Enlarge image

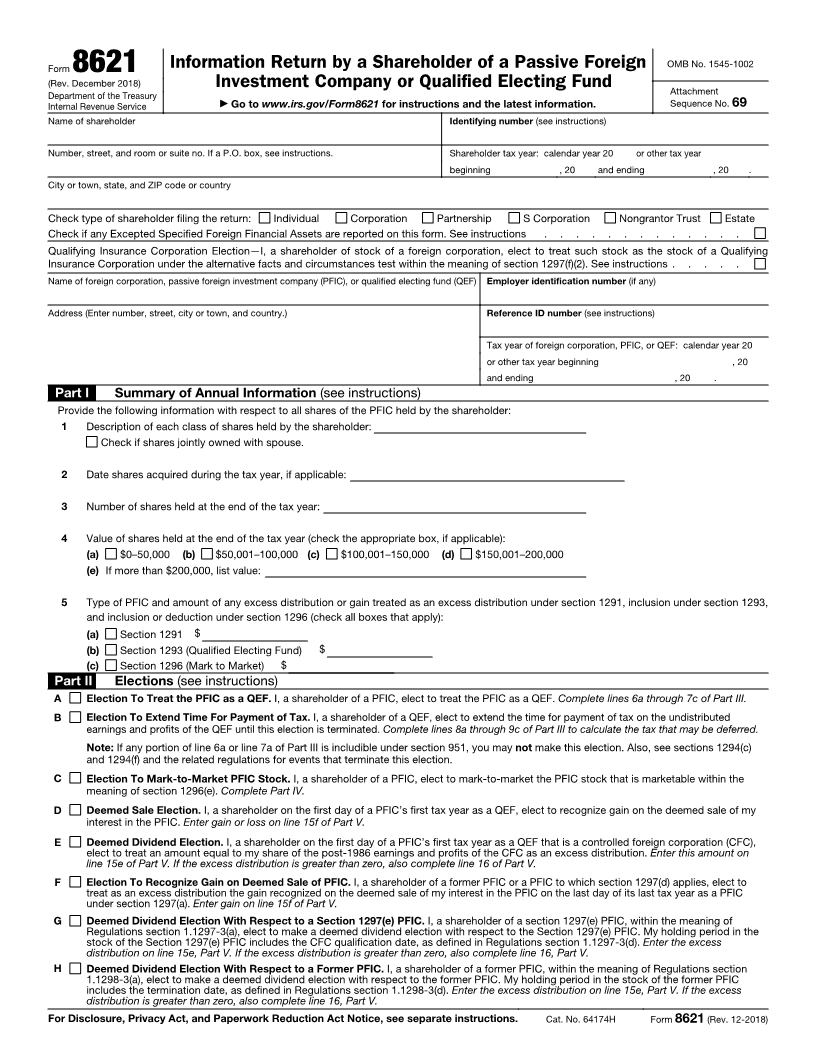

Information Return by a Shareholder of a Passive Foreign OMB No. 1545-1002

Form 8621

(Rev. December 2018) Investment Company or Qualified Electing Fund Attachment

Department of the Treasury ▶ Go to www.irs.gov/Form8621 for instructions and the latest information. Sequence No. 69

Internal Revenue Service

Name of shareholder Identifying number (see instructions)

Number, street, and room or suite no. If a P.O. box, see instructions. Shareholder tax year: calendar year 20 or other tax year

beginning , 20 and ending , 20 .

City or town, state, and ZIP code or country

Check type of shareholder filing the return: Individual Corporation Partnership S Corporation Nongrantor Trust Estate

Check if any Excepted Specified Foreign Financial Assets are reported on this form. See instructions . . . . . . . . . . . . .

Qualifying Insurance Corporation Election I,—a shareholder of stock of a foreign corporation, elect to treat such stock as the stock of a Qualifying

Insurance Corporation under the alternative facts and circumstances test within the meaning of section 1297(f)(2). See instructions . . . . .

