Enlarge image

No text to extract.

Enlarge image | No text to extract. |

Enlarge image |

Contents

Need assistance?

Assistance and forms .................................................................. This page You can download forms and find other

Changes for 2024 ................................................................................... 1 information on our website at:

tax.nd.gov

General instructions ................................................................................2

Email

Who must file .....................................................................................2

Individual, estate, trust, partnership,

When and where to file ........................................................................ 2 and S corporation income tax at

Extension of time to file ....................................................................... 2 individualtax@nd.gov

Penalty and interest ............................................................................ 2

Estimated tax payment (for 2025) ........................................................ 3 Call

Withholding from nonresident partners .................................................. 3 Individual income tax:

Composite filing ..................................................................................3 Questions 701-328-1247

Correcting a previously filed return ........................................................ 3 Forms 701-328-1243

Reporting federal changes .................................................................... 4 Partnership income tax:

W-2/1099 reporting requirement .......................................................... 4 Questions 701-328-1258

Disclosure notification ......................................................................... 4 Forms 701-328-1243

Use of information .............................................................................. 4 Speech/hearing impaired:

TDD 800-366-6888

General instructions for completing Form 58 .............................................. 4

Specific line instructions ..........................................................................5 Write

Form 58, Page 1, Items A-J .................................................................. 5 Office of State Tax Commissioner

Schedule FACT ................................................................................... 5 600 E. Boulevard Ave., Dept. 127

Bismarck, North Dakota 58505-0599

Schedule K ........................................................................................6

Schedule KP ..................................................................................... 10 Walk-in or appointment

Form 58, Page 1, Lines 1-12 ............................................................... 12 service

Schedule K-1 .................................................................................... 13 State Capitol Building, 8th Floor

Before you file Form 58 ..................................................................... 14 600 E. Boulevard Ave., Bismarck,

North Dakota

Required forms Monday through Friday

The following forms are needed to complete Form 58: 8:00 a.m. to 5:00 p.m.

(except holidays)

Form 58 Partnership return

Schedule FACT Calculation of North Dakota apportionment factor Walk-ins are welcome. To assure

Schedule K Total North Dakota adjustments, credits, and other availability and promptness of

items distributable to partners service, call in advance to make an

Schedule KP Partner information appointment.

Schedule K-1 Partner’s share of North Dakota income (loss), deductions,

adjustments, credits, and other items

The following forms may be needed:

Form 58-PV Partnership return payment voucher

Form 58-EXT Partnership extension payment voucher

Form 101 Application for extension of time to file a North Dakota Privacy Act Notification

In compliance with the Privacy Act of

income tax return 1974, disclosure of a Federal Employer

Form PWA Passthrough entity withholding adjustment Identification Number (FEIN) or social

Form PWE Nonresident passthrough entity member exemption and security number on this form is required under

certification N.D.C.C. §§ 57-01-15 and 57-38-42, and will

be used for tax reporting, identification, and

Download these forms from our website at tax.nd.gov. administration of North Dakota tax laws.

Disclosure is mandatory. Failure to provide

the FEIN or social security number may

delay or prevent the processing of this form.

Taxpayer Bill of Rights

Obtain a copy of the North Dakota Taxpayer Bill of Rights on the

Office of State Tax Commissioner’s website at

tax.nd.gov 28703 December 2024

|

Enlarge image |

1

Changes affecting partnerships

Developments, updates, and items of interest relating to partnership income tax

Form 1099/K-1 withholding Renaissance Zone tax incentive Disabled employment tax credit

Partnerships claiming North Dakota changes effective August 1, 2023 In 2023, the North Dakota Legislature

withholding reported on a Form 1099 reenacted and made permanent the

or ND Schedule K-1 must correctly A variety of changes occurred to the existing income tax credit related to

identify which form the withholding Renaissance Zone program. One of the employment of an individual with

was reported on in their tax software the changes is the maximum length of developmental disabilities or severe

program. These forms are not an income tax incentive was changed mental illness. The existing provisions

interchangeable when e-filing. If the from 5 years to 8 years for a project of the tax credit were unchanged,

forms are not identified correctly, this that meets certain rehabilitation except the statewide limitation on

will delay processing of your return. thresholds. Specifically, for residential the number of eligible employees was

(except owner occupied) and removed and there is no limit.

Electronic filing commercial property, a rehabilitation

Partnerships with 10 or more owners level exceeding 75% is required Stay informed

are required to file the North Dakota to allow for an exemption up to 8 Individuals, businesses, or other

income tax return and pay any tax years. Rehabilitation exceeding 50% interested persons may sign up to

due on it by electronic means. If a is required for an exemption up to 5 receive email notifications when

partnership return with 10 or more years. For owner occupied residential a newsletter or other important

owners is filed on paper, the return property, rehabilitation exceeding information is issued by the Office of

will not be processed and may be 20% may qualify for an exemption up State Tax Commissioner. To sign up,

subject to penalties due to the failure to 8 years. go to tax.nd.gov and select “News

to file electronically. Center” at the top of the page. Then

For additional RZ information, please select “Email Sign-Up”.

Tax credit for contributions to refer to our website:

a maternity home, child placing tax.nd.gov/renaissance-zone-

agency, or pregnancy help center incentives.

An income tax credit is allowed Automation tax credit

for contributions to a child placing

agency licensed by the North Dakota The 2023 North Dakota Legislature

Department of Health and Human made changes to the automation

Services (DHS), a nonprofit maternity tax credit program. The program

home located in North Dakota, or a was expanded to include automation

pregnancy help center recognized by or robotic equipment purchased

DHS. See Schedule MCP. to upgrade or advance an animal

agricultural process.

Tax credit for compensation paid

to an apprentice The tax rate was changed to 15% of

the cost of the qualifying equipment.

Beginning with tax year 2023, an The annual maximum statewide tax

income tax credit was created for the credits authorized was increased from

employment of a qualified apprentice $1 million to $3 million per year.

in an apprenticeship program position

in North Dakota. Of the $3 million annual total amount,

$500,000 of tax credits is reserved

The apprentice must be in an each year for first-time claimants for

apprenticeship program certified by automation equipment and $500,000

the U.S. Department of Labor or be of tax credits is reserved each year

an electrical apprentice registered for first-time claimants for animal

under North Dakota law. agriculture equipment.

The credit is equal to 10% of the The program was also made

stipend or salary paid to the qualified permanent. Other provisions were

apprentice. The maximum credit a unchanged.

taxpayer can claim in all tax years is

$3,000 and limits the earning of a tax The requirement continues to exist for

credit to only five apprentices at the a claimant to subsequently file with

same time. the Office of State Tax Commissioner

a report of Improved Job Quality or

Increased Productivity.

|

Enlarge image |

2

Form 58 Instructions 2024

North Dakota Partnership Income Tax Return

“N.D.C.C.” references are to the North Dakota Century Code, which contains North Dakota’s statutes.

“N.D. Admin. Code” references are to the North Dakota Administrative Code, which contains North Dakota’s rules.

