Enlarge image

Userid: CPM Schema: instrx Leadpct: 100% Pt. size: 9 Draft Ok to Print

AH XSL/XML Fileid: … 1116schb/202112/a/xml/cycle06/source (Init. & Date) _______

Page 1 of 3 17:05 - 15-Mar-2022

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Department of the Treasury

Internal Revenue Service

Instructions for Schedule B

(Form 1116)

(December 2021)

Foreign Tax Carryover Reconciliation Schedule

Section references are to the Internal Revenue must file Schedule B for that separate your prior year carryover schedule (that is,

Code unless otherwise noted. category of income. the equivalent of any estimated carryback

amount that you would have entered on

Future Developments Definitions line 7, column (xiii), of Schedule B had that

schedule existed last year) and the actual

For the latest information about Excess limitation. If your foreign tax carryback amount.

developments related to Schedule B credit limitation (Form 1116, Part III,

(Form 1116) and its instructions, such as line 23) exceeds your current year foreign Example. For 2021, Sam has excess

legislation enacted after they were taxes available for credit (the sum of Form foreign taxes of $100 entered on

published, go to IRS.gov/Form1116. 1116, Part III, lines 9, 12, and 13), you Schedule B, line 6, column (xiii). Sam

have an excess limitation. enters $20 on line 7 as the estimated

amount of line 6 to be carried back to

General Instructions Excess foreign taxes. If your current 2020. He enters $80 on line 8 as the

year foreign taxes available for credit (the carryover amount for following years. The

Purpose of Schedule sum of Form 1116, Part III, lines 9, 12, and actual carryback amount to 2020 is later

Schedule B (Form 1116) is used to 13) exceed your foreign tax credit determined to be $15. In 2022, Sam

reconcile your prior year foreign tax limitation (Form 1116, Part III, line 23), you enters $80 on line 1, column (xii), as the

carryover with your current year foreign have excess foreign taxes. carryover from 2021, corresponding to the

tax carryover. Taxpayers are therefore amount entered on line 8, column (xiii), of

reporting running balances of their foreign Specific Instructions Schedule B filed for the 2021 tax year.

tax carryovers showing all activity since Because the estimated carryback amount

the filing of their prior year income tax Important: All information reported on of $20 from 2021 to 2020 (entered on

return. Schedule B must be in English. All line 7 of Schedule B filed for 2021)

amounts must be stated in U.S. dollars. exceeds the actual carryback of $15, Sam

Lines 1 through 3. On these lines, you will enter the $5 excess ($20 − $15) on

figure your adjusted foreign tax carryover Checkboxes at top of page 1. Use a

from the prior tax year which is available separate Schedule B for each applicable line 2a of his 2022 Schedule B as a

for credit in the current tax year. The total category of income and check the positive number. Assuming no other

amount on line 3, column (xiv), is included corresponding box. Check only one box adjustments are needed, the total

on Form 1116, Part III, line 10. for each completed Schedule B. carryover amount from 2021 entered on

line 3, column (xii), of Sam’s 2022

Line 4. If you have a current year excess See Categories of Income in the Schedule B will be $85 ($80 + $5).

limitation (defined later), some or all of the Instructions for Form 1116 for additional

line 3 adjusted foreign tax carryover information regarding separate categories. Line 2b. Adjustments for section

amount will be utilized in the current tax For country codes on lines (h) and (i), see 905(c) redeterminations. Enter on

year. This activity is shown on line 4 of IRS.gov/CountryCodes for the code to line 2b any adjustments needed for

Schedule B. use. section 905(c) redeterminations. See

Foreign Tax Redeterminations in the

Lines 5 through 8. If you have current Note. Don’t complete Schedule B for Instructions for Form 1116 for additional

year excess foreign taxes (defined later), section 951A category income because information.

none of the line 3 adjusted foreign tax the carryover provisions of section 904(c)

carryover amount will be utilized in the don’t apply to foreign taxes assigned to Lines 2c, 2d, 2e, etc. Include on

current tax year. If you have any remaining section 951A category income. these additional lines the following types

carryover from the 10th preceding tax of adjustments needed to reflect:

year, this carryover amount will expire Line 1. Foreign tax carryover from the • Domestic audit adjustments, and

