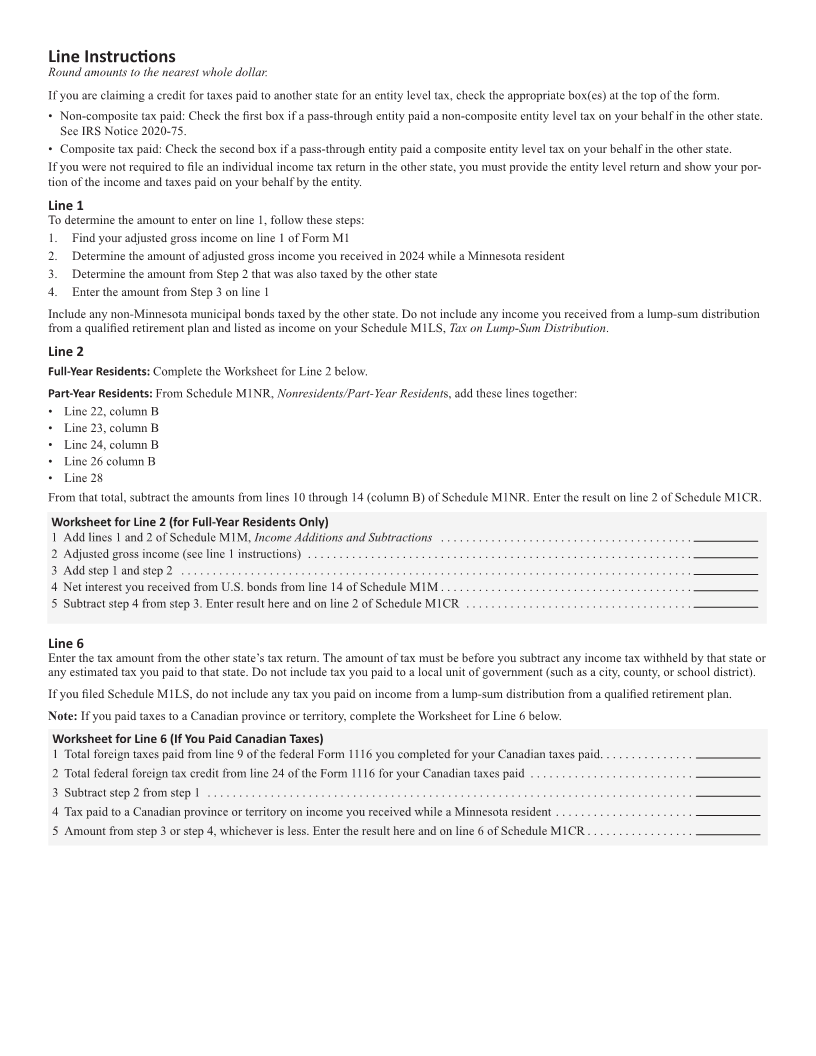

Enlarge image

NEAR FINAL DRAFT 8/1/24

*241321*

2024 Schedule M1CR, Credit for Income Tax Paid to Another State

Your First Name and Initial Last Name Social Security Number

State or Canadian Province or Territory That Taxed Income Also Taxed By Minnesota

You must complete a separate Schedule M1CR for each state or province to which you paid taxes. To report tax paid to Wisconsin, use

Schedule M1RCR, Credit for Tax Paid to Wisconsin.

To be eligible for this credit, all of these must apply:

• You were a full- or part-year Minnesota resident in 2024

• You paid 2024 state income tax to both Minnesota and another state or Canadian province on the same income

• You were a Minnesota resident when both states taxed the same income

Check this box if you are claiming a credit for non-composite tax paid by a pass-through entity (see instructions).

Check this box if you are claiming a credit for composite tax paid by a pass-through entity (see instructions) .

Round amounts to the

Full-Year Residents and Part-Year Residents nearest whole dollar.

1 Amount of adjusted gross income you received while

a Minnesota resident that was taxed by the other state (see instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2 Your adjusted gross income adjusted by U .S . bond interest and

bonds of another state (determine from instructions).

Part-year residents: See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

3 Divide line 1 by line 2 . Enter the result as a decimal (carry to

five decimal places; if line 1 is more than line 2, enter 1.00000) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 .

4 Complete the lines below to determine your Minnesota tax after credits.

a Tax from line 13 of Form M1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4a

b Add lines 1-2 and 4-9 of Schedule M1C . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4b

Subtract line 4b from line 4a . If the result is zero or less, STOP HERE . You do not qualify for this credit . . . . . . . . . . 4

5 Multiply line 4 by line 3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

6 From the other state’s income tax return, enter the tax amount before

you subtract any tax withheld or estimated tax payments (see instructions).

If you paid taxes to a Canadian province or territory, see instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Full-Year Residents

7 Amount from line 5 or line 6, whichever is less . Enter here and include on line 3 of Schedule M1C . . . . . . . . . . . . . 7

Part-Year Residents

8 From the other state’s income tax return, enter the amount of income

taxed by that state before subtracting itemized or standard deductions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

9 Divide line 1 by line 8 . Enter the result as a decimal (carry to

five decimal places; if line 1 is more than line 8, enter 1.00000) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9 .

10 Multiply line 6 by line 9 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

11 Amount from line 5 or line 10, whichever is less . Enter here and include on line 3 of Schedule M1C . . . . . . . . . . . 11

You must include this schedule with your Form M1.

9995