Electronic filing North Dakota extension may be

General applied for by filing Form 101,

Partnerships with 10 or more owners

instructions are required to file the North Dakota Application for Extension of Time to

income tax return and pay any tax File a North Dakota Tax Return. This

Who must file due on it by electronic means. is not an automatic extension—there

A 2024 Form 58, Partnership Income must be good cause to request a

Tax Return, must be filed by a When and where to file North Dakota extension. Form 101

partnership that meets both of the The 2024 Form 58 must be filed on must be postmarked on or before the

following: or before (1) April 15, 2025, if filing due date of Form 58. Notification of

• It is required to file a 2024 for the 2024 calendar year, or (2) the whether the extension is accepted or

Form 1065, U.S. Return of 15th day of the fourth month following rejected will be provided by the

Partnership Income. the end of the tax year, if filing for Office of State Tax Commissioner.

a fiscal year beginning in the 2024

• It carries on business, or derives Extension interest. If Form 58 is

calendar year. If the due date falls

gross income from sources, in filed on or before the extended due

on a Saturday, Sunday, or holiday,

North Dakota during the 2024 tax date, and the total amount of tax due

the return may be filed on or before

year. is paid with the return, no penalty will

the next day that is not a Saturday, be charged. Interest on the tax due will

Investment partnership. A Sunday, or holiday. be charged at the rate of 12% per year

partnership that elects out of the from the original due date of the return

Note: Use the 2023 Form 58 if filing

partnership rules under I.R.C. to the earlier of the date the return is

for a fiscal year beginning in the 2023

§ 761(a)(1) and does not file a federal filed or the extended due date.

calendar year.

partnership return must file a 2024

Form 58 if it carries on investment If not required to file Prepayment of tax due. If an

activity, or derives any gross income electronically, mail Form 58 and all extension of time to file Form 58 is

from sources, in North Dakota during required attachments to: obtained, any tax expected to be due

may be paid on or before the regular

its 2024 tax year. A 2024 Form 1065 Office of State Tax Commissioner due date to avoid paying extension

must be completed on a pro forma 600 East Boulevard Ave., Dept. 127 interest. For more information,

basis and attached to Form 58. Bismarck, ND 58505-0599 including payment options, obtain the

Limited liability company (LLC). An 2024 Form 58-EXT.

LLC that is classified as a partnership Extension of time to file

for federal income tax purposes is An extension of time to file Form 58 Alternatively, a check or money

treated like a partnership for may be obtained in one of the order may be sent with a letter

North Dakota income tax purposes following ways: containing the following: (1) name of

and must file Form 58 if it meets the partnership, (2) partnership’s FEIN,

above conditions for filing. • Obtain a federal extension. (3) partnership’s address and phone

• Separately apply for a number, and (4) statement that the

Nonfiler penalty. If a partnership North Dakota extension. payment is a 2024 Form 58-EXT

does not file Form 58 as required, payment.

a minimum $500 penalty may be Federal extension. If an extension

assessed if the failure continues after of time to file the federal partnership Penalty and interest

receiving a 30-day notice to file from return is obtained, it is automatically If an extension of time to file

the Office of State Tax Commissioner. accepted as an extension of time to Form 58 was obtained, the tax

file Form 58. If this applies, a separate due may be paid by the extended

Disaster recovery tax exemptions. North Dakota extension does not have due date of the return without

Exemptions from state and local tax to be applied for, nor does the penalty, but extension interest will

filing and payment obligations are Office of State Tax Commissioner have apply—see “Extension interest” and

available to out-of-state businesses to be notified that a federal extension “Prepayment of tax due” on this page.

and their employees who are in has been obtained prior to filing

North Dakota on a temporary basis Form 58. The extended due date for If Form 58 is filed by its due date (or

for the sole purpose of repairing North Dakota purposes is the same as extended due date), but the total

or replacing natural gas, electrical, the federal extended due date. amount of tax due is not paid by the

or telecommunication transmission due date (or extended due date), a

property that is damaged, or under North Dakota extension. If a penalty equal to 5% of the unpaid tax

threat of damage, from a state- or federal extension is not obtained, or $5.00, whichever is greater, must

presidentially-declared disaster or but additional time is needed to be paid.

emergency. For more information, go complete and file Form 58, a separate

to tax.nd.gov.

|

Enlarge image |

3

If Form 58 is filed after its due date • The nonresident partner elects to filing satisfies the North Dakota

(or extended due date), and there include the distributive share in a income tax filing and payment

is an unpaid tax due on it, a penalty composite filing—see “Composite obligations of the eligible nonresident

equal to 5% of the unpaid tax due or filing” on this page. partners included in it, which means

$5.00, whichever is greater, for the • The nonresident partner is a they do not have to separately file

month the return was due plus 5% of passthrough entity and elects their own North Dakota income tax

the unpaid tax due for each additional exemption from withholding on its returns. The composite filing method

month (or fraction of a month) during distributive share of North Dakota is optional and does not require prior

which the return remains delinquent income. For more information, approval from the Office of State Tax

must be paid. This penalty may not obtain Form PWE. Commissioner, and a choice to use it

exceed 25% of the tax due. may be made on a year-to-year basis.

Withholding procedure. This

In addition to any penalty, interest withholding requirement applies to Eligible nonresident partner. For

must be paid at the rate of 1% per a nonresident partner’s year-end purposes of this composite filing

month or fraction of a month, except distributive share of North Dakota method, a nonresident partner

for the month in which the tax was income, which is determined at the has the same meaning as that

due, on any tax due that remains end of the partnership’s tax year and used for withholding income tax

unpaid after the return’s due date (or reported on Form 58, Schedule KP, from nonresident partners—see

extended due date). Column 6. The requirement does “Withholding from nonresident

not apply to actual distributions partners” on this page. A nonresident

Estimated tax payment partner is eligible to be included in a

made to a nonresident partner

(for 2025) during the tax year. The withholding composite filing if both of the following

A partnership may, but is not required amount is calculated and reported apply:

to, make estimated income tax on Schedule KP, Column 7. If a • The nonresident partner’s

payments. For more information, nonresident partner meets certain only source of income within

including payment options, obtain the conditions, an amount less than the North Dakota is one or more

2025 Form 58-ES. amount calculated at the 2.50% passthrough entities. A

Withholding from tax rate may be withheld. For the passthrough entity includes a trust,

qualifying conditions, see Form PWA. partnership, S corporation, LLC

nonresident partners A partnership must submit a payment treated like a partnership or

A partnership must withhold for the total amount of withholding S corporation, and any other

North Dakota income tax at the rate of reported on Schedule KP, Column 7, similar entity.

2.50% from the year-end distributive with Form 58 when it is filed.

share of North Dakota income of a • The nonresident partner elects

nonresident partner. See “Publicly Publicly traded partnership. to be included in a composite

traded partnership” on this page for A publicly traded partnership, as filing. An election is indicated by

an exception to this requirement. defined under Internal Revenue Code the partnership’s calculation and

§ 7704(b), does not have to withhold reporting of a tax amount for the

Nonresident partner. For purposes North Dakota income tax from its nonresident partner on Form 58,

of this withholding requirement, a unitholders if it meets both of the Schedule KP, Column 8. (If the

nonresident partner means: following: distributive share is a loss, the tax

is zero.)

• an individual who is not domiciled • It is treated as a partnership for

in North Dakota; federal income tax purposes. The distributive share of North Dakota

• a trust, including a grantor trust, • It reports on Form 58, income included in a composite return

that is not organized under Schedule KP, every unitholder with is subject to tax even if it is under

North Dakota law. This only a North Dakota distributive share $1,000.

includes trusts that are subject to of income of over $500. Composite filing method

income tax; or

procedure. The tax under the

• a passthrough entity that has a Composite filing composite filing method is calculated

commercial domicile outside North A composite filing method is available and reported on Form 58, Schedule KP,

Dakota. A passthrough entity to a partnership with one or more Column 8. A partnership must submit

includes a partnership, eligible nonresident partners. Under a payment for the total tax reported on

S corporation, LLC treated like a this method, a partnership calculates Schedule KP, Column 8, with Form 58

partnership or S corporation, and the North Dakota income tax on an when it is filed.

any other similar entity. eligible nonresident partner’s year-end

Exemption from withholding. No distributive share of North Dakota Correcting a previously filed

withholding is required if any of the income and pays the tax with return

following apply: Form 58. The tax is calculated at If a partnership needs to correct an

the highest individual income tax error on Form 58 after it is filed, the

• The distributive share of rate (which is 2.50% for the 2024 partnership must file an amended

North Dakota income is less tax year), and no adjustments, return. There is no special form for

than $1,000. deductions, or tax credits are allowed this purpose. See “How to prepare an

in calculating the tax. A composite amended 2024 return” below.

|

Enlarge image |

4

If a partnership paid too much tax return, an amended North Dakota 5. Complete Schedule KP on

because of an error on its 2024 Form 58 must be filed within 90 days page 5 of Form 58—see page 10.

