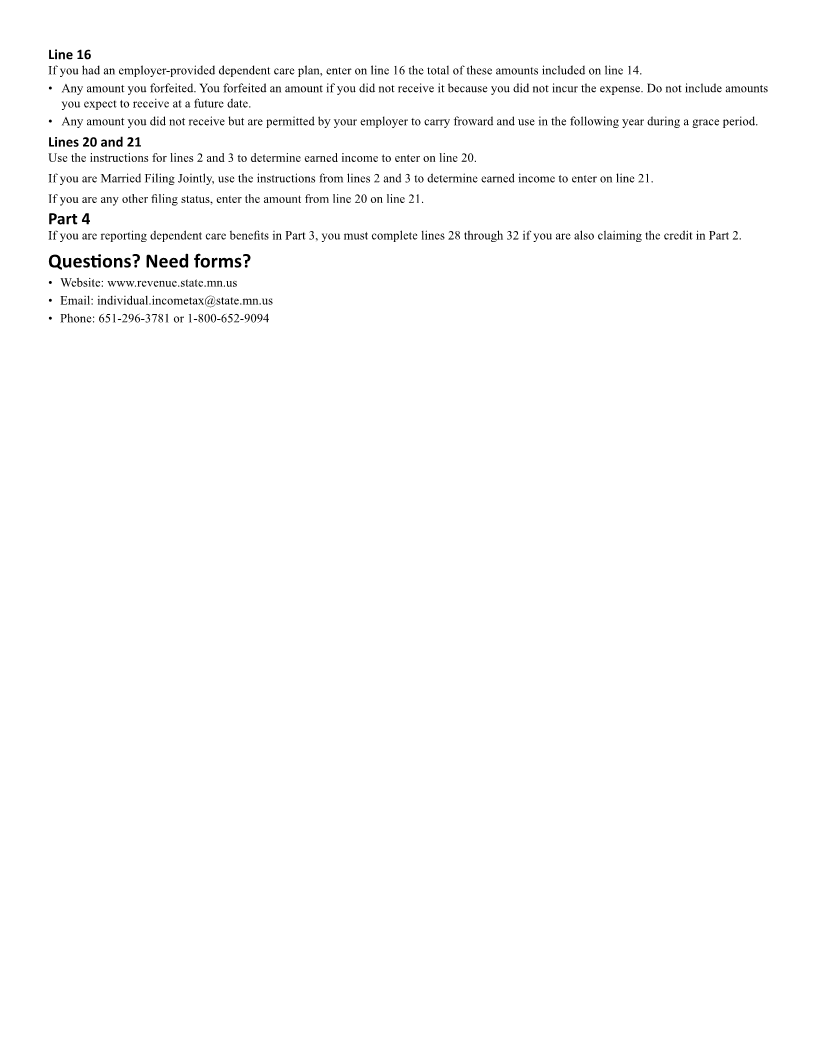

Enlarge image

NEAR FINAL DRAFT 8/1/24

*241771*

2024 Schedule M1CD, Child and Dependent Care Credit

If you received dependent care benefits, you must complete Parts 1 through 4. If you did not receive dependent care benefits, complete only Parts 1

and 2. You cannot claim child and dependent care expenses if your filing status is Married Filing Separately, unless you meet the requirements listed in

the instructions under “Married Persons Filing Separately.”

Your First Name and Initial Your Last Name Your Social Security Number

Place an X in this box if you meet the requirements to claim the credit under “Married Persons Filing Separately” in the instructions.

Place an X in this box if you operate a licensed family day care home and are claiming the credit for your own child(ren).

Enter your day care license number:

Place an X in this box if you are claiming the credit for your child born in 2024.