Name of foreign corporation, passive foreign investment company (PFIC), or qualified electing fund (QEF) Employer identification number (if any)

Address (Enter number, street, city or town, and country.) Reference ID number (see instructions)

Tax year of foreign corporation, PFIC, or QEF: calendar year 20

or other tax year beginning , 20

and ending , 20 .

Part I Summary of Annual Information (see instructions)

Provide the following information with respect to all shares of the PFIC held by the shareholder:

1 Description of each class of shares held by the shareholder:

Check if shares jointly owned with spouse.

2 Date shares acquired during the tax year, if applicable:

3 Number of shares held at the end of the tax year:

4 Value of shares held at the end of the tax year (check the appropriate box, if applicable):

(a) $0–50,000 (b) $50,001–100,000 (c) $100,001–150,000 (d) $150,001–200,000

(e) If more than $200,000, list value:

5 Type of PFIC and amount of any excess distribution or gain treated as an excess distribution under section 1291, inclusion under section 1293,

and inclusion or deduction under section 1296 (check all boxes that apply):

(a) Section 1291 $

(b) Section 1293 (Qualified Electing Fund) $

(c) Section 1296 (Mark to Market) $

Part II Elections (see instructions)

A Election To Treat the PFIC as a QEF. I, a shareholder of a PFIC, elect to treat the PFIC as a QEF. Complete lines 6a through 7c of Part III.

B Election To Extend Time For Payment of Tax.I, a shareholder of a QEF, elect to extend the time for payment of tax onthe undistributed

earnings and profits of the QEF until this election is terminated. Complete lines 8a through 9c of Part III tocalculate the tax that may be deferred.

Note: If any portion of line 6a or line 7a of Part III is includible under section 951, you may not make this election. Also, see sections 1294(c)

and 1294(f) and the related regulations for events that terminate this election.

C Election To Mark-to-Market PFIC Stock. I, a shareholder of a PFIC, elect to mark-to-market the PFIC stock that ismarketable within the

meaning of section 1296(e). Complete Part IV.

D Deemed Sale Election.I, a shareholder on the first day of a PFIC’s first tax year as a QEF, elect to recognize gain on thedeemed sale of my

interest in the PFIC. Enter gain or loss on line 15f of Part V.

E Deemed Dividend Election. I, a shareholder on the first day of a PFIC’s first tax year as a QEF that is a controlled foreigncorporation (CFC),

elect to treat an amount equal to my share of the post-1986 earnings and profits of the CFC as an excessdistribution. Enter this amount on

line 15e of Part V. If the excess distribution is greater than zero, also complete line 16 of Part V.

F Election To Recognize Gain on Deemed Sale of PFIC. I, a shareholder of a former PFIC or a PFIC to which section 1297(d) applies, elect to

treat as an excess distribution the gain recognized on the deemed sale of my interest in the PFIC on the last day of its last tax year as a PFIC

under section 1297(a). Enter gain on line 15f of Part V.

G Deemed Dividend Election With Respect to a Section 1297(e) PFIC. I, a shareholder of a section 1297(e) PFIC, within the meaning of

Regulations section 1.1297-3(a), elect to make a deemed dividend election with respect to the Section 1297(e) PFIC.My holding period in the

stock of the Section 1297(e) PFIC includes the CFC qualification date, as defined in Regulations section 1.1297-3(d). Enter the excess

distribution on line 15e, Part V. If the excess distribution is greater than zero, also complete line 16, Part V.

H Deemed Dividend Election With Respect to a Former PFIC. I, a shareholder of a former PFIC, within the meaning of Regulations section

1.1298-3(a), elect to make a deemed dividend election with respect to the former PFIC.My holding period in the stock of the former PFIC

includes the termination date, as defined in Regulations section 1.1298-3(d). Enter the excess distribution on line 15e, Part V. If the excess

distribution is greater than zero, also complete line 16, Part V.

For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see separate instructions. Cat. No. 64174H Form 8621 (Rev. 12-2018)