Enlarge image

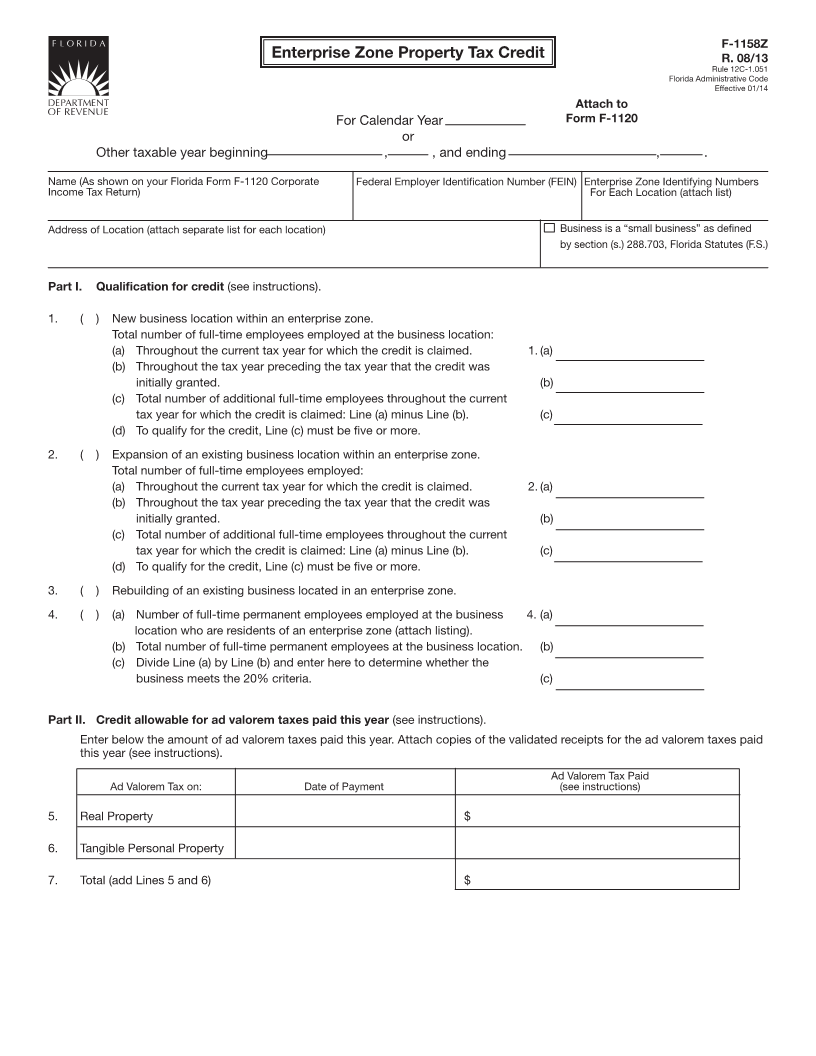

F-1158Z

Enterprise Zone Property Tax Credit R. 08/13

Rule 12C-1.051

Florida Administrative Code

Effective 01/14

Attach to

For Calendar Year Form F-1120

or

Other taxable year beginning , , and ending , .

Name (As shown on your Florida Form F-1120 Corporate Federal Employer Identification Number (FEIN) Enterprise Zone Identifying Numbers

Income Tax Return) For Each Location (attach list)

Address of Location (attach separate list for each location) Business is a “small business” as defined

by section (s.) 288.703, Florida Statutes (F.S.)

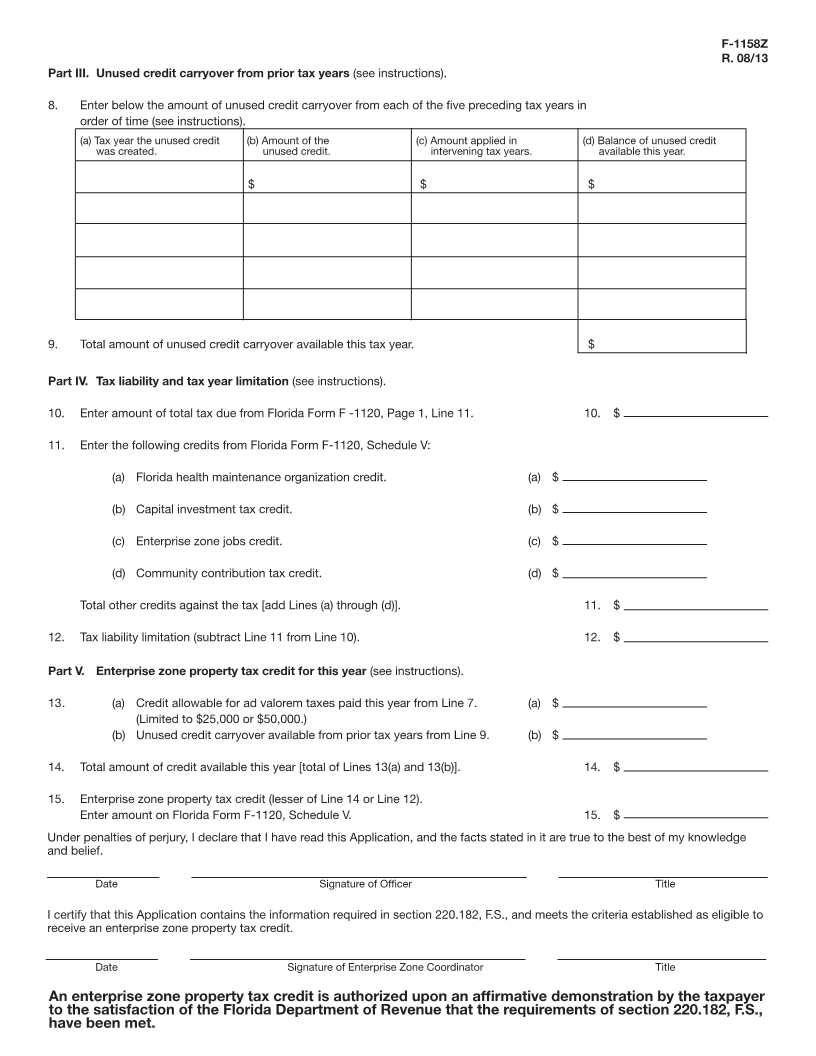

Part I. Qualification for credit (see instructions).

1. ( ) New business location within an enterprise zone.

Total number of full-time employees employed at the business location:

(a) Throughout the current tax year for which the credit is claimed. 1. (a)

(b) Throughout the tax year preceding the tax year that the credit was

initially granted. (b)

(c) Total number of additional full-time employees throughout the current

tax year for which the credit is claimed: Line (a) minus Line (b). (c)

(d) To qualify for the credit, Line (c) must be five or more.

2. ( ) Expansion of an existing business location within an enterprise zone.

Total number of full-time employees employed:

(a) Throughout the current tax year for which the credit is claimed. 2. (a)

(b) Throughout the tax year preceding the tax year that the credit was

initially granted. (b)

(c) Total number of additional full-time employees throughout the current

tax year for which the credit is claimed: Line (a) minus Line (b). (c)

(d) To qualify for the credit, Line (c) must be five or more.

3. ( ) Rebuilding of an existing business located in an enterprise zone.

4. ( ) (a) Number of full-time permanent employees employed at the business 4. (a)

location who are residents of an enterprise zone (attach listing).

(b) Total number of full-time permanent employees at the business location. (b)

(c) Divide Line (a) by Line (b) and enter here to determine whether the

business meets the 20% criteria. (c)

Part II. Credit allowable for ad valorem taxes paid this year (see instructions).

Enter below the amount of ad valorem taxes paid this year. Attach copies of the validated receipts for the ad valorem taxes paid

this year (see instructions).

Ad Valorem Tax Paid

Ad Valorem Tax on: Date of Payment (see instructions)

5. Real Property $

6. Tangible Personal Property

7. Total (add Lines 5 and 6) $