- 2 -

Enlarge image

|

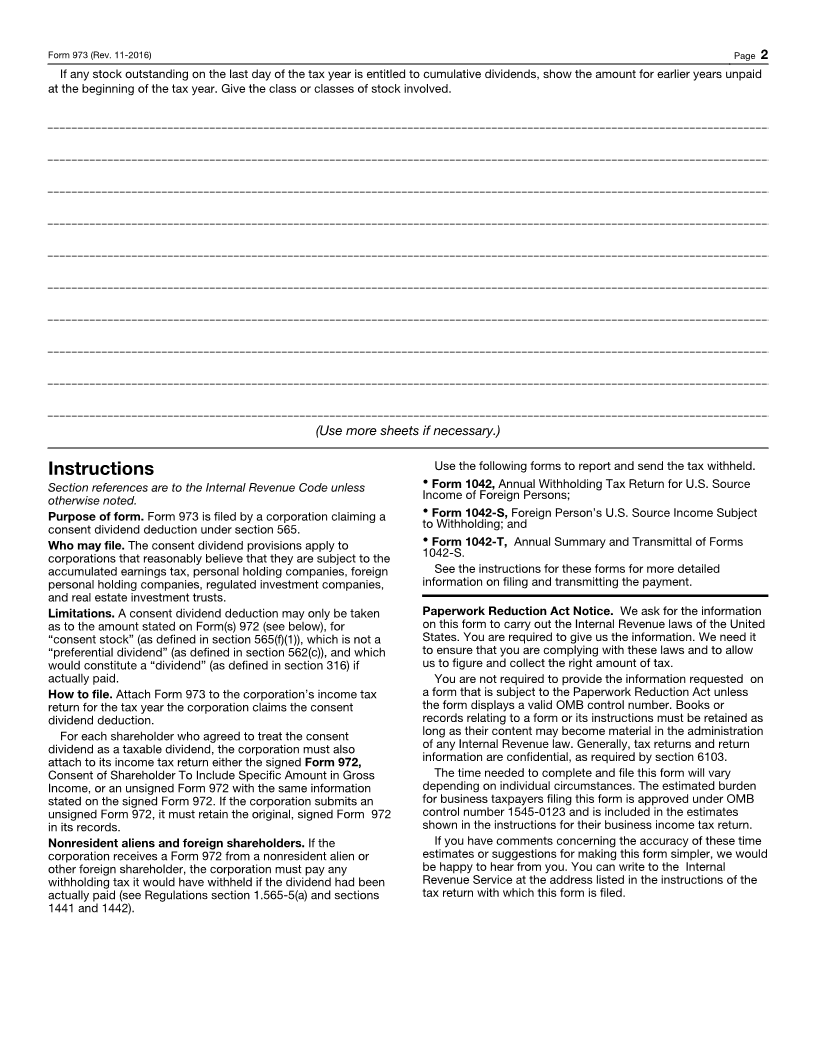

Form 973 (Rev. 11-2016) Page 2

If any stock outstanding on the last day of the tax year is entitled to cumulative dividends, show the amount for earlier years unpaid

at the beginning of the tax year. Give the class or classes of stock involved.

(Use more sheets if necessary.)

Instructions Use the following forms to report and send the tax withheld.

Section references are to the Internal Revenue Code unless • Form 1042, Annual Withholding Tax Return for U.S. Source

otherwise noted. Income of Foreign Persons;

Purpose of form.Form 973 is filed by a corporation claiming a • Form 1042-S, Foreign Person’s U.S. Source Income Subject

consent dividend deduction under section 565. to Withholding; and

Who may file. The consent dividend provisions apply to • Form 1042-T, Annual Summary and Transmittal of Forms

corporations that reasonably believe that they are subject to the 1042-S.

accumulated earnings tax, personal holding companies, foreign See the instructions for these forms for more detailed

personal holding companies, regulated investment companies, information on filing and transmitting the payment.

and real estate investment trusts.

Limitations. A consent dividend deduction may only be taken Paperwork Reduction Act Notice. We ask for the information

as to the amount stated on Form(s) 972 (see below), for on this form to carry out the Internal Revenue laws of the United

“consent stock” (as defined in section 565(f)(1)), which is not a States. You are required to give us the information. We need it

“preferential dividend” (as defined in section 562(c)), and which to ensure that you are complying with these laws and to allow

would constitute a “dividend” (as defined in section 316) if us to figure and collect the right amount of tax.

actually paid. You are not required to provide the information requested on

How to file. Attach Form 973 to the corporation’s income tax a form that is subject to the Paperwork Reduction Act unless

return for the tax year the corporation claims the consent the form displays a valid OMB control number. Books or

dividend deduction. records relating to a form or its instructions must be retained as

For each shareholder who agreed to treat the consent long as their content may become material in the administration

dividend as a taxable dividend, the corporation must also of any Internal Revenue law. Generally, tax returns and return

attach to its income tax return either the signed Form 972, information are confidential, as required by section 6103.

Consent of Shareholder To Include Specific Amount in Gross The time needed to complete and file this form will vary

Income, or an unsigned Form 972 with the same information depending on individual circumstances. The estimated burden

stated on the signed Form 972. If the corporation submits an for business taxpayers filing this form is approved under OMB

unsigned Form 972, it must retain the original, signed Form 972 control number 1545-0123 and is included in the estimates

in its records. shown in the instructions for their business income tax return.

Nonresident aliens and foreign shareholders. If the If you have comments concerning the accuracy of these time

corporation receives a Form 972 from a nonresident alien or estimates or suggestions for making this form simpler, we would

other foreign shareholder, the corporation must pay any be happy to hear from you. You can write to the Internal

withholding tax it would have withheld if the dividend had been Revenue Service at the address listed in the instructions of the

actually paid (see Regulations section 1.565-5(a) and sections tax return with which this form is filed.

1441 and 1442).

|