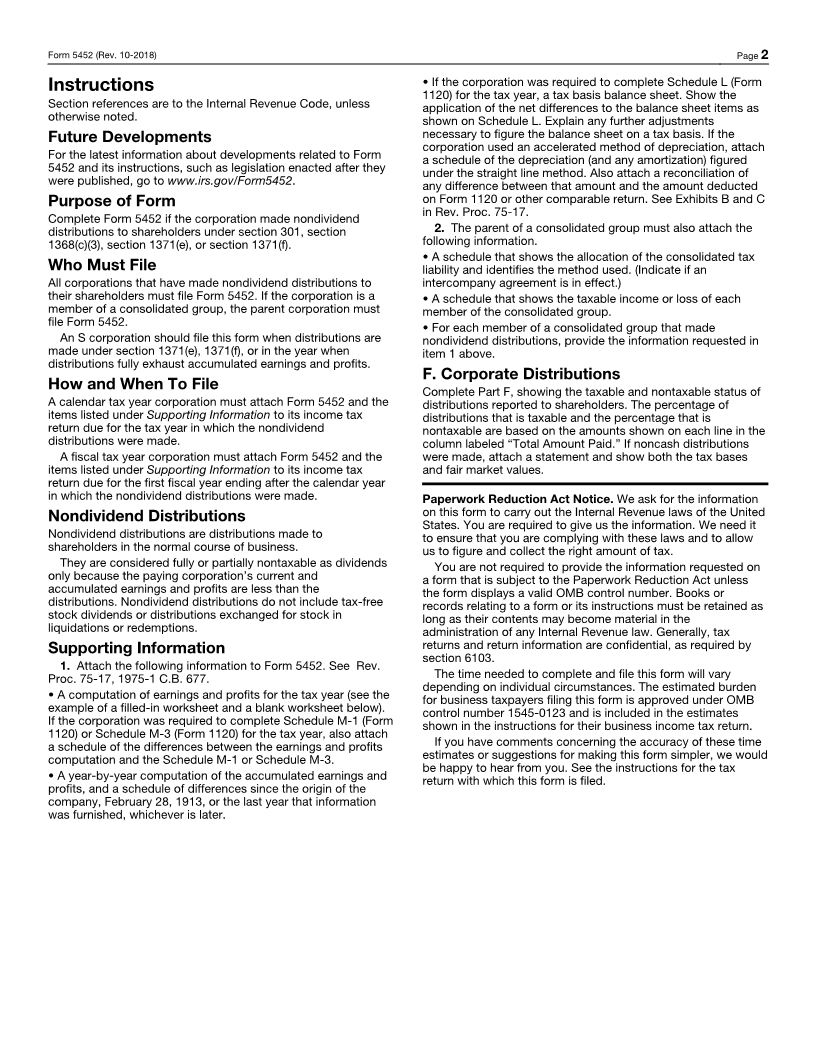

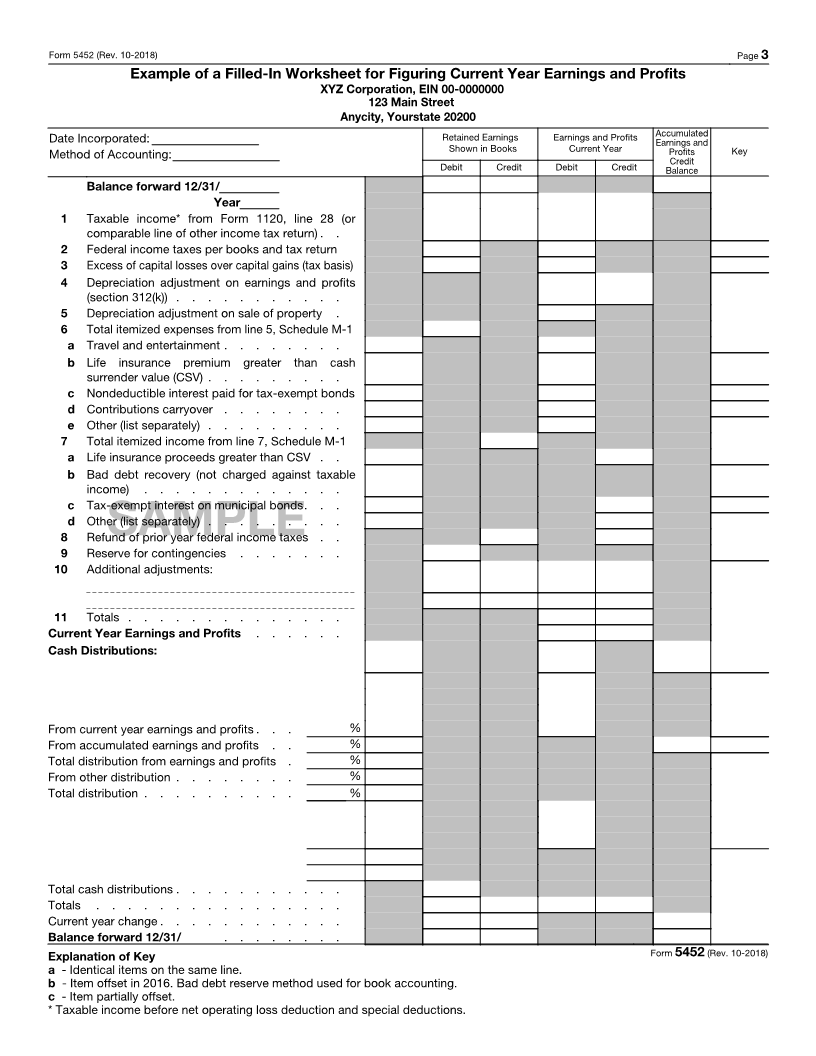

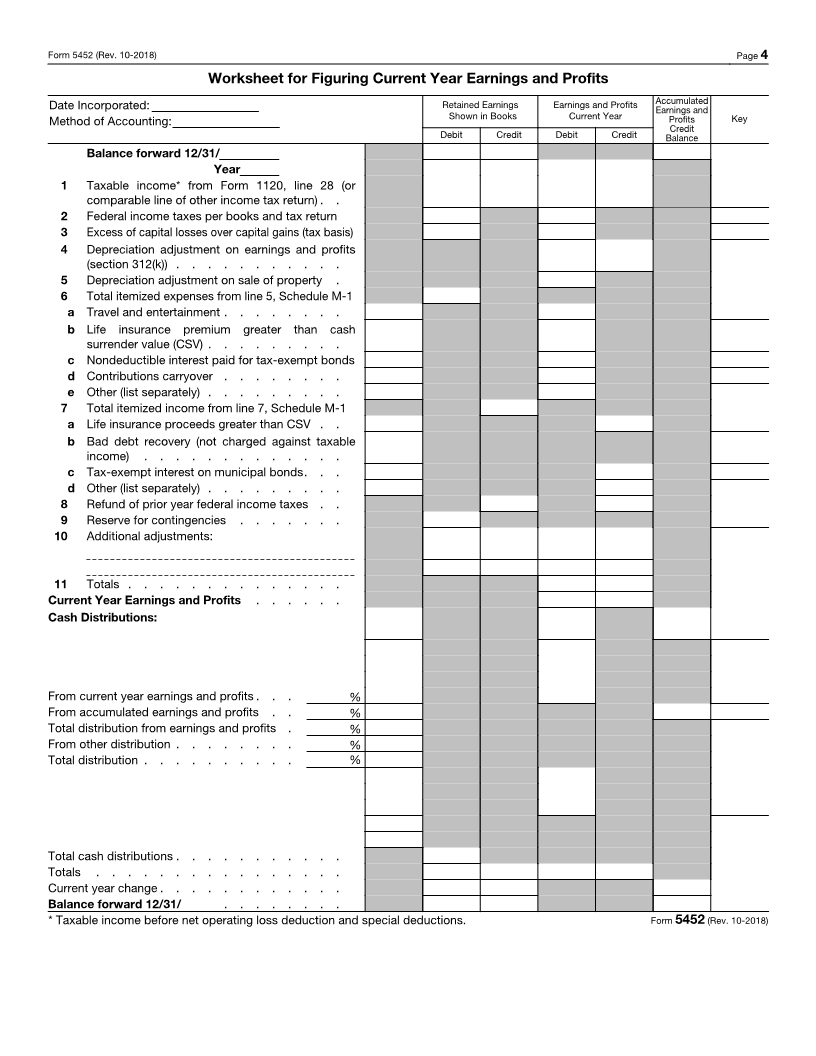

Enlarge image

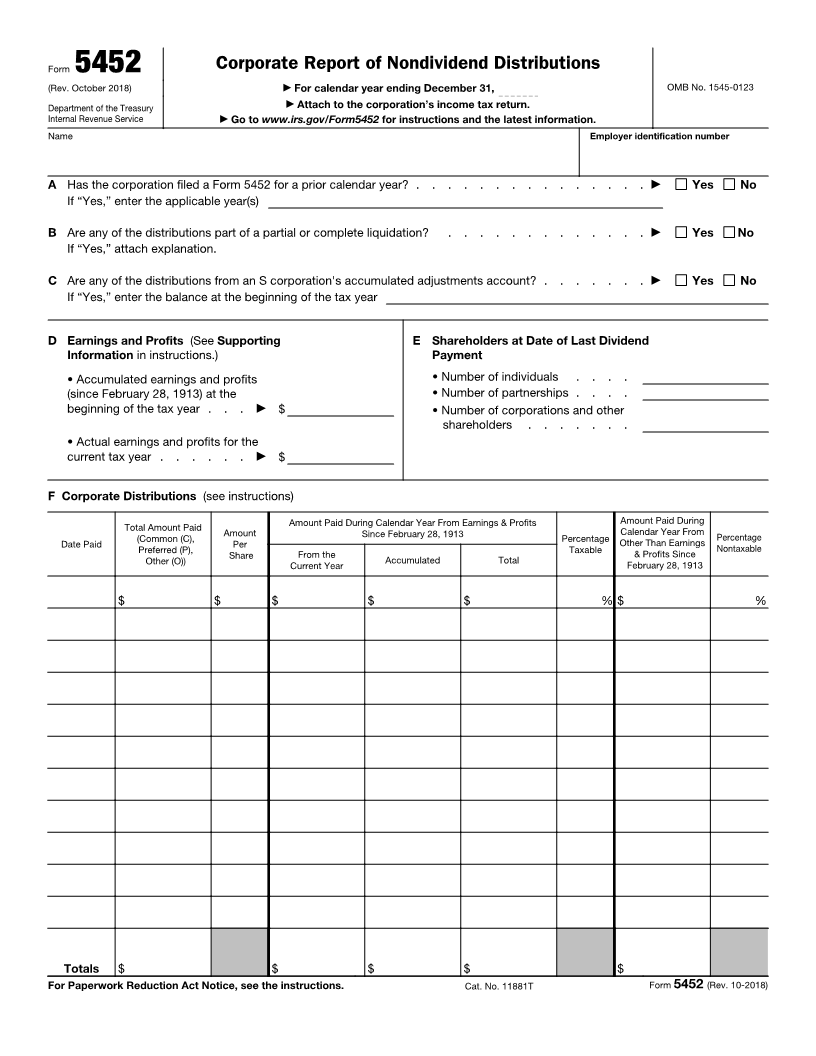

Form 5452 Corporate Report of Nondividend Distributions

(Rev. October 2018) ▶ For calendar year ending December 31, OMB No. 1545-0123

Department of the Treasury ▶ Attach to the corporation’s income tax return.

Internal Revenue Service ▶ Go to www.irs.gov/Form5452 for instructions and the latest information.

Name Employer identification number

A Has the corporation filed a Form 5452 for a prior calendar year? . . . . . . . . . . . . . . . ▶ Yes No