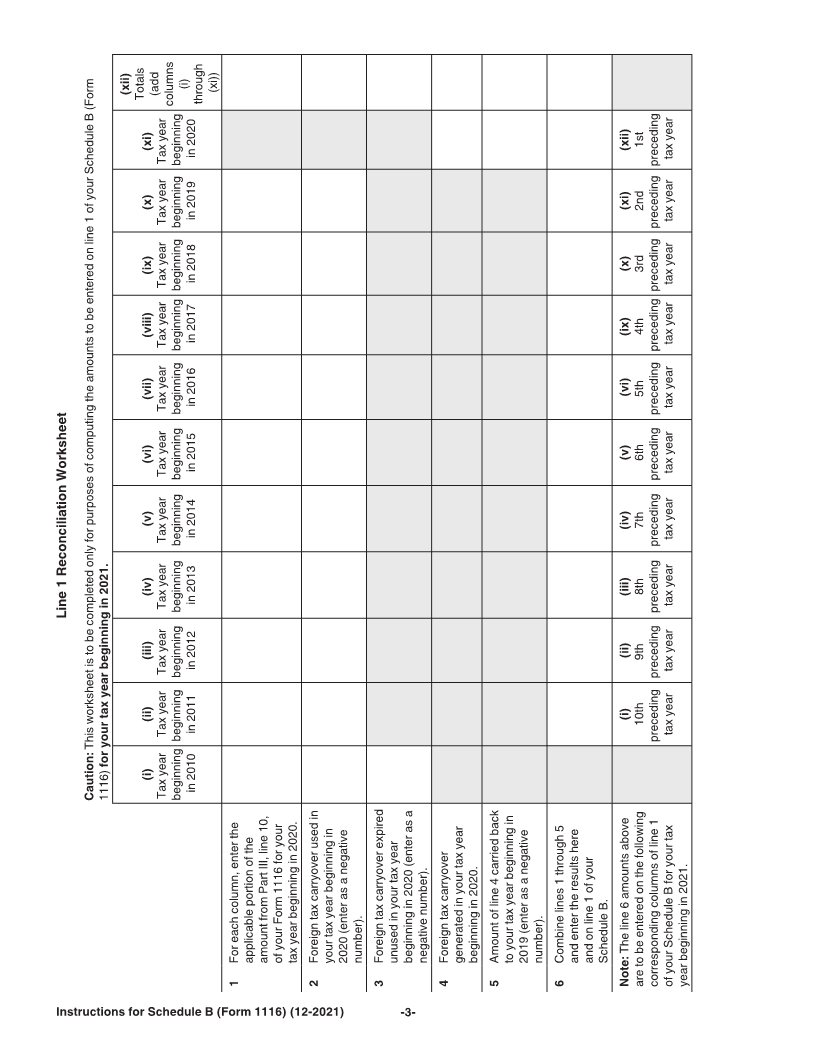

unused. This activity is shown on line 5 of prior tax year. Enter on line 1 the • Any other adjustments needed to

Schedule B. Furthermore, you will amounts from line 6 of the Line 1 properly reflect the total carryover amount

generate a foreign tax carryover in the Reconciliation Worksheet at the end of the from the prior tax year that is available for

current tax year which can be carried back instructions. See the instructions under credit in the current tax year.

to the prior tax year and/or carried forward Line 1 Reconciliation Worksheet, later,

to future tax years (see the line 10 before completing the worksheet. Note. Be sure to enter a brief description

instructions in the Instructions for Form Line 2. Adjustments to line 1. Report of each applicable adjustment item

1116 for details). This activity is shown on on lines 2a, 2b, 2c, 2d, etc., any immediately after the lower case letter in

lines 6 through 8 of Schedule B. adjustments resulting from events that the first column of the schedule.

occurred between the filing of your prior Line 3. Adjusted foreign tax carryover

Who Must File year tax return and the filing of your from prior tax year. Combine lines 1

With respect to each separate category of current year tax return. and 2. The total amount on line 3, column

(xiv), is the adjusted carryover amount

income, if you are filing Form 1116 that Line 2a. Carryback adjustment. from the prior tax year. It is included on

has a foreign tax carryover in the prior tax Enter on line 2a, column (xii), the Form 1116, Part III, line 10 (and, if filing an

year, the current tax year, or both, you difference between any estimated amended return, combined with

carryback amount you may have used on

Mar 15, 2022 Cat. No. 37626c