Enlarge image

1 1

2 4 6 8 10 12 14 16 18 20 22 24 26 28 30NEAR32 34 DRAFT36 38 8/1/2440 42 44 46 48 50 52 54 56 58 60 62 64 66 68 70 72 74 76 78 80 82 84 86

3 3

4 4

5 5

6 *247301* 6

7 7

8 8

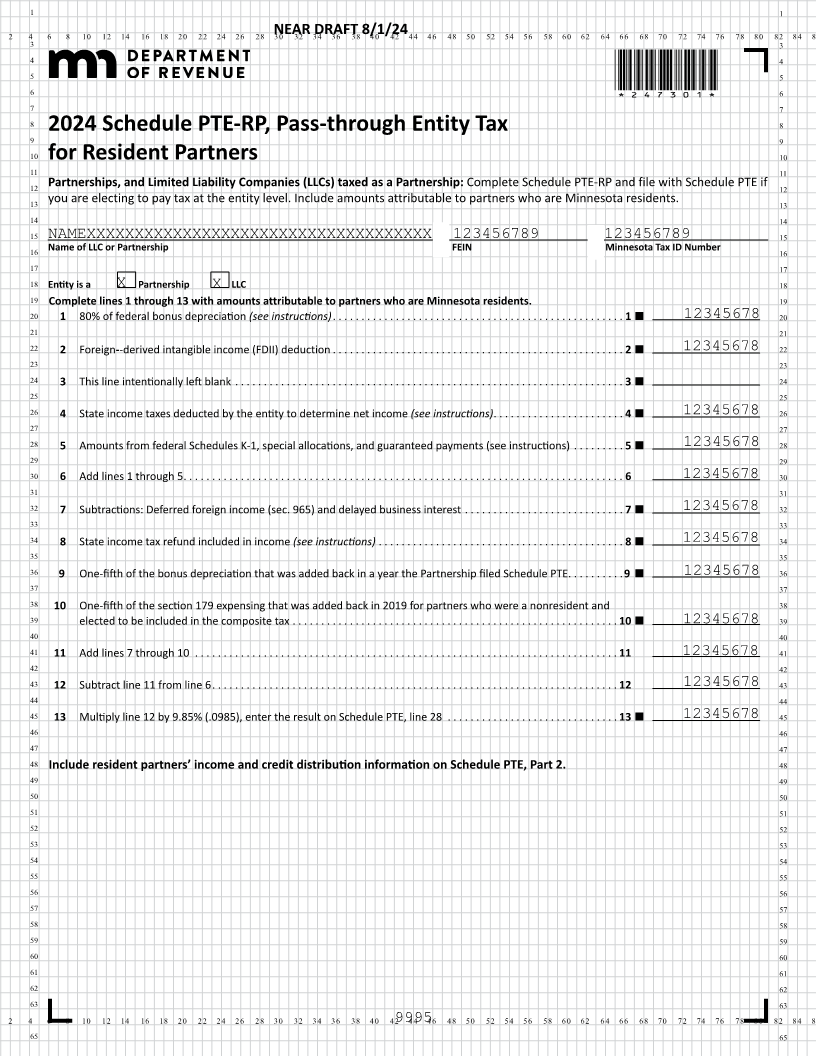

9 2024 Schedule PTE-RP, Pass-through Entity Tax 9

10 for Resident Partners 10

11 11

12 Partnerships, and Limited Liability Companies (LLCs) taxed as a Partnership: Complete Schedule PTE-RP and file with Schedule PTE if 12

13 you are electing to pay tax at the entity level. Include amounts attributable to partners who are Minnesota residents. 13

14 14

15 NAMEXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX 123456789 123456789 15

16 Name of LLC or Partnership FEIN Minnesota Tax ID Number 16

17 17

18 Entity is a X Partnership X LLC 18

19 Complete lines 1 through 13 with amounts attributable to partners who are Minnesota residents. 19

20 1 80% of federal bonus depreciation (see instructions) ... ...... ..... ....... ..... ...... ..... ..... ...... ... 1 12345678 20

21 21

22 2 Foreign--derived intangible income (FDII) deduction ... ...... ..... ....... ..... ...... ..... ..... ...... ... 2 12345678 22

23 23

24 3 This line intentionally left blank . ..... ...... ...... ..... ..... ...... ...... ..... ...... ...... ..... ...... 3 24

25 25

26 4 State income taxes deducted by the entity to determine net income (see instructions) ... ...... ..... ....... .. 4 12345678 26

27 27

28 5 Amounts from federal Schedules K-1, special allocations, and guaranteed payments (see instructions) .... ..... 5 12345678 28

29 29

30 6 Add lines 1 through 5... ...... ..... ...... ...... ..... ...... ..... ...... ...... ..... ...... ...... ..... . 6 12345678 30

31 31

32 7 Subtractions: Deferred foreign income (sec. 965) and delayed business interest ... ...... ..... ...... ...... .. 7 12345678 32

33 33

34 8 State income tax refund included in income (see instructions) ...... ...... ..... ...... ..... ...... ...... ... 8 12345678 34

35 35

36 9 One-fifth of the bonus depreciation that was added back in a year the Partnership filed Schedule PTE... ...... .9 12345678 36

37 37

38 10 One-fifth of the section 179 expensing that was added back in 2019 for partners who were a nonresident and 38

39 elected to be included in the composite tax ..... ..... ...... ..... ...... ...... ...... ...... .... ...... .. 10 12345678 39

40 40

41 11 Add lines 7 through 10 ... ..... ..... ...... ...... ...... ..... ...... ..... ....... ..... ...... ...... ... 11 12345678 41

42 42

43 12 Subtract line 11 from line 6 ... ...... ..... ....... ..... ..... ...... ..... ...... ...... ...... ..... ...... 12 12345678 43

44 44

45 13 Multiply line 12 by 9.85% (.0985), enter the result on Schedule PTE, line 28 . ..... ....... ...... ..... ..... . 13 12345678 45

46 46

47 47

48 Include resident partners’ income and credit distribution information on Schedule PTE, Part 2. 48

49 49

50 50

51 51

52 52

53 53

54 54

55 55

56 56

57 57

58 58

59 59

60 60

61 61

62 62

63 63

2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 42 999544 46 48 50 52 54 56 58 60 62 64 66 68 70 72 74 76 78 80 82 84 86

65 65