- 7 -

Enlarge image

|

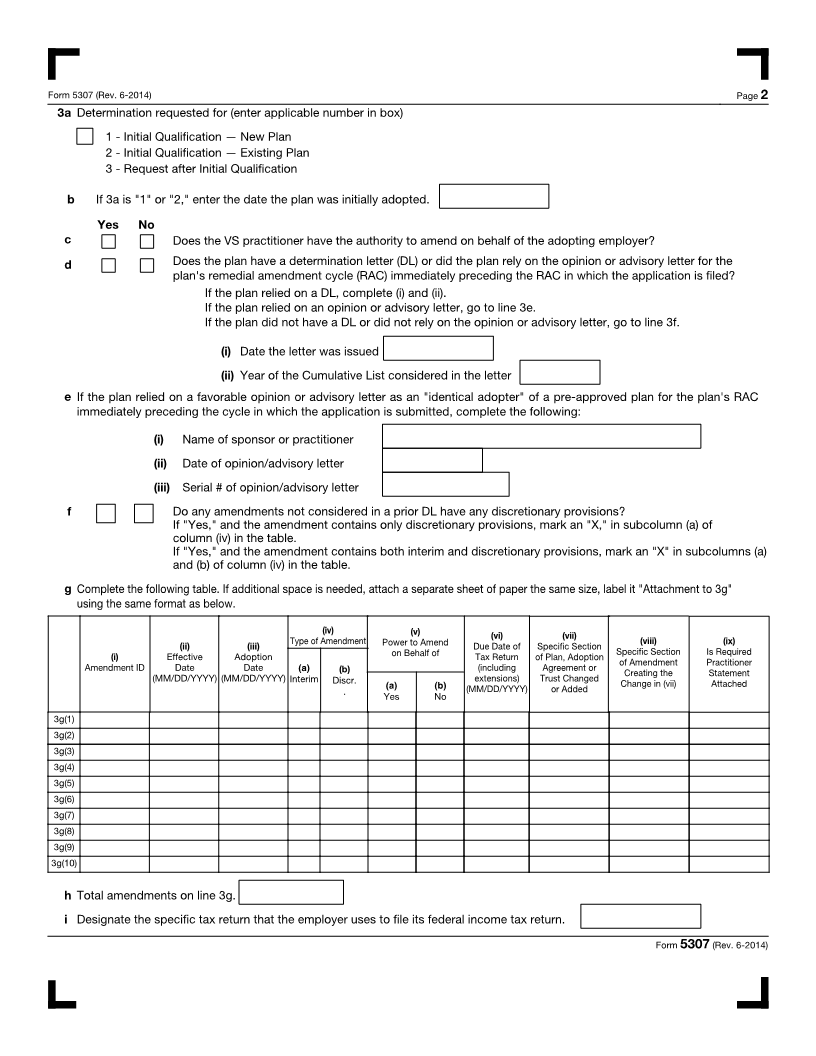

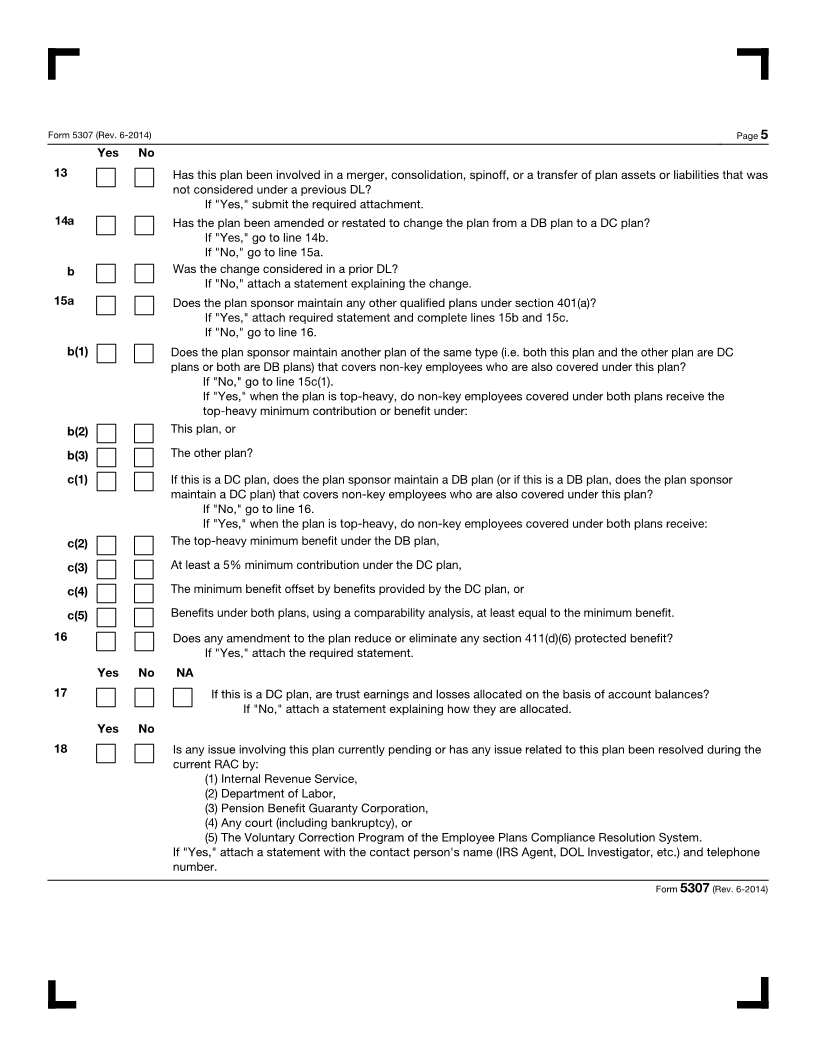

Form 5307 (Rev. 6-2014) Page 5

Yes No

13 Has this plan been involved in a merger, consolidation, spinoff, or a transfer of plan assets or liabilities that was

not considered under a previous DL?

If "Yes," submit the required attachment.

14 a Has the plan been amended or restated to change the plan from a DB plan to a DC plan?

If "Yes," go to line 14b.

If "No," go to line 15a.

b Was the change considered in a prior DL?

If "No," attach a statement explaining the change.

15 a Does the plan sponsor maintain any other qualified plans under section 401(a)?

If "Yes," attach required statement and complete lines 15b and 15c.

If "No," go to line 16.

b(1) Does the plan sponsor maintain another plan of the same type (i.e. both this plan and the other plan are DC

plans or both are DB plans) that covers non-key employees who are also covered under this plan?

If "No," go to line 15c(1).

If "Yes," when the plan is top-heavy, do non-key employees covered under both plans receive the

top-heavy minimum contribution or benefit under:

b(2) This plan, or

b(3) The other plan?

c(1) If this is a DC plan, does the plan sponsor maintain a DB plan (or if this is a DB plan, does the plan sponsor

maintain a DC plan) that covers non-key employees who are also covered under this plan?

If "No," go to line 16.

If "Yes," when the plan is top-heavy, do non-key employees covered under both plans receive:

c(2) The top-heavy minimum benefit under the DB plan,

c(3) At least a 5% minimum contribution under the DC plan,

c(4) The minimum benefit offset by benefits provided by the DC plan, or

c(5) Benefits under both plans, using a comparability analysis, at least equal to the minimum benefit.

16 Does any amendment to the plan reduce or eliminate any section 411(d)(6) protected benefit?

If "Yes," attach the required statement.

Yes No NA

17 If this is a DC plan, are trust earnings and losses allocated on the basis of account balances?

If "No," attach a statement explaining how they are allocated.

Yes No

18 Is any issue involving this plan currently pending or has any issue related to this plan been resolved during the

current RAC by:

(1) Internal Revenue Service,

(2) Department of Labor,

(3) Pension Benefit Guaranty Corporation,

(4) Any court (including bankruptcy), or

(5) The Voluntary Correction Program of the Employee Plans Compliance Resolution System.

If "Yes," attach a statement with the contact person's name (IRS Agent, DOL Investigator, etc.) and telephone

number.

Form 5307 (Rev. 6-2014)

|