Form 58, the partnership generally after the final determination of the 6. Complete lines 1 through 12 on

has three years from the due date of IRS changes or the filing of the page 1 of Form 58—see page 12.

the return (excluding extensions) or amended federal return. Enclose a

the date the return was actually filed, copy of the IRS audit report or the 7. Complete Schedule K-1, if

whichever is later, in which to file an amended federal partnership return required, for the partners—see

amended return to claim a refund of with the amended North Dakota page 13.

the overpayment. See N.D.C.C. Form 58. Rounding of numbers. Numbers

§ 57-38-40 for other time periods that may be entered on the return in

may apply. W-2/1099 reporting dollars and cents, or they may be

requirement rounded to the nearest whole dollar. If

How to prepare an amended 2024 Every partnership doing business in rounding, drop the cents if less than

return North Dakota that is required to file $0.50 and round up to the next whole

1. Obtain a blank 2024 Form 58. Federal Form 1099 or W-2 must also dollar amount if $0.50 or higher. For

2. Enter the partnership’s name, file one with the Office of State Tax example, $25.36 becomes $25.00,

current address, FEIN, etc., in the Commissioner. For more information, and $25.50 becomes $26.00.

top portion of page 1 of Form 58. obtain the guideline Income Tax

Withholding and see “Annual Filing Fiscal year filers. The tax year for

3. Fill in the “Amended return” circle Requirements - W-2 and 1099.” North Dakota income tax purposes

at the top of page 1 of Form 58. must be the same as the tax year

4. Complete Schedules FACT, Disclosure notification used for federal income tax purposes.

K, and KP using the corrected Upon written request from the Use the 2023 Form 58 if the

information. However, unless chairman of a North Dakota legislative partnership’s taxable year began in

there is an increase in the standing committee or Legislative the 2023 calendar year.

amount reported on Schedule KP, Management, the law requires the

Column 6, of the amended return, Office of State Tax Commissioner to Specific line

enter on Schedule KP, Column 7, disclose the amount of any deduction

the same amount reported on or credit claimed on a tax return. instructions for

the previously filed return. Then Any other confidential information,

complete lines 1 through 3 on such as a taxpayer’s name or federal page 1 of

page 1 of Form 58. employer identification number, may

not be disclosed. Form 58, Items A-J

5. On line 5 of one of Form 58,

Complete Items A through J at

enter the total taxes due from the Use of information the top of page 1 of Form 58.

previously filed 2024 Form 58, All of the information on Form 58 and Then complete Schedule FACT,

page 1, line 3. its attachments is confidential by law Schedule K, and Schedule KP

6. Complete line 7 (overpayment) and cannot be given to others except before completing lines 1

or line 10 (tax due), whichever as provided by state law. Information through 12 on page 1 of Form 58.

applies. If there is an about the partners is required under

overpayment on line 7, enter the state law so the Office of State Item A - Tax year

full amount on line 9 (refund). On Tax Commissioner can determine The same tax year used for federal

an amended return, the amount the partner’s correct North Dakota income tax purposes (as indicated on

credited to the next year’s taxable income and verify if the the federal partnership return) must

estimated tax (line 8) may not be partner has filed a return and paid the be used for North Dakota income

increased or decreased. tax. tax purposes. Fill in the applicable

circle. If the partnership uses a fiscal

7. Attach a statement explaining the

year, enter the beginning and ending

reason(s) for filing the amended General instructions dates of the fiscal year. Use the 2024

return. If it is because of changes

the partnership or the IRS made for completing Form 58 only if the partnership’s tax

year began in the 2024 calendar year.

to the partnership’s 2024 Federal

Form 1065, attach a copy of the Form 58 Item B - Name and address

amended federal return or IRS Complete Federal Enter the legal name of the partnership

notice. on the first line of the name and

Form 1065 as follows:

8. Complete and provide a corrected address area. If the partnership

Schedule K-1 (Form 58) to the 1. Complete Federal Form 1065 (or publicly operates under a fictitious or

partners, as required. 1065-B) in its entirety. assumed name (which, in most states,

2. Complete Items A through J at must be recorded or registered with

Reporting federal changes the top of page 1 of the state), enter that name on the

If the Internal Revenue Service Form 58—see page 4. second line of the name and address

(IRS) changes or audits the federal area. If filing an amended return, enter

3. Complete Schedule FACT on

partnership return, or if a partnership the most current address.

page 2 of Form 58—see page 5.

files an amended federal partnership

4. Complete Schedule K on page 3

of Form 58—see page 6.

|

Enlarge image |

5

Item C - Federal EIN Item H - Professional service • Multistate partnership

North Dakota uses the federal partnership If the partnership conducted its

employer identification number Indicate whether the partnership is trade or business both within

(FEIN) for identification purposes. a professional service partnership. and without North Dakota during

Enter the FEIN from page 1 of Federal A “professional service partnership” the tax year, complete lines

Form 1065. is a partnership that engages in the 1 through 14. However, if all

practice of law, accounting, medicine, of the partners consist of only

Item D - Business code number or any other profession in which the North Dakota resident individuals,

Enter the business code number from capital or the services of employees estates, and trusts, skip lines 1

the NAICS code list found on the are not a material income-producing through 13 and enter “1.000000”

Office of State Tax Commissioner’s factor. The services performed by on line 14.

website at tax.nd.gov. Enter the the partners themselves must be the

code that most closely describes the primary income-producing factor. A If the partnership has a partner

industry in which the partnership professional service partnership does OTHER THAN an individual, estate,

derives most of its income. not include one that primarily engages or trust, complete lines 1 through 14

Item E - Date business started in wholesale or retail sales activity, of Schedule FACT.

Enter the date the business started manufacturing activity, or any other Apportionment factor in

from page 1 of Federal Form 1065. type of activity in which the capital

general

or the services of employees are a

In general, the apportionment factor

Item F - Indicators material income-producing factor.

Fill in applicable circles, as follows: is a product of a formula consisting of

Item I - Publicly traded an equally-weighted average of three

Initial return. Fill in circle if this is partnership factors: property, payroll, and sales.

the first return filed in North Dakota Indicate whether the partnership is a Each factor represents the percentage

by the partnership. publicly traded partnership. A “publicly of the partnership’s North Dakota

Final return. Fill in circle if this is the traded partnership” is a partnership in activity compared to its total

last return to be filed in North Dakota which interests in it are either traded activity everywhere. A partnership

by this partnership. on an established securities market multiplies its business income by the

or are readily tradable on a secondary apportionment factor to determine

Farming/ranching partnership. market. the portion of its business income

Fill in circle if this is an LLC that is attributable to North Dakota.

registered as a farming and ranching Item J

LLC with the North Dakota Secretary Tiered partnership If the partnership includes the

of State. Indicate whether the partnership distributable share of income

holds an interest in one or more from another partnership in its

Filed by an LLC. Fill in circle if the other partnerships or limited liability apportionable business income, include

entity filing this return is an LLC. companies. If it does, attach a in the numerator and denominator

Composite return. Fill in this circle statement to Form 58 showing of each factor the partnership’s

only if (1) the partnership has one or the name and federal employer proportionate share of the other

more nonresident partners eligible to identification number of each partnership’s apportionment factors—

be included in a composite filing and partnership or LLC in which it holds an see the specific line instructions for

(2) all of them elected to include their interest. more information. Do not include in

distributive shares of North Dakota the factors any property, payroll, or

source income in a composite filing. Instructions for sales related to allocable nonbusiness

See “Composite filing” on page 3 for income—see the instructions to

more information. Schedule FACT Form 58, Schedule K, line 24, for what

constitutes allocable nonbusiness

Amended return. Fill in circle if (Form 58, page 2) income.

this return is being filed to correct a General instructions If the amount of any factor’s

previously filed 2024 Form 58. See All partnerships must complete the denominator is zero, exclude that

“Correcting a previously filed return” applicable portions of Schedule FACT. factor from the calculation.

on page 3 for more information.

If the partnership has ONLY individual, Special apportionment rules

Extension. Fill in circle if a federal estate, and trust partners, complete may apply in the case of certain

or state extension of time to file the Schedule FACT as follows: industries or unique circumstances.

return was obtained. See “Extension

of time to file” on page 2 for more • 100% North Dakota For additional information on the

information. partnership apportionment factor, see N.D.C.C.

