State ZIP Final Year of Installment Agreement

Name of S Corporation or Partnership FEIN Minnesota Tax ID Number

Complete this schedule if you are reporting installment sale gains from a sale executed after December 31, 2016, of any interest in, or

assets of, an S corporation or partnership. These amounts are reported on federal Form 6252 or Minnesota Schedule KF, KPI, or KS.

Do not complete this schedule if you are a full-year Minnesota resident.

I elect to defer installment sale gains under Minnesota Statute 290.0137, paragraph (b), and agree to:

• File Minnesota income tax returns in all subsequent years when gains are recognized from an installment sale executed after

December 31, 2016

• Allocate gains to Minnesota as though the gains were realized in the year of sale

• Include all relevant federal tax documents reporting the installment sale with subsequent Minnesota tax returns

If you elect to defer, STOP HERE. Submit this form to verify your election. If you do not elect to defer installment sale gains, complete the

rest of this schedule.

1 Gross profit from Minnesota Schedule KF line 6a, KPI line 7a, and KS line 7a, or

federal Form 6252 line 16 in the year of the sale... ...... ..... ....... ..... ..... ...... ..... . 1

2 Installment sale income received in prior years (see instructions).... ...... ..... ....... ..... ... 2

3 Installment sale income from Minnesota Schedule KF line 6b, KPI line 7b, and KS line 7b,

or federal Form 6252 line 24 in the current year ...... ...... ...... ..... ..... ...... ..... .... 3

4 Add lines 2 and 3 ... ...... ..... ....... ..... ..... ...... ..... ...... ...... ..... ....... ... 4

5 Subtract line 4 from line 1. Enter the amount here and include on line 6 of Schedule M1MB .. .... 5

Residents at the time of sale: Also include this amount on line 13 of Column B

of Schedule M1NR. STOP HERE.

Nonresidents at the Time of Sale

6 Enter the S corporation’s or partnership’s apportionment percentage thefor year saleof .. ...... 6

7 Allocation percentage of nonbusiness income (see instructions) ... ...... ..... ....... ..... .... 7

8 Enter the amount from line 5 that is nonbusiness income (see instructions) .... ..... ...... ..... 8

9 Subtract line 8 from line 5 .. ...... ...... ..... ...... ..... ....... ..... ...... ..... ...... .. 9

10 Multiply line 7 by line 8 ..... ...... ..... ..... ...... ...... ..... ...... ...... ..... ...... . 10

11 Multiply line 6 by line 9 ..... ...... ..... ..... ...... ...... ..... ...... ...... ..... ...... . 11

12 Add lines 10 and 11. Enter the result here and include on line 13, Column B, of Schedule M1NR ... 12

9995