Enlarge image

2024 INSTRUCTIONS FOR FILING RI-1040NR

(FOR RHODE ISLAND NONRESIDENTS OR PART-YEAR RESIDENTS FILING FORM RI-1040NR)

WHAT’S NEW FOR TAX YEAR 2024

Each year the RI Division of Taxation is required to make an inflationary adjustment for the following amounts:

• Standard deduction amounts (see page I-4 for the increased amounts)

• Exemption amount (see page I-5 for the increased amount)

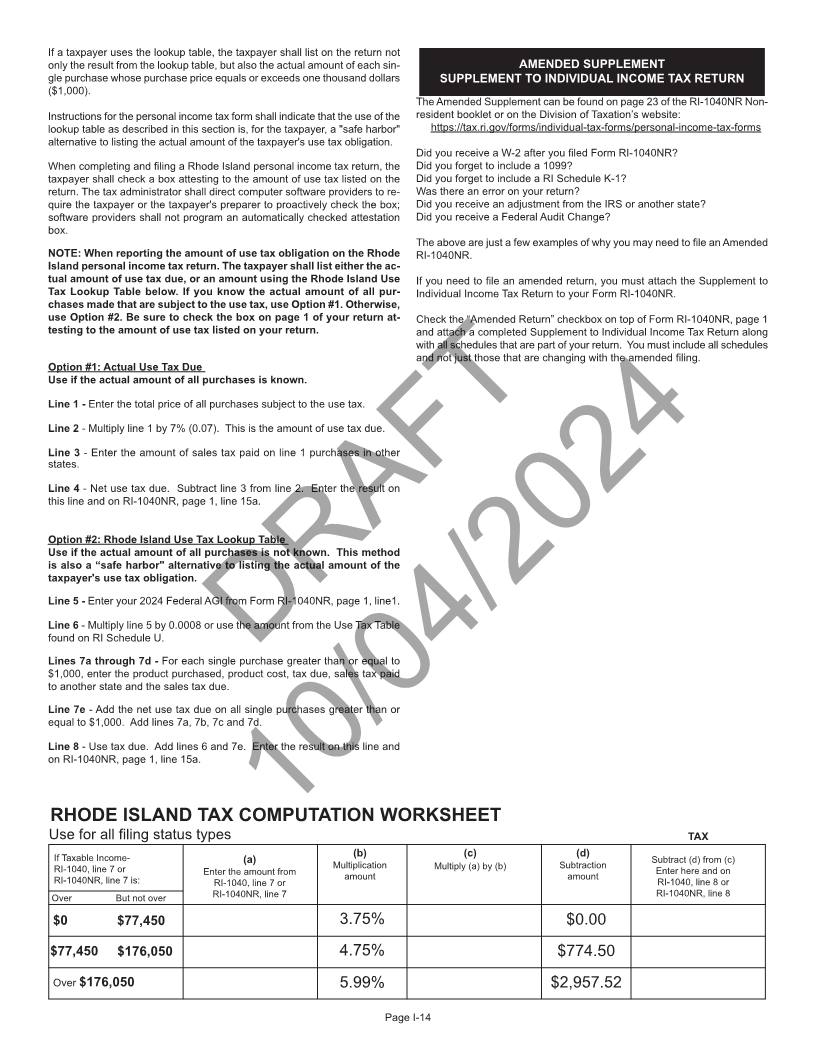

• Income tax brackets (see page I-14 for the new tiers)

• Increased Standard Deduction and Exemption phaseout amount (see pages I-4 and I-5 for the increased amount)

• Federal AGI amounts for the social security modification (see worksheet on page 18)

• Federal AGI amounts for the pension and annuity modification (see instructions starting on page I-12)

Additional changes for tax year 2024 include:

• New Charitable Contribution Check-off for Behavioral Health Education, Training and Coordination Fund (see instructions on page I-6)

• Discontinuance of exemption for Medicaid recipients on Form IND-HEALTH (see instructions on page IND-6)

GENERAL INSTRUCTIONS

The RI-1040NR Nonresident booklet contains returns and instructions for only for a limited time even if it is for a relatively long duration. For a married

filing the 2024 Rhode Island Nonresident Individual Income Tax Return. couple, normally both individuals have the same domicile. Any person as-

Read the instructions in this book carefully. For your convenience we have serting a change in domicile must show:

provided line by line instructions which will aid you in completing your return. (1) an intent to abandon the former domicile,

Please print or type so that it will be legible. Fillable forms are available on (2) an intent to acquire a new domicile and

our website at: (3) actual physical presence in a new domicile.

https://tax.ri.gov/forms/individual-tax-forms/personal-income-tax-forms.