If “Yes,” enter the applicable year(s)

B Are any of the distributions part of a partial or complete liquidation? . . . . . . . . . . . . . ▶ Yes No

If “Yes,” attach explanation.

C Are any of the distributions from an S corporation's accumulated adjustments account? . . . . . . . ▶ Yes No

If “Yes,” enter the balance at the beginning of the tax year

D Earnings and Profits (See Supporting E Shareholders at Date of Last Dividend

Information in instructions.) Payment

• Accumulated earnings and profits • Number of individuals . . . .

(since February 28, 1913) at the • Number of partnerships . . . .

beginning of the tax year . . . ▶ $ • Number of corporations and other

shareholders . . . . . . .

• Actual earnings and profits for the

current tax year . . . . . . ▶ $

F Corporate Distributions (see instructions)

Total Amount Paid Amount Paid During Calendar Year From Earnings & Profits Amount Paid During

Calendar Year From

Date Paid (Common (C), Amount Since February 28, 1913 Percentage Other Than Earnings Percentage

Other (O)) Share

Preferred (P), Per From the Accumulated Total Taxable & Profits Since Nontaxable

Current Year February 28, 1913

$ $ $ $ $ % $ %

Totals $ $ $ $ $

For Paperwork Reduction Act Notice, see the instructions. Cat. No. 11881T Form 5452 (Rev. 10-2018)