If the partnership conducted all of Ch. 57-38.1 and N.D. Admin. Code

Item G - Number of partners its business within North Dakota Ch. 81-03-09.

Enter the total number of partners during the tax year, skip lines 1

and the number of each type of through 13 and enter “1.000000”

partner. on line 14.

|

Enlarge image |

6

Specific line instructions one state, compensation is generally a tax measured by income in that

assigned to North Dakota based on jurisdiction. For more complete

Property factor the amount of compensation reported information, see N.D. Admin. Code

Lines 1 through 6 to North Dakota for unemployment §§ 81-03-09-29 and 81-03-09-30.

Owned and rented property compensation purposes. Whether

Line 14

Enter on the applicable line the or not state income tax was

Apportionment factor

average value of real and tangible withheld from an employee’s

Divide line 13 by the number of

personal property owned and rented compensation does not affect where

factors having an amount greater than

by the partnership. For owned the compensation is assigned for

zero in column 1 on lines 7, 8, and 12.

property, this generally means the apportionment factor purposes.

Enter the result on this line.

average of the original cost (before Include on this line in the applicable

depreciation) used for federal income column the partnership’s share of the

tax purposes. For rented property, payroll factor from a North Dakota

Instructions for

this generally means the amount of Schedule K-1 (Form 58), Part 6. For

rent paid multiplied by eight. Certain more complete information on Schedule K

property items are subject to special the payroll factor, see N.D. Admin.

rules. Do not include amounts related Code §§ 81-03-09-22 through (Form 58, page 3)

to construction in progress. Include on 81-03-09-25. All partnerships must complete

Schedule K. The purpose of this

line 5 the partnership’s share of the Sales Factor schedule is to show the total amount

property factor from a North Dakota

Schedule K-1 (Form 58), Part 6. Line 9 of North Dakota adjustments, credits,

Everywhere sales and other items distributable to

The average value of owned and Enter the partnership’s total its partners. These items may be

rented property is assigned to North sales or receipts, less returns or applicable to the preparation of the

Dakota if the property is located allowances, for the tax year. Sales partners’ North Dakota income tax

in North Dakota. The amount generally means all gross receipts returns.

attributable to mobile property is of a partnership. However, the types Schedule K-1 from another

generally assignable to North Dakota of sales or gross receipts included passthrough entity.

based on a ratio of the property’s in the sales factor depend on the Include on the applicable lines

time spent in North Dakota. For more nature of the partnership’s regular of Schedule K any adjustments,

complete information on the property business activities and may include credits, etc., from a North Dakota

factor, see N.D. Admin. Code amounts other than sales reported Schedule K-1, as instructed in the

§§ 81-03-09-15 through 81-03-09-21 on Form 1065, line 1. Include on this partner or beneficiary instructions to

and 81-03-09-33. line the partnership’s share of the that form.

Payroll factor everywhere sales from a North Dakota

Schedule K-1 (Form 58), Part 6. Reminder: Be sure to attach to

Line 8 Form 58 any prescribed schedule or

Enter the amount of total Line 10 other supporting document specified

compensation paid to employees North Dakota sales in the instructions.

for the tax year. This includes gross For sales of tangible property, the

wages, salaries, commissions, and sale is assigned to North Dakota if the Property tax clearance

any other form of remuneration paid destination of the property is in North Dakota Century Code

to the employees. Use the amount North Dakota, regardless of the § 57-01-15.1 provides that, before

before deductions for deferred shipping terms. For sales of other certain state tax incentives may be

compensation, flexible spending plans, than tangible property, the sale claimed, a taxpayer must obtain a

and other payroll deductions. Do not is assigned to North Dakota if the property tax clearance record from

include amounts paid for employee income-producing activity which gave each North Dakota county in which

benefit plans that are not considered rise to the receipt is performed in the taxpayer holds a 50% or more

taxable wages to the employee. An North Dakota. Include on this line ownership interest in real property.

employee is an individual treated as the partnership’s share of the North The property tax clearance record(s)

an employee under the usual common Dakota sales from a North Dakota must be attached to the North Dakota

law rules, which generally mirror an Schedule K-1 (Form 58), Part 6. For tax return on which the incentive is

individual’s status for purposes of more complete information, see N.D. claimed. Certain tax incentives on

unemployment compensation and the Admin. Code §§ 81-03-09-26 through Form 58, Schedule K, are subject

Federal Insurance Contribution Act. 81-03-09-31 and 81-03-09-34. to this requirement. The incentives

Do not include on this line guaranteed subject to this requirement are

payments to partners. Line 11 identified in the box at the top of

Throwback sales Schedule K.

Compensation of an employee’s Enter the amount of sales shipped

services performed entirely within from a location in North Dakota that If the partnership is claiming any

North Dakota is assigned to are delivered to the U.S. government of the specified incentives, it must

North Dakota. For an employee whose or to another state or country complete the property tax clearance

services are performed in more than where the sales are not subject to section at the top of Schedule K. If

the partnership is required to attach

|

Enlarge image |

7

a property tax clearance record, Line 5 Line 9

obtain one by completing the form New or expanding business Ag commodity investment tax

Property Tax Clearance Record, which income exemption credit

is available on the Office of State Tax If the partnership qualified for the If the partnership invested in a

Commissioner’s website. new or expanding business income qualified business for purposes of the

exemption under N.D.C.C. agricultural commodity processing

Line 1 Ch. 40-57.1, enter the exempt facility investment tax credit, multiply

Income from state, local, and portion of the partnership’s business the total amount invested during the

foreign securities and bonds income. See N.D. Admin. Code 2024 tax year by 30% and enter the

Enter on this line interest and 81-03-01.1-06§ for guidance on result on this line. The partnership

dividend income from state, local, calculating the amount of the exempt is allowed no more than $250,000

and foreign securities and bonds that income. Attach a statement in total credits for investments

is exempt from federal income tax. showing the calculation of the made in tax years 2005 and after.

Do not include interest income from exempt income. See N.D.C.C. Ch. 57-38.6. Attach

securities or bonds issued by a copy of the Ag Commodity

North Dakota or its political Line 6 Processing Facility Investment

subdivisions. Do not enter on this Eminent domain gain Reporting Form. Or, if claiming an

line any income that is treated Enter on this line the taxable portion agricultural commodity processing

as nonbusiness income subject of a gain from the disposition of facility investment credit from a

to allocation under N.D.C.C. property due to the exercise of North Dakota Schedule K-1, attach

§§ 57-38.1-04 through 57-38.1-08. eminent domain. a statement identifying the facility

Include the nonbusiness income on in which the investment was

Line 7a

Schedule K, line 24. made.

Renaissance zone historic

Line 2 property preservation tax credit Line 10

State and local income taxes Enter on this line the amount from Biodiesel or green diesel fuel

Enter on this line the taxes measured Schedule RZ, Part 7, line 4. Attach blending tax credit

by income that were incurred by Schedule RZ. If the partnership is a licensed

the partnership and deducted in supplier of biodiesel or green diesel

Line 7b

calculating the partnership’s ordinary fuel, it is allowed a credit equal to

Renaissance fund organization

income (loss). Include franchise or $0.05 per gallon for blending biodiesel

investment tax credit

privilege taxes measured by income or green diesel fuel having at least

Enter on this line the amount from

paid to any taxing authority, including a 5% blend (“B5”) that meets ASTM

Schedule RZ, Part 7, line 5. Attach

a foreign country. specifications. The blending must

Schedule RZ.

be done in North Dakota. For this

Line 3 Line 7c purpose, a “supplier” means a person

Interest from U.S. obligations Renaissance zone nonparticipating who distributes the biodiesel or green

Enter on this line interest income from property owner tax credit diesel fuel from a terminal in

U.S. obligations and from securities Enter on this line the amount from North Dakota. Enter the credit on this

the interest from which is specifically Schedule RZ, Part 7, line 6. Attach line. See N.D.C.C. § 57-38-01.22.

exempted from state income tax by Schedule RZ. Attach a statement showing the

federal statute. Include the portion of

dividend income from a mutual fund Line 8 calculation of the credit.

attributable to the fund’s investment Seed capital investment tax credit Line 11

in the same kinds of securities. If the partnership invested in a Biodiesel or green diesel fuel sales

qualified business for purposes of the

Do not enter on this line interest equipment tax credit

seed capital investment tax credit,

income from securities of the Federal If the partnership is a licensed seller

multiply the total amount invested

Home Loan Mortgage Corporation of biodiesel or green diesel fuel, it is

during the 2024 tax year by 45%

(Freddie Mac), Federal National allowed a credit equal to 10% of the

and enter the result on this line.

