Enlarge image

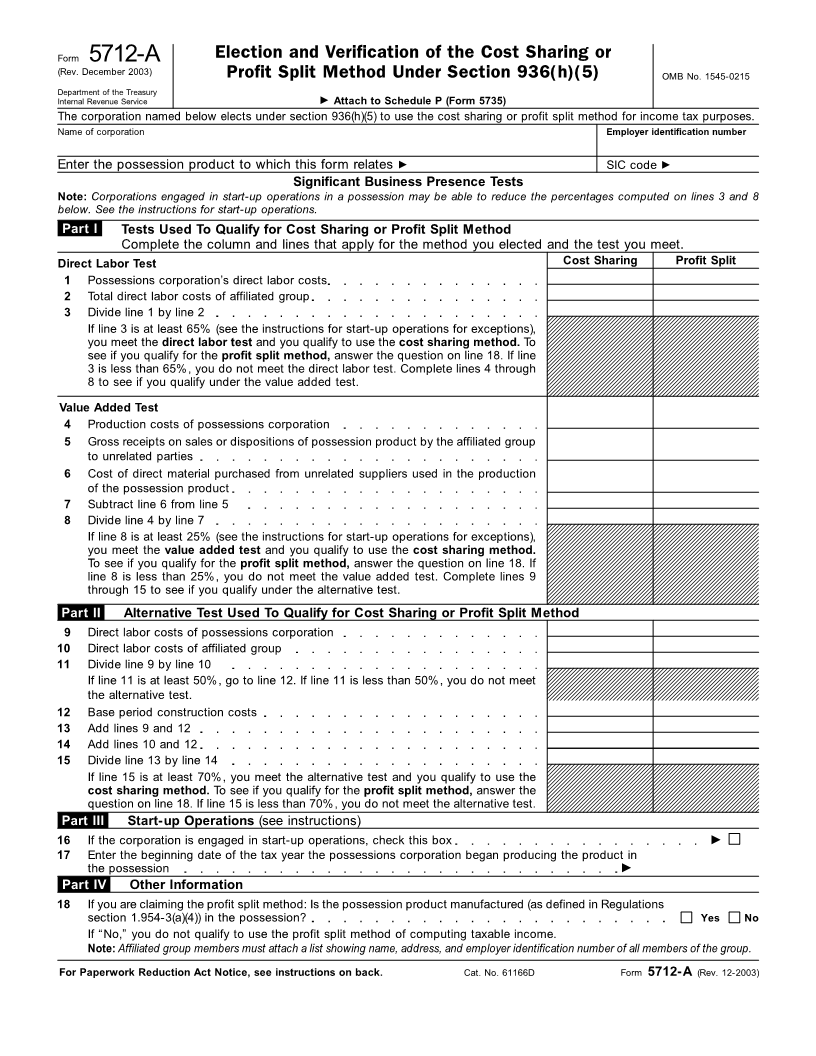

Form 5712-A Election and Verification of the Cost Sharing or

(Rev. December 2003) Profit Split Method Under Section 936(h)(5) OMB No. 1545-0215

Department of the Treasury

Internal Revenue Service Attach to Schedule P (Form 5735)

The corporation named below elects under section 936(h)(5) to use the cost sharing or profit split method for income tax purposes.

Name of corporation Employer identification number

Enter the possession product to which this form relates SIC code

Significant Business Presence Tests

Note: Corporations engaged in start-up operations in a possession may be able to reduce the percentages computed on lines 3 and 8

below. See the instructions for start-up operations.

Part I Tests Used To Qualify for Cost Sharing or Profit Split Method

Complete the column and lines that apply for the method you elected and the test you meet.

Direct Labor Test Cost Sharing Profit Split

1 Possessions corporation’s direct labor costs

2 Total direct labor costs of affiliated group

3 Divide line 1 by line 2

If line 3 is at least 65% (see the instructions for start-up operations for exceptions),

you meet the direct labor test and you qualify to use the cost sharing method. To

see if you qualify for the profit split method, answer the question on line 18. If line

3 is less than 65%, you do not meet the direct labor test. Complete lines 4 through

8 to see if you qualify under the value added test.

Value Added Test

4 Production costs of possessions corporation

5 Gross receipts on sales or dispositions of possession product by the affiliated group

to unrelated parties

6 Cost of direct material purchased from unrelated suppliers used in the production

of the possession product

7 Subtract line 6 from line 5

8 Divide line 4 by line 7

If line 8 is at least 25% (see the instructions for start-up operations for exceptions),

you meet the value added test and you qualify to use the cost sharing method.

To see if you qualify for the profit split method, answer the question on line 18. If

line 8 is less than 25%, you do not meet the value added test. Complete lines 9

through 15 to see if you qualify under the alternative test.

Part II Alternative Test Used To Qualify for Cost Sharing or Profit Split Method

9 Direct labor costs of possessions corporation

10 Direct labor costs of affiliated group

11 Divide line 9 by line 10

If line 11 is at least 50%, go to line 12. If line 11 is less than 50%, you do not meet

the alternative test.

12 Base period construction costs

13 Add lines 9 and 12

14 Add lines 10 and 12

15 Divide line 13 by line 14

If line 15 is at least 70%, you meet the alternative test and you qualify to use the

cost sharing method. To see if you qualify for the profit split method, answer the

question on line 18. If line 15 is less than 70%, you do not meet the alternative test.

Part III Start-up Operations (see instructions)

16 If the corporation is engaged in start-up operations, check this box

17 Enter the beginning date of the tax year the possessions corporation began producing the product in

the possession

Part IV Other Information

18 If you are claiming the profit split method: Is the possession product manufactured (as defined in Regulations

section 1.954-3(a)(4)) in the possession? Yes No

If “No,” you do not qualify to use the profit split method of computing taxable income.

Note: Affiliated group members must attach a list showing name, address, and employer identification number of all members of the group.

For Paperwork Reduction Act Notice, see instructions on back. Cat. No. 61166D Form 5712-A (Rev. 12-2003)