Enlarge image

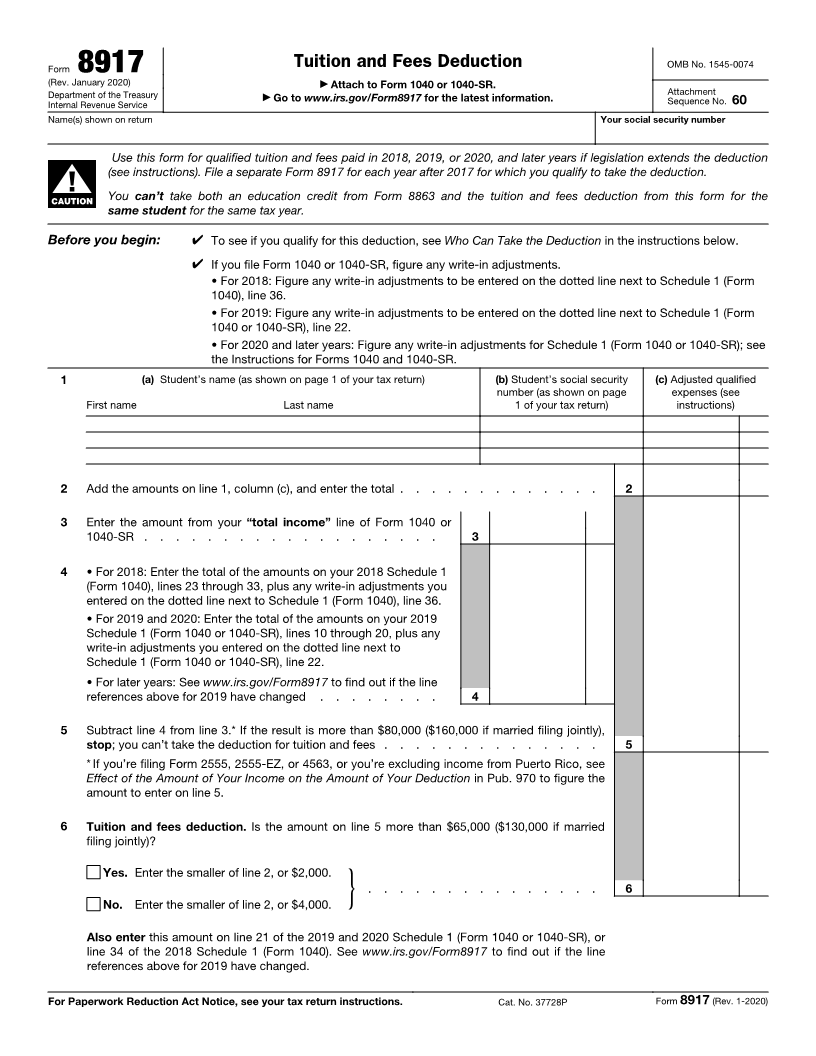

Tuition and Fees Deduction OMB No. 1545-0074

Form 8917

(Rev. January 2020) ▶ Attach to Form 1040 or 1040-SR.

Attachment

Department of the Treasury ▶ Go to www.irs.gov/Form8917 for the latest information. Sequence No. 60

Internal Revenue Service

Name(s) shown on return Your social security number

Use this form for qualified tuition and fees paid in 2018, 2019, or 2020, and later years if legislation extends the deduction

(see instructions). File a separate Form 8917 for each year after 2017 for which you qualify to take the deduction.

▲! You can’t take both an education credit from Form 8863 and the tuition and fees deduction from this form for the

CAUTION

same student for the same tax year.

Before you begin: ✔ To see if you qualify for this deduction, see Who Can Take the Deduction in the instructions below.

✔ If you file Form 1040 or 1040-SR, figure any write-in adjustments.

•For 2018: Figure any write-in adjustments to be entered on the dotted line next to Schedule 1 (Form

1040), line 36.

• For 2019: Figure any write-in adjustments to be entered on the dotted line next to Schedule 1 (Form

1040 or 1040-SR), line 22.

• For 2020 and later years: Figure any write-in adjustments for Schedule 1 (Form 1040 or 1040-SR); see

the Instructions for Forms 1040 and 1040-SR.

1 (a) Student’s name (as shown on page 1 of your tax return) (b) Student’s social security (c) Adjusted qualified

number (as shown on page expenses (see

First name Last name 1 of your tax return) instructions)

2 Add the amounts on line 1, column (c), and enter the total . . . . . . . . . . . . . 2

3 Enter the amount from your “total income” line of Form 1040 or

1040-SR . . . . . . . . . . . . . . . . . . . 3

4 • For 2018: Enter the total of the amounts on your 2018 Schedule 1

(Form 1040), lines 23 through 33, plus any write-in adjustments you

entered on the dotted line next to Schedule 1 (Form 1040), line 36.

• For 2019 and 2020: Enter the total of the amounts on your 2019

Schedule 1 (Form 1040 or 1040-SR), lines 10 through 20, plus any

write-in adjustments you entered on the dotted line next to

Schedule 1 (Form 1040 or 1040-SR), line 22.

• For later years: See www.irs.gov/Form8917 to find out if the line

references above for 2019 have changed . . . . . . . . 4

5 Subtract line 4 from line 3.* If the result is more than $80,000 ($160,000 if married filing jointly),

stop; you can’t take the deduction for tuition and fees . . . . . . . . . . . . . . 5

*If you’re filing Form 2555, 2555-EZ, or 4563, or you’re excluding income from Puerto Rico, see

Effect of the Amount of Your Income on the Amount of Your Deduction in Pub. 970 to figure the

amount to enter on line 5.

6 Tuition and fees deduction. Is the amount on line 5 more than $65,000 ($130,000 if married

filing jointly)?

Yes. Enter the smaller of line 2, or $2,000.

. . . . . . . . . . . . . . . 6

No. Enter the smaller of line 2, or $4,000. }

Also enter this amount on line 21 of the 2019 and 2020 Schedule 1 (Form 1040 or 1040-SR), or

line 34 of the 2018 Schedule 1 (Form 1040). See www.irs.gov/Form8917 to find out if the line

references above for 2019 have changed.

For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 37728P Form 8917 (Rev. 1-2020)