Mortgage Association (Fannie Mae), costs to adapt or add equipment to

See N.D.C.C. Ch. 57-38.5. Attach a

Government National Mortgage its North Dakota facility to enable it

copy of the Qualified Seed Capital

Association (Ginnie Mae), or from to sell diesel fuel having at least a

Business Investment Reporting

a federal income tax refund or 2% biodiesel or green diesel blend

Form. Or, if claiming a seed capital

repurchase agreement. Attach a (“B2”) that meets ASTM specifications.

investment credit from a

statement identifying the specific For this purpose, a “seller” means a

North Dakota Schedule K-1,

securities from which the interest person who acquires the fuel from

attach a statement identifying the

was derived. a wholesale supplier or distributor

qualified business in which the for resale to a consumer at a retail

Line 4 investment was made. location. Except for costs incurred

Renaissance zone exemption before January 1, 2005, include

Enter on this line the amount from eligible costs incurred before the tax

Schedule RZ, Part 7, line 1c. Attach year in which sales of the eligible

Schedule RZ. biodiesel or green diesel fuel begin.

|

Enlarge image |

8

The credit is allowed in each of five Lines 14c and 14d. Enter on category of school, the credit equals

tax years, starting with the tax year these lines an endowment fund 50% of the contributions made to all

in which sales of the eligible biodiesel credit and the related contribution eligible schools within the category.

or green diesel fuel begin. Enter amount shown on a North Dakota (Note: For a partner other than

the credit on this line. See N.D.C.C. Schedule K-1 received from an estate, another passthrough entity, additional

§ 57-38-01.23. Attach a statement trust, partnership, or S corporation. limitations on the allowable credit

showing the calculation of the apply at the partner level.) A list of

Line 15

credit. the eligible schools within each of

Workforce recruitment tax credit the three categories of schools is

Line 12 If the partnership employs provided on page 15.

Employer internship program tax extraordinary recruitment methods

credit to hire an employee to fill a hard- Election. A partnership may elect, on

If the partnership hired an eligible to-fill position in North Dakota, it is a contribution by contribution basis,

college student under a qualifying allowed a tax credit equal to 5% of to treat a contribution as having been

internship program set up in the compensation paid during the made during the 2024 tax year if it

North Dakota, it is allowed a credit first 12 months to the employee is made on or before the due date,

equal to 10% of the compensation hired to fill that position. The credit including extensions, for filing the

paid to the intern. For details, may be claimed in the first taxable 2024 Form 58. Make the election by

see N.D.C.C. § 57-38-01.24. The year beginning after the employee attaching to the return a document

partnership is allowed no more than completes the first 12 consecutive containing the following:

$3,000 of credits for all tax years. months of employment. For details,

1. A statement that the election is

see N.D.C.C. § 57-38-01.25.

Line 12a. Enter the allowable credit being made.

on this line. Line 15a. Enter the allowable credit 2. Name of qualifying school.

on this line.

Attach a schedule listing the names 3. Date of contribution.

of the employees, their social security Attach a schedule listing the names 4. Amount of contribution.

numbers, and wages paid. If the credit of the employees, their social

is received through a passthrough security numbers, wages paid, and To qualify, a contribution must be

entity, attach a copy of the statement employment start date. If the credit made directly to, or specifically

received from the passthrough entity. is received through a passthrough designated for the exclusive use of, a

entity, attach a copy of the statement qualifying school.

Line 12b. Enter the number of received from the passthrough entity. School network or organization.

eligible interns employed during the

2024 tax year. Disregard this line Line 15b. Enter the number of If a contribution is made payable

if the credit is from a passthrough eligible employees whose first 12 to the account or fund of a school

entity. months of employment ended during network or organization that governs

the partnership’s 2024 tax year. or benefits multiple schools, the

Line 12c. Enter on this line the contribution will qualify only if the

total compensation paid to eligible Line 15c. Enter the total partnership specifically designates it

interns during the 2024 tax year (as compensation paid to the eligible for the use of a qualifying school, and

shown on their 2024 Form W-2s). employees’ during their first 12 the network or organization separately

Disregard this line if the credit is from consecutive months of employment accounts for the funds on behalf of

a passthrough entity. ending in the partnership’s 2023 tax that school. The partnership must

year.

Line 13 obtain a statement from the network

or organization that identifies the

Research expense tax credit Line 16 qualifying school and the amount

A credit is allowed for conducting Credit for wages paid to a contributed to it. If the qualifying

qualified research in North Dakota. For mobilized employee school falls into both the primary and

details, see N.D.C.C. § 57-38-30.5. Enter on this line the amount from high school categories, also see the

Enter the allowable credit on this line. Schedule ME, line 13. N.D.C.C. next paragraph.

Attach a statement showing the § 57-38-31. Attach Schedule ME.

computation of the base amount Schools in both primary and high

and the credit. Lines 17 through 19 school categories. If a contribution

Line 14 Nonprofit private school tax is made to a qualifying school that

Endowment fund tax credit credits provides education in one or more

A tax credit is allowed for making a Tax credits are allowed under grades in both the primary school

contribution to a qualified endowment N.D.C.C. § 57-38-01.7 for making category (kindergarten through 8th

fund. For more information, charitable contributions to qualifying grades) and the high school category

see Schedule QEC (for filers of nonprofit private primary schools, (9th through 12th grades), a separate

Forms 38, 40, 58, and 60) Attach high schools, and colleges located credit is allowed for the portion of the

Schedule QEC. in North Dakota. A separate credit contribution designated for use within

is allowed for each of the three each school category. The partnership

Lines 14a and 14b. Enter on these categories of school—primary school, must obtain a statement from the

lines the applicable amounts from high school, and college. For each

Schedule QEC.

|

Enlarge image |

9

qualifying school or the school Attach a copy of the Participating Unused credit: There is no carryover

network or organization that identifies Angel Investor Investment provision to succeeding tax years.

the qualifying school and shows Statement.

Line 24

the amount contributed within each

Line 21 Apprentice tax credit

category of school. If the partnership

Automation tax credit A tax credit is available for

does not obtain a statement, one-

If the partnership qualified for the compensation paid by a partnership

half of the total contribution will be

automation tax credit under N.D.C.C. to an apprentice. The credit equals

deemed to have been made to each

§ 57-38-01.41, enter on this line the 10% of the stipend or salary paid to

category of school.

amount of the credit shown on the a qualified apprentice employed in

Line 17. Enter on this line the credit approval letter issued to the North Dakota. The apprentice must be

allowable credit for contributions to partnership by the Office of State Tax in an apprenticeship program certified

qualified nonprofit private primary Commissioner. by the U.S. Department of Labor or

schools. be an electrical apprentice registered

Line 22 under North Dakota law. The credit

Line 18. Enter on this line the Credit for hiring an individual is allowed for up to five apprentices

allowable credit for contributions with a developmental disability or employed by the partnership at the

to qualified nonprofit private high mental illness same time.

schools. A tax credit is available for employing

an individual with a developmental Lifetime credit limit: A taxpayer is

Line 19. Enter on this line the disability or mental illness. To allowed no more than $3,000 in total

allowable credit for contributions to qualify, an employer must apply for tax credits for eligible wages paid in

qualified nonprofit private colleges. and obtain certification from the all tax years.

Line 20 North Dakota Department of Human

Line 24a.

Angel investor investment credit Services, Vocational Rehabilitation

Enter the allowable credit on this line.

