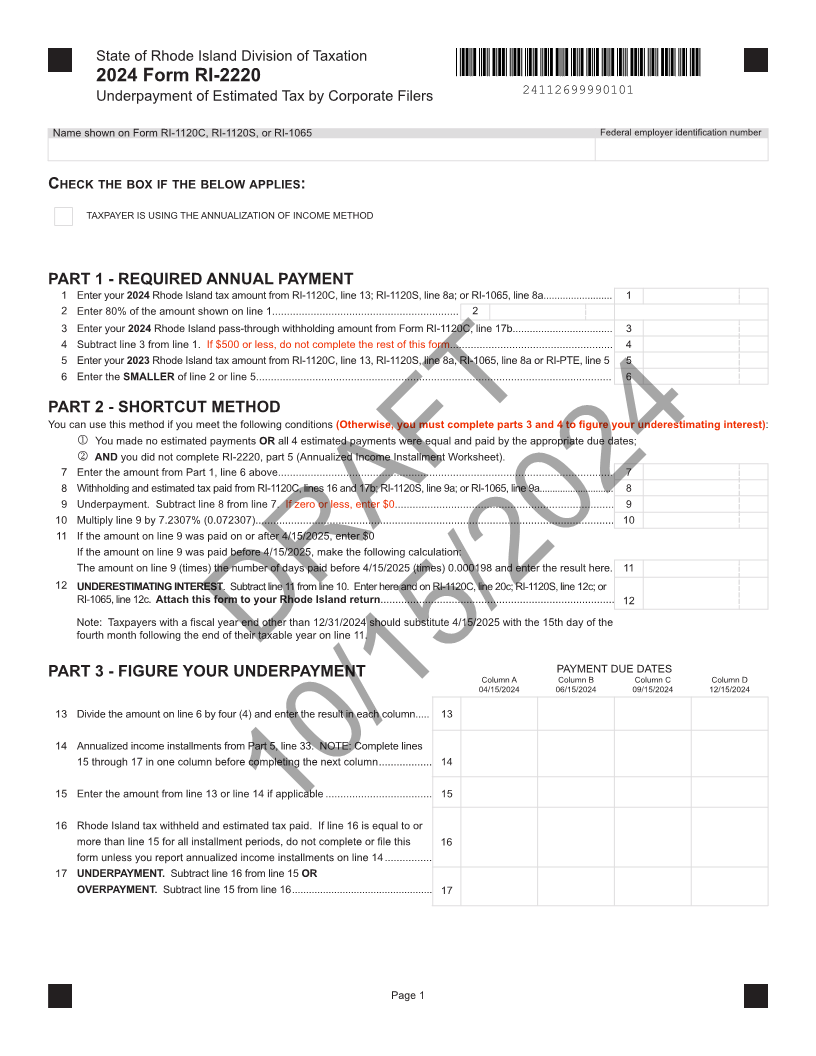

Enlarge image

State of Rhode Island Division of Taxation

2024 Form RI-2220

Underpayment of Estimated Tax by Corporate Filers 24112699990101

Name shown on Form RI-1120C, RI-1120S, or RI-1065 Federal employer identification number

CHECK THE BOX IF THE BELOW APPLIES :

TAXPAYER IS USING THE ANNUALIZATION OF INCOME METHOD

PART 1 - REQUIRED ANNUAL PAYMENT

1 Enter your 2024 Rhode Island tax amount from RI-1120C, line 13; RI-1120S, line 8a; or RI-1065, line 8a......................... 1

2 Enter 80% of the amount shown on line 1............................................................... 2

3 Enter your 2024 Rhode Island pass-through withholding amount from Form RI-1120C, line 17b................................... 3

4 Subtract line 3 from line 1. If $500 or less, do not complete the rest of this form....................................................... 4

5 Enter your 2023 Rhode Island tax amount from RI-1120C, line 13, RI-1120S, line 8a, RI-1065, line 8a or RI-PTE, line 5 5

6 EnterSMALLERthe of line 2 or line 5........................................................................................................................ 6

PART 2 - SHORTCUT METHOD

You can use this method if you meet the following conditions (Otherwise, you must complete parts 3 and 4 to figure your underestimating interest):

1 You made no estimated payments ORall 4 estimated payments were equal and paid by the appropriate due dates;

2 ANDyou did not complete RI-2220, part 5 (Annualized Income Installment Worksheet).

7 Enter the amount from Part 1, line 6 above................................................................................................................. 7

8 Withholding and estimated tax paid from RI-1120C, lines 16 and 17b; RI-1120S, line 9a; or RI-1065, line 9a............................. 8

9 Underpayment. Subtract line 8 from line 7. If zero or less, enter $0.......................................................................... 9

10 Multiply line 9 by 7.2307% (0.072307)......................................................................................................................... 10

11 If the amount on line 9 was paid on or after 4/15/2025, enter $0

If the amount on line 9 was paid before 4/15/2025, make the following calculation:

The amount on line 9 (times) the number of days paid before 4/15/2025 (times) 0.000198 and enter the result here. 11

12 UNDERESTIMATING INTEREST. Subtract line 11 from line 10. Enter here and on RI-1120C, line 20c; RI-1120S, line 12c; or

RI-1065, line 12c. Attach this form to your Rhode Island return............................................................................... 12

Note: Taxpayers with a fiscal year end other than 12/31/2024 should substitute 4/15/2025 with the 15th day of the

fourth month following the end of their taxable year on line 11.

PART 3 - FIGURE YOUR UNDERPAYMENTDRAFT PAYMENT DUE DATES

Column A Column B Column C Column D

04/15/2024 06/15/2024 09/15/2024 12/15/2024

13 Divide the amount on line 6 by four (4) and enter the result in each column..... 13

14 Annualized income installments from Part 5, line 33. NOTE: Complete lines

15 through 17 in one column before completing the next column.................. 14

15 Enter the amount from line 13 or line 14 if applicable .................................... 15

16 Rhode Island tax withheld and estimated tax paid. If line 16 is equal to or

more than line 15 for all installment periods, do not10/15/2024complete or file this 16

form unless you report annualized income installments on line 14................

17 UNDERPAYMENT. Subtract line 16 from line 15 OR

OVERPAYMENT. Subtract line 15 from line 16.................................................. 17

Page 1