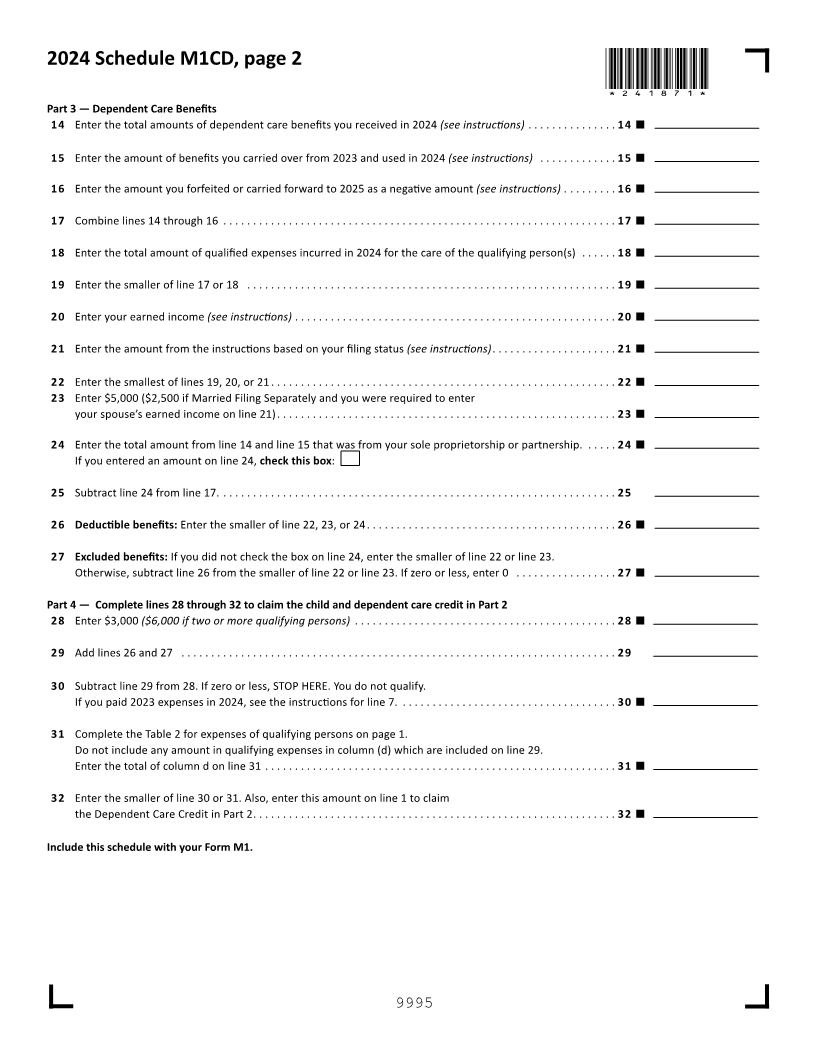

Part 1 — Table 1. Persons or organizations providing the care (if more than two care providers, see instructions)

(a) Care Provider Name (b) Address (c) ID Number (SSN or FEIN) (d) Amount Paid

Part 2 — Table 2. Credit for dependent care expenses: Information about qualifying persons

(If more than two qualifying persons, see instructions)

(a) Qualifying Person Name (b) Date of Birth (MM/DD/YYYY) (c) ID Number (SSN) (d) Qualifying Expenses

Round amounts to the nearest whole dollar.

1 Add the amounts in column (d) of Table 2. Do not enter more than $3,000 for one qualifying person

or $6,000 for two or more qualifying persons. If you completed Part 4, enter the amount from line 32. . . . . . . . . . . . . 1

2 Enter your earned income (see instructions) .. ..... ...... ..... ...... ...... ..... ...... ..... ...... ....... . 2

3 If Married Filing Jointly, enter your spouse’s earned income.

If your spouse was a student or was disabled, see instructions. All others, enter the amount from line 2 . ...... .... 3

4 Enter the smallest of 1, 2, or 3... ...... ..... ....... ..... ...... ..... ..... ...... ...... ...... ..... ...... .. 4

5 Adjusted gross income (see instructions) .... ...... ...... ..... ..... ...... ...... ..... ....... ..... ..... ... 5

6 Enter the decimal amount shown in Table 3 of the instructions that applies to the amount from line 5. ... ...... ... 6

7 Multiply line 6 by line 4. If you paid 2023 expenses in 2024, see the instructions .. ....... ...... ..... ...... ..... 7

8 If line 5 is $62,410 or less, skip line 8 and enter the amount from line 7 on line 9. If line 5 is greater than $62,410,

enter the amount from step 6 of the Worksheet for Line 8 .... ......... ...... ....... ........ ......... .. 8

9 Enter the amount from line 7 or line 8, whichever is less

Full-year residents: Enter the result here and on line 1 of Schedule M1REF.

Enter the number of qualifying persons on line 1a of Schedule M1REF .. ....... ........ ....... ........ .... 9

Part-Year Residents, Nonresidents, and American Indians Living on a Reservation

10 If you are married, add lines 2 and 3. If you are single, enter the amount from line 2 ... ...... ..... ....... .... 10

11 Amount of income on line 10 taxable to Minnesota ... ...... ..... ....... ..... ...... ..... ..... ...... ..... 11

12 Divide line 11 by 10. line Enter the result as a decimal (carry to five decimal places) ..... ...... ...... ..... ....12

13 Multiply line 9 by line 12. Enter the result here and on line 1 of Schedule M1REF.

Enter the number of qualifying persons on line 1a of Schedule M1REF..... ........ ....... ....... ........ ... 13

Continued

9995