Division, that the individual has a

Important! This line is only for severe disability, is eligible for the Attach a schedule listing the names

credits attributable to investments agency’s services, and requires of the employees, their social security

made in qualified businesses customized or supported employment numbers, wages paid and employment

by angel funds organized and to become employed. The credit is start date. If the credit is received

certified on or after July 1, 2017. equal to 25% of the wages paid to the through a passthrough entity, attach

If a partnership is a member of a individual during the tax year, up to a a copy of the statement received from

North Dakota angel fund that is maximum credit of $1,500 per year. the passthrough entity.

organized and certified on or after The credit is allowed for each eligible

July 1, 2017, a credit is allowed to individual hired. Attach a copy Line 24b.

the partnership if it participates in of the certification letter from Enter the number of eligible

a qualified investment made by the Human Services. apprentices employed during the 2024

tax year. Disregard this line if the

angel fund in a qualified business. Line 23 credit is from a passthrough entity.

The angel fund is required to provide Maternity home, child placing

a Participating Angel Investor agency, or pregnancy help center Line 24c.

Statement to the partnership, tax credit Enter the total amount of wages,

which evidences the partnership’s A tax credit is allowed for salaries, or other compensation paid

investment. For qualified investments contributions to the following to eligible apprentices employed

made after June 30, 2017, that fall organizations: (1) a child placing during the 2024 tax year (as shown

into the partnership’s 2024 tax year, agency licensed by the North Dakota on their 2024 Form W-2’s). Disregard

multiply the investment amount Department of Health and Human this line if the credit is from a

by the applicable credit rate shown Services (DHS), (2) a nonprofit passthrough entity.

on the statement. If a partnership maternity home located in North Line 25

participates in more than one qualified Dakota, or (3) a pregnancy help Professional service partnership

investment during the tax year, center recognized by DHS. guaranteed payments

calculate the credit separately for each

Participating Angel Investor Statement The credit is equal to 100% of the Lines 25a through 25c apply only

received and add the separately contribution and is limited to 50% of if the partnership marked “Yes” to

calculated amounts. a taxpayer’s tax liability. Enter on this Item H on page 1 of Form 58. See

line the amount from Schedule MCP, the instructions to Form 58, page 1,

Enter the credit amount on this line 8. Attach Schedule MCP. Item H, on page 5.

line. Do not enter on this line

an angel investor credit from The credit is available to corporations, Line 25a. Enter the total guaranteed

a North Dakota Schedule K-1. individuals, estates, trusts, and payments from Federal Form 1065,

A partnership is not allowed to passthrough entities. A tax credit Schedule K, line 4.

claim an angel investor credit from earned by a passthrough entity is Line 25b. Enter the portion of the

another passthrough entity. See passed through and allowed to each amount on line 25a that was made to

N.D.C.C. § 57-38-01.26 (effective owner in proportion to their respective individual partners as a reasonable

for investments made after June 30, interests in the passthrough entity.

2017).

|

Enlarge image |

10

salary for personal services, completing lines 26a and 26b, the

regardless of where the services partnership must attach the following Instructions for

were performed. Do not include any to Form 58: Schedule KP

guaranteed payments for other than

• A statement on which each item

personal services. (Form 58, page 5)

of nonbusiness income is shown Schedule KP must be completed

Line 25c. Enter the portion of the along with its related expenses. to provide information about each

amount on line 25b that was made • A statement explaining the basis partner. If the partnership has more

to nonresident individual partners for for treating the item of income than seven partners, complete and

personal services performed within as nonbusiness income subject to attach additional schedules as needed

North Dakota. allocation. to list all partners. If more than one

Line 26 • If an item of nonbusiness income Schedule KP is needed, complete

Allocable nonbusiness income is allocated to a state other than lines 1 through 4 on only one of them,

Lines 26a and 26b apply only if the North Dakota, a copy of that other and include the combined amount

partnership meets all of the following: state’s income tax return must for all of the schedules on that one

be attached. If the partnership is schedule.

• It is a multistate partnership, i.e., not required to file an income tax

it carries on its trade or business return with the other state, the All partners

activity both within and without partnership must indicate this in (Columns 1 through 5)

North Dakota. the attached statement. Columns 1 and 2

• It has one or more nonresident Enter the name, mailing address, and

individual, estate, or trust Line 26a. Enter the total allocable

partners. income (less related expenses) partner’s identifying number as shown

from all sources within and without on the partner’s Federal Schedule K-1.

• It has allocable nonbusiness North Dakota. If the partner is a single member

income. Generally, all income LLC that is a disregarded entity for

received by a partnership is Line 26b. Enter the portion of the federal income tax purposes, enter

considered business income unless amount on line 24a that is allocable to the owner’s name, address, and

clearly classifiable as nonbusiness North Dakota. identifying number.

income. The classification of

Line 27

income by the labels used to Column 3

Disposition of I.R.C. Section 179

describe it—for example, interest, Identify the entity type of the partner

property

dividends, rents, royalties, by entering the applicable code letter

Lines 27a through 27b apply only if

operating income, or nonoperating as follows:

the partnership sold, exchanged, or

income—is generally not relevant Entity type Code letter

disposed of property for which an

in determining whether income is Individual ..................... I

I.R.C. Section 179 deduction was

business or nonbusiness income. C corporation ................ C

passed through to the partners.

For more information, see N.D. S corporation ................ S

Note: The partnership is required

Admin. Code § 81-03-09-03. Partnership ................... P

to report this same information on

Nonbusiness income is not a separate statement attached to Estate .......................... E

apportioned using the apportionment Federal Form 1065, Schedule K, Trust ............................ T

factor (from Schedule FACT) but is line 20c. Exempt organization ...... O

allocated within or without North Note: A “C corporation” is a

For lines 27a through 27d, multiply

Dakota as provided under N.D.C.C. corporation that files Federal

the corresponding combined amount

§§ 57-38.1-04 through 57-38.1-08 Form 1120; an “S corporation”

for all partners as reported on

and N.D. Admin. Code is a corporation that files Federal

Federal Form 1065, Schedule K,

§ 81-03-09-09. Expenses must be Form 1120S; and the “Trust” entity

line 20c, by the apportionment factor

attributed to the nonbusiness income type applies to a trust that files

from Schedule FACT, line 14, and

in a manner which fairly distributes Federal Form 1041 or, in lieu of

enter the result. However, if the

all of the partnership’s expenses to its filing Federal Form 1041, elects an

property disposed of is treated as a

business and nonbusiness income. alternative reporting method under

nonbusiness asset the gain or loss

If the partnership has an item of from which is subject to allocation the federal income tax regulations,

nonbusiness income subject to under N.D.C.C. §§ 57-38.1-04 through and to an IRA (generally filing Federal

allocation, the partnership must take 57-38.1-08, subtract the amounts Form 990-T to report Unrelated

this into account when calculating for that asset before multiplying by Business Taxable Income.)

the North Dakota distributive share the apportionment factor. Include the If the partner is an LLC that is a

of income or loss reportable on nonbusiness gain or loss from the disregarded entity for federal income

Schedule KP and Schedule K-1 disposition on Form 58, Schedule K, tax purposes or a nominee on Federal