Check the accuracy of your name(s), address, social security number(s),

and the federal identification numbers listed on RI Schedule W. INCOME OF A NONRESIDENT SUBJECT TO TAX

A nonresident is subject to tax on all items included in his or her total fed-

These instructions are for the use of non-resident and part-year resident tax- eral income (including his or her distributive share of partnership income or

payers only. Full Year resident taxpayers will file their individual income tax gain and his or her share of estate or trust income or gain) which are derived

returns on Form RI-1040. Resident forms and instructions are available from or connected with Rhode Island sources as follows:

upon request at the Rhode Island Division of Taxation and on our website •From real or tangible personal property located in the state.

at: https://tax.ri.gov/forms/individual-tax-forms/personal-income-tax-forms. •From a business, trade, profession or occupation carried on in the

state.

Complete your 2024 Federal Income Tax Return first. •From services performed in the state.

It is the basis for preparing your Rhode Island tax return. The Rhode Is- •Winnings and prizes from the Rhode Island lottery and other gam-

land tax is based on your federal adjusted income. bling establishments in this state.

Accuracy and attention to detail in completing the return in accordance •A nonresident is not subject to tax on the following classes of in-

with these instructions will facilitate the processing of your tax return. You come even though included in total federal income:

may find the following points helpful in preparing your Rhode Island Personal •Annuities, interest, dividends or gains from the sale or exchange

Income Tax Return. of intangible personal property unless they are part of the income from

any business, trade, profession or occupation carried on in this state

by the nonresident taxpayer.

WHO MUST FILE A RETURN DRAFT •Compensation received for active service in the military forces of

Every nonresident individual required by the laws of the United States to the United States.

file a federal income tax return who has income derived from or connected

with Rhode Island sources must file a Rhode Island individual income tax

return. Nonresidents should complete page 13, Schedule II. INCOME TERMS DEFINED

Every part-year individual who was a resident for a period of less than 12 In these instructions “total federal income” is federal adjusted gross in-

months is required to file a Rhode Island return if he or she is required to file come as defined in the United States Internal Revenue Code (IRC) and ap-

a federal return. Part-year residents should complete page 15, Schedule III. plicable regulations. “Total income from Rhode Island sources” is that portion

Nonresident and part-year resident individuals who are not required to file of your total federal income derived from or connected with Rhode Island

a federal income tax return may be required to file a Rhode Island individual sources. “Total Rhode Island income” is your total income from Rhode Island

income tax return if he or she has Rhode Island modifications increasing sources after making the additions and subtractions described later in these

their Federal Adjusted Gross income. instructions. Total Rhode Island income of a part-year resident includes total

These schedules can be found on the Division of Taxation’s website at: income from Rhode Island sources for the entire year plus other income re-

https://tax.ri.gov/forms/individual-tax-forms/personal-income-tax-forms. 10/04/2024ceived during period of residence in Rhode Island after making the additions

and subtractions described later in these instructions.

DEFINITION OF RESIDENT AND NONRESIDENT

RESIDENT: a person (a)who is domiciled in the State of Rhode Island or

(b) who, even though domiciled outside Rhode Island, maintains a perma- JOINT AND SEPARATE RETURNS

nent place of abode within the state and spends a total of more than 183 JOINT RETURNS: Generally, if two married individuals file a joint federal

days of the taxable year within the state. income tax return they also must file a joint Rhode Island income tax return.

NONRESIDENT: any person not coming within the definition of a resident. However, if either one of the married individuals is a resident and the other

For purposes of the above definition, domicile is found to be a place an in- is a non-resident, they must file separate returns, unless they elect to file a

dividual regards as his or her permanent home – the place to which he or joint return as if both were residents of Rhode Island. If the resident spouse

she intends to return after a period of absence. A domicile, once established, files separately in Rhode Island and a joint federal return is filed for both

continues until a new fixed and permanent home is acquired. No change of spouses, the resident spouse must compute income, exemptions, credits

domicile results from moving to a new location if the intention is to remain and tax as if a separate federal return had been filed.

Page I-1 Revised 09/2024