Enlarge image

State of Rhode Island Division of Taxation

2024 RI Schedule CR-PT

Other Rhode Island Credits for RI-1065 & RI-1120S IMAGEONLY

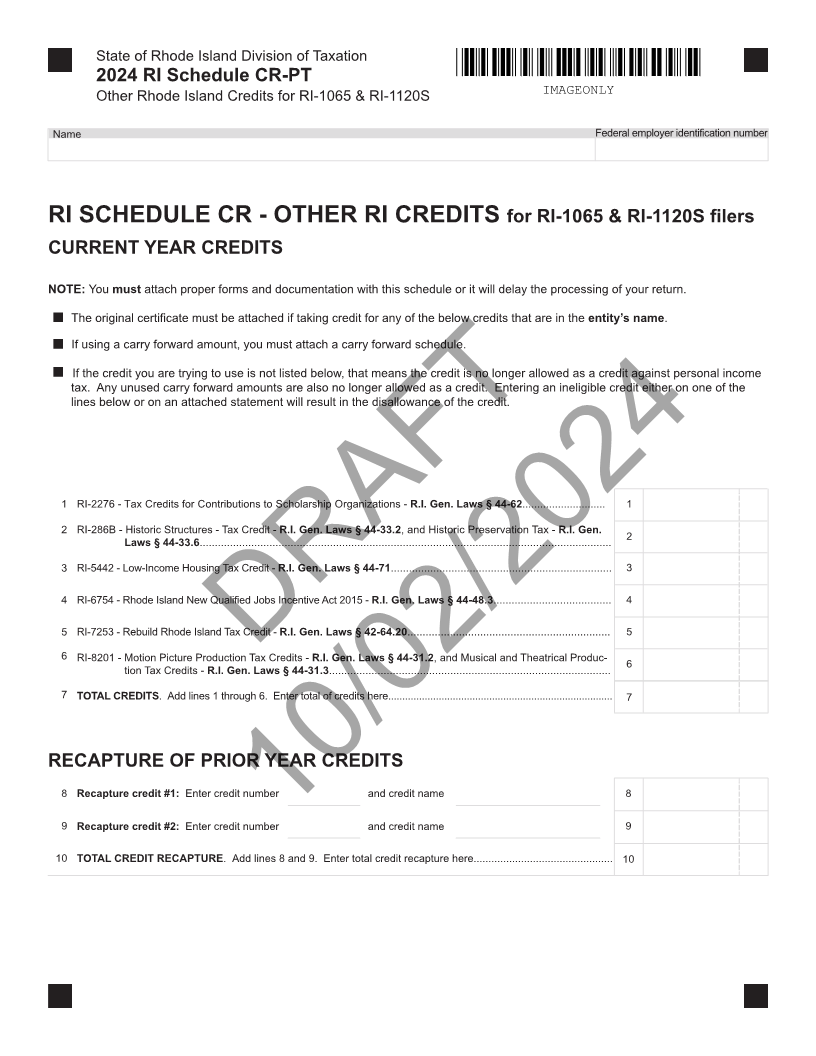

Name Federal employer identification number

RI SCHEDULE CR - OTHER RI CREDITS for RI-1065 & RI-1120S filers

CURRENT YEAR CREDITS

NOTE: mustYou attach proper forms and documentation with this schedule or it will delay the processing of your return.

The original certificate must be attached if taking credit for any of the below credits that are in theentity’s. name

If using a carry forward amount, you must attach a carry forward schedule.

If the credit you are trying to use is not listed below, that means the credit is no longer allowed as a credit against personal income

tax. Any unused carry forward amounts are also no longer allowed as a credit. Entering an ineligible credit either on one of the

lines below or on an attached statement will result in the disallowance of the credit.

1 RI-2276 - Tax Credits for Contributions to Scholarship Organizations - R.I. Gen. Laws § 44-62............................ 1

2 RI-286B - Historic StructuresR.I. Gen.-Laws §Tax Credit - 44-33.2, and Historic Preservation Tax - R.I. Gen. 2

Laws § 44-33.6........................................................................................................................................

3 RI-5442 - Low-Income Housing Tax Credit - R.I. Gen. Laws § 44-71......................................................................... 3

4 RI-6754 - Rhode Island New Qualified Jobs Incentive Act 2015 - R.I. Gen. Laws § 44-48.3....................................... 4

5 RI-7253 - Rebuild Rhode Island Tax Credit - R.I. Gen. Laws § 42-64.20................................................................... 5

6

RI-8201 - Motion Picture Production Tax CreditsDRAFT-R.I. Gen. Laws § 44-31.2,and Musical and Theatrical Produc- 6

tion Tax Credits - R.I. Gen. Laws § 44-31.3.............................................................................................

7 TOTAL CREDITS . Add lines 1 through 6. Enter total of credits here................................................................................7

RECAPTURE OF PRIOR YEAR CREDITS

8 Recapture credit #1: Enter credit number and credit name 8

9 Recapture credit #2: Enter credit number and credit name 9

10/02/2024

10 TOTAL CREDIT RECAPTURE . Add lines 8 and 9. Enter total credit recapture here............................................... 10