(Form 58). See the instructions to line 26. Schedule K-1, enter the code letter

Schedule KP, Column 6, on page 10 for the type of entity of the entity’s

for more information. In addition to owner. If the LLC is treated like a

|

Enlarge image |

11

C corporation, partnership, or S

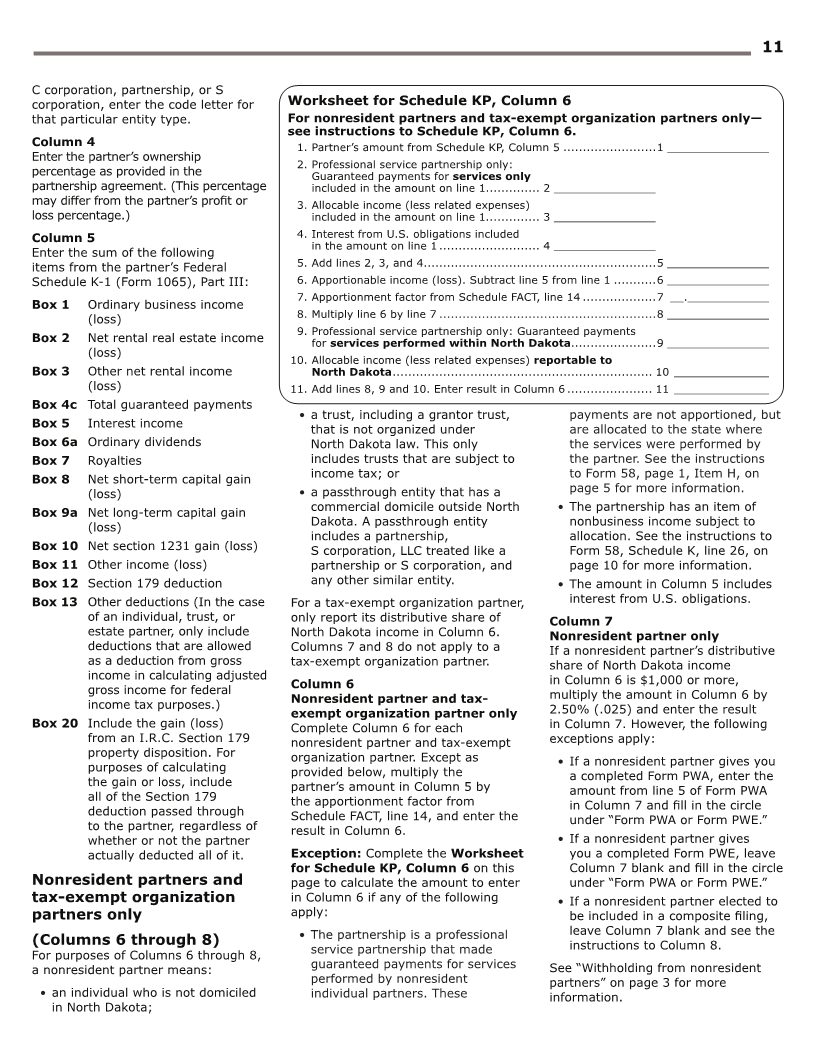

corporation, enter the code letter for Worksheet for Schedule KP, Column 6

that particular entity type. For nonresident partners and tax-exempt organization partners only—

see instructions to Schedule KP, Column 6.

Column 4 1. Partner’s amount from Schedule KP, Column 5 ........................1 _______________

Enter the partner’s ownership

2. Professional service partnership only:

percentage as provided in the Guaranteed payments for services only

partnership agreement. (This percentage included in the amount on line 1.............. 2 _______________

may differ from the partner’s profit or 3. Allocable income (less related expenses)

loss percentage.) included in the amount on line 1.............. 3 _______________

Column 5 4. Interest from U.S. obligations included

in the amount on line 1 .......................... 4 _______________

Enter the sum of the following

items from the partner’s Federal 5. Add lines 2, 3, and 4 ............................................................5 _______________

Schedule K-1 (Form 1065), Part III: 6. Apportionable income (loss). Subtract line 5 from line 1 ...........6 _______________

7. Apportionment factor from Schedule FACT, line 14 ...................7 __.____________

Box 1 Ordinary business income

(loss) 8. Multiply line 6 by line 7 ........................................................8 _______________

9. Professional service partnership only: Guaranteed payments

Box 2 Net rental real estate income for services performed within North Dakota ......................9 _______________

(loss) 10. Allocable income (less related expenses) reportable to

Box 3 Other net rental income North Dakota ................................................................... 10 ______________

(loss) 11. Add lines 8, 9 and 10. Enter result in Column 6 ...................... 11 ______________

Box 4c Total guaranteed payments

• a trust, including a grantor trust, payments are not apportioned, but

Box 5 Interest income that is not organized under are allocated to the state where

Box 6a Ordinary dividends North Dakota law. This only the services were performed by

Box 7 Royalties includes trusts that are subject to the partner. See the instructions

Box 8 Net short-term capital gain income tax; or to Form 58, page 1, Item H, on

(loss) • a passthrough entity that has a page 5 for more information.

Box 9a Net long-term capital gain commercial domicile outside North • The partnership has an item of

(loss) Dakota. A passthrough entity nonbusiness income subject to

includes a partnership, allocation. See the instructions to

Box 10 Net section 1231 gain (loss) S corporation, LLC treated like a Form 58, Schedule K, line 26, on

Box 11 Other income (loss) partnership or S corporation, and page 10 for more information.

Box 12 Section 179 deduction any other similar entity. • The amount in Column 5 includes

Box 13 Other deductions (In the case For a tax-exempt organization partner, interest from U.S. obligations.

of an individual, trust, or only report its distributive share of Column 7

estate partner, only include North Dakota income in Column 6. Nonresident partner only

deductions that are allowed Columns 7 and 8 do not apply to a If a nonresident partner’s distributive

as a deduction from gross tax-exempt organization partner. share of North Dakota income

income in calculating adjusted in Column 6 is $1,000 or more,

gross income for federal Column 6

income tax purposes.) Nonresident partner and tax- multiply the amount in Column 6 by

exempt organization partner only 2.50% (.025) and enter the result

Box 20 Include the gain (loss) Complete Column 6 for each in Column 7. However, the following

from an I.R.C. Section 179 nonresident partner and tax-exempt exceptions apply:

property disposition. For organization partner. Except as • If a nonresident partner gives you

purposes of calculating provided below, multiply the a completed Form PWA, enter the

the gain or loss, include partner’s amount in Column 5 by amount from line 5 of Form PWA

all of the Section 179 the apportionment factor from in Column 7 and fill in the circle

deduction passed through Schedule FACT, line 14, and enter the under “Form PWA or Form PWE.”

to the partner, regardless of result in Column 6.

whether or not the partner • If a nonresident partner gives

actually deducted all of it. Exception: Complete the Worksheet you a completed Form PWE, leave

for Schedule KP, Column 6 on this Column 7 blank and fill in the circle

Nonresident partners and page to calculate the amount to enter under “Form PWA or Form PWE.”

tax-exempt organization in Column 6 if any of the following • If a nonresident partner elected to

partners only apply: be included in a composite filing,

• The partnership is a professional leave Column 7 blank and see the

(Columns 6 through 8) instructions to Column 8.

For purposes of Columns 6 through 8, service partnership that made

a nonresident partner means: guaranteed payments for services See “Withholding from nonresident

performed by nonresident partners” on page 3 for more

• an individual who is not domiciled individual partners. These information.

in North Dakota;

|

Enlarge image |

12

Column 8 Line 8 Interest. Calculate the interest

Nonresident partner only Application of overpayment to amount as follows:

Note: Leave Column 8 blank if 2025

• If an extension of time to file

Column 7 was completed for the If there is an overpayment on line 7,

Form 58 was obtained, extension

nonresident partner. the partnership may elect to apply

interest is calculated at the rate of

part or all of it as an estimated

12% per year on any tax due from

Complete Column 8 for each payment toward its 2025 tax liability.

the due date of the return to the

nonresident partner electing to To make the election, enter the

earlier of the extended due date or

be included in a composite filing. portion of line 7 to be applied on

the date the return was filed.

