Enlarge image

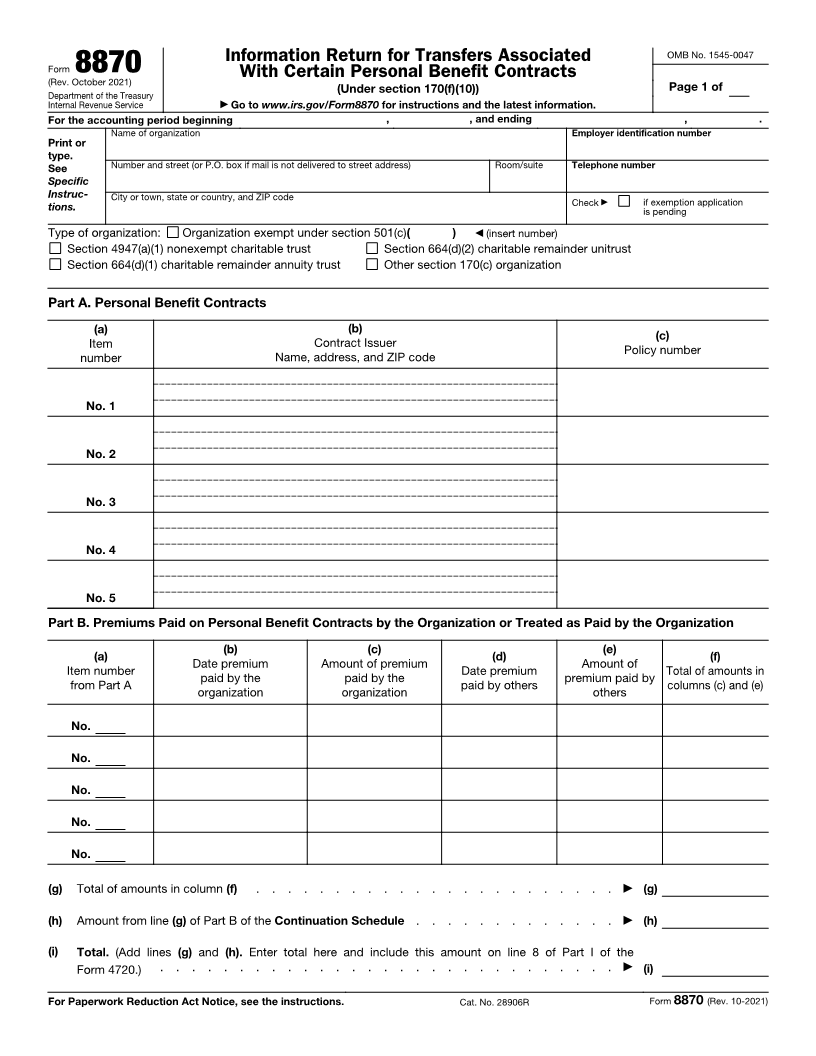

Information Return for Transfers Associated OMB No. 1545-0047

Form 8870 With Certain Personal Benefit Contracts

(Rev. October 2021) Page 1 of

Department of the Treasury (Under section 170(f)(10))

Internal Revenue Service ▶ Go to www.irs.gov/Form8870 for instructions and the latest information.

For the accounting period beginning , , and ending , .

Name of organization Employer identification number

Print or

type.

See Number and street (or P.O. box if mail is not delivered to street address) Room/suite Telephone number

Specific

Instruc- City or town, state or country, and ZIP code Check ▶ if exemption application

tions. is pending

Type of organization: Organization exempt under section 501(c)( ) ◀ (insert number)

Section 4947(a)(1) nonexempt charitable trust Section 664(d)(2) charitable remainder unitrust

Section 664(d)(1) charitable remainder annuity trust Other section 170(c) organization