Multiply the amount in Column 6 by line 8. If this election is made, the

2.50% (.025) and enter the result in election and the amount applied may • If the total amount of tax due

Column 8. If the amount in Column 6 not be changed after the return is is not paid by the due date (or

is zero or less, enter zero in Column 8. filed. If this is an amended return, do extended due date) of the return,

See “Composite filing” on page 3 for not make an entry on this line. interest is calculated at the rate

more information. of 1% per month or fraction of a

Line 10 month on the unpaid tax, except

Specific line Tax due for the month in which the return

A tax due must be paid in full with the was due.

instructions for return when the return is filed. See

the instructions to line 12 for payment Line 12

page 1 of options. Balance due

The balance due must be paid in full

Form 58, lines 1-12 Line 11 with the return. The payment may

Complete Schedule FACT, Penalty and interest be made electronically in one of the

The Office of State Tax Commissioner following ways:

Schedule K, and Schedule KP will notify the partnership of any

before completing lines 1 penalty and interest payable on a tax • Online—A payment may be made

through 12 on page 1 of due shown on Form 58. However, the online with an electronic check or a

Form 58. partnership may calculate the penalty debit or credit card. The electronic

and interest amounts and include check option is free. North Dakota

Line 4 them in the balance due on Form 58. contracts with a national payment

Income tax withholding service to provide the debit or

Enter the North Dakota income Penalty. Calculate the penalty credit card option. There is a fee

tax withholding shown on a 2024 amount as follows: for the debit or credit option, none

Form 1099 or North Dakota • If Form 58 is filed by the due date of which goes to the State of North

Schedule K-1. Be sure the state (or extended due date), but the Dakota. To pay online, go to

identified on the Form 1099 is total amount of tax due is not paid www.tax.nd.gov/payment.

North Dakota. Also enter the with the return, the penalty is • Electronic funds transfer—A

North Dakota income tax withholding equal to 5% of the unpaid tax or payment may be made by means

shown on a 2023 North Dakota $5.00, whichever is greater. of an Automated Clearing House

Schedule K-1 if the entity that issued

it has a fiscal tax year ending in • If Form 58 is filed after its due (ACH) credit transaction that

the partnership’s 2024 tax year. Do date (or extended due date), and the taxpayer initiates through

not enter on this line North Dakota there is an unpaid tax due on it, a its banking institution. For more

extraction or production taxes penalty equal to 5% of the unpaid information, go to our website at

withheld from mineral interest income, tax due (with a $5.00 minimum) tax.nd.gov.

such as an oil or gas royalty, because applies for the month the return

If paying with a paper check or money

they are not income taxes. Attach a was due, plus 5% of the unpaid

order, complete a 2024 Form 58-PV

copy of the Form 1099 or tax due (with a $5.00 minimum)

payment voucher and enclose it with

North Dakota Schedule K-1. for each month or fraction of a

the payment. Make the check or

month the return remains unfiled,

money order payable to “ND State

Line 5 not to exceed the greater of 25%

Tax Commissioner,” and write the last

Estimated tax payments of the unpaid tax due or $25.00.

Enter the amount paid with the 2024 four digits of the partnership’s FEIN

Forms 58-EXT and 58-ES plus any and “2024 Form 58” on the check or

overpayment applied from the 2023 money order. A check must be drawn

Form 58. However, if filing an amended on a U.S. or Canadian bank, be in U.S.

return, do not enter any previously dollars, and use a standard nine-digit

paid estimated tax amount; instead, routing number. A check drawn on a

enter the amount of the total taxes foreign bank (except one in Canada)

due from line 3 of the previously filed cannot be accepted.

original or amended return.

|

Enlarge image |

13

Amended schedule. If a partnership Lines 3 through 5. Enter on the

Instructions files an amended Form 58, the corresponding lines the partner’s

for completing partnership must issue amended share of each amount shown on

North Dakota Schedule K-1 forms to Form 58, Schedule K, lines 3

Schedule K-1 its partners. Fill in the “Amended” through 5.

A partnership is not subject to circle at the top of the North Dakota

Line 6. Enter on this line the amount

North Dakota income tax. Instead, Schedule K-1 (Form 58).

determined by multiplying the amount

the partners are responsible for Final schedule. Fill in the “Final” on Form 58, Schedule K, line 6, by the

reporting and paying any applicable circle at the top of the North Dakota same percentage used to determine

North Dakota income tax on their Schedule K-1 (Form 58) if it is the last the partner’s distributive share of

shares of the partnership’s income one to be issued by the partnership to income (loss) from the partnership.

reportable to North Dakota. the partner.

Lines 7 through 24 Enter on the

The North Dakota Schedule K-1 Part 2 corresponding lines the partner’s

(Form 58) must be used by a share of each amount shown on

partnership to provide its partners Partner information

Form 58, Schedule K, lines 7 through

with information they will need to Item E 24. Also, for the following lines,

complete a North Dakota income Enter the code letter for the partner additional supporting information

tax return. The information to be from Form 58, Schedule KP, Column 3. must be provided with Schedule K-1.

included in the schedule will depend

on the type of partner. In the case of Item F Lines 8 and 9. Provide a statement

certain credits reported on Schedule If the partner is an individual, estate, identifying the qualified business

K-1 (Form 58), additional supporting or trust, fill in the applicable circle to or qualified agricultural commodity

information must be provided with indicate the legal residency status of processing facility in which the

Schedule K-1 — see the instructions the partner for North Dakota income qualifying investment was made.

to Part 3. tax purposes. If an individual partner

changed his or her legal residency Line 14. Provide a statement

A North Dakota Schedule K-1 (Form to or from North Dakota during the identifying the qualified nonprofit

58) must be completed and given to: tax year, mark the part-year resident organization and the qualified

status. In the case of an estate or trust endowment fund to which the

• Each nonresident partner for qualifying contribution was made.

partner, only the full-year resident or

which the partnership is required

full-year nonresident status will apply.

to report the North Dakota Line 20. Provide a statement

distributive share of income on Item G identifying the angel fund that made

Form 58, Schedule KP, Column 6. For an eligible nonresident partner, the qualified investment in the

• Each partner to which a share of indicate whether the partner is qualified business.

a North Dakota adjustment or tax included in a composite filing by filling Part 4

credit from Form 58, Schedule K, in the applicable circle.

Nonresident individual,

lines 1 through 24, is distributable. Item I estate, or trust partner

• Each partnership or corporation Enter the partner’s ownership only — North Dakota income

partner for the purpose of percentage from Form 58,

reporting a share of the Schedule KP, Column 4. (loss)

apportionment factors from Complete Part 4 for a nonresident

Form 58, Schedule FACT. Part 3 individual, estate, or trust partner.

• Each tax-exempt organization All partners—

Line 25

partner. North Dakota adjustments Partnership’s apportionment

If there are no North Dakota and tax credits factor

If there are any North Dakota

adjustments or tax credits on Form 58, Enter the partnership’s apportionment

adjustments or tax credits on

Schedule K, lines 1 through 24, a factor from Form 58, Schedule FACT,

Form 58, Schedule K, lines 1

North Dakota Schedule K-1 does not line 14.

through 24, complete this part for all

have to be given to a North Dakota Lines 26 through 39

partners.

resident individual, estate, or trust. Income and loss items

Lines 1 and 2. Enter on the

In addition to the North Dakota Except as provided under

corresponding lines the amount

Schedule K-1 (Form 58), the Exceptions 1 through 3 below,

determined by multiplying each

partnership must provide the multiply the corresponding

amount shown on Form 58,

partner with a copy of the Partner’s amount from the partner’s Federal

Schedule K, lines 1 and 2, by the

Instructions for North Dakota Schedule K-1, Part III, boxes 1 through

same percentage used to determine

Schedule K-1 (Form 58). 13, and any I.R.C. § 179 property

the partner’s distributive share of disposition gain (loss) included in box

A copy of all North Dakota income (loss) from the partnership. 20 by the partnership’s apportionment

Schedule K-1 forms must be enclosed factor from Schedule FACT, line 14, and

with Form 58 along with any required enter the result on the corresponding

supporting statements. line of Part 4, lines 26 through 39.

|

Enlarge image |

14

For “Other deductions” from box 13 If the calculation of any amount on Line 44

of Federal Schedule K-1, only include lines 26 through 39 of Part 4 was Total factors

deductions that are allowed as a affected by the removal or inclusion Enter in the corresponding column the

deduction from gross income in of net nonbusiness income, attach partner’s share of the partnership’s

calculating adjusted gross income for a statement to the partner’s North total factor amounts from Form 58,

federal income tax purposes. Dakota Schedule K-1 (Form 58) Schedule FACT, Column 1, lines 7, 8,

identifying the net nonbusiness and 12.

For purposes of calculating the gain income and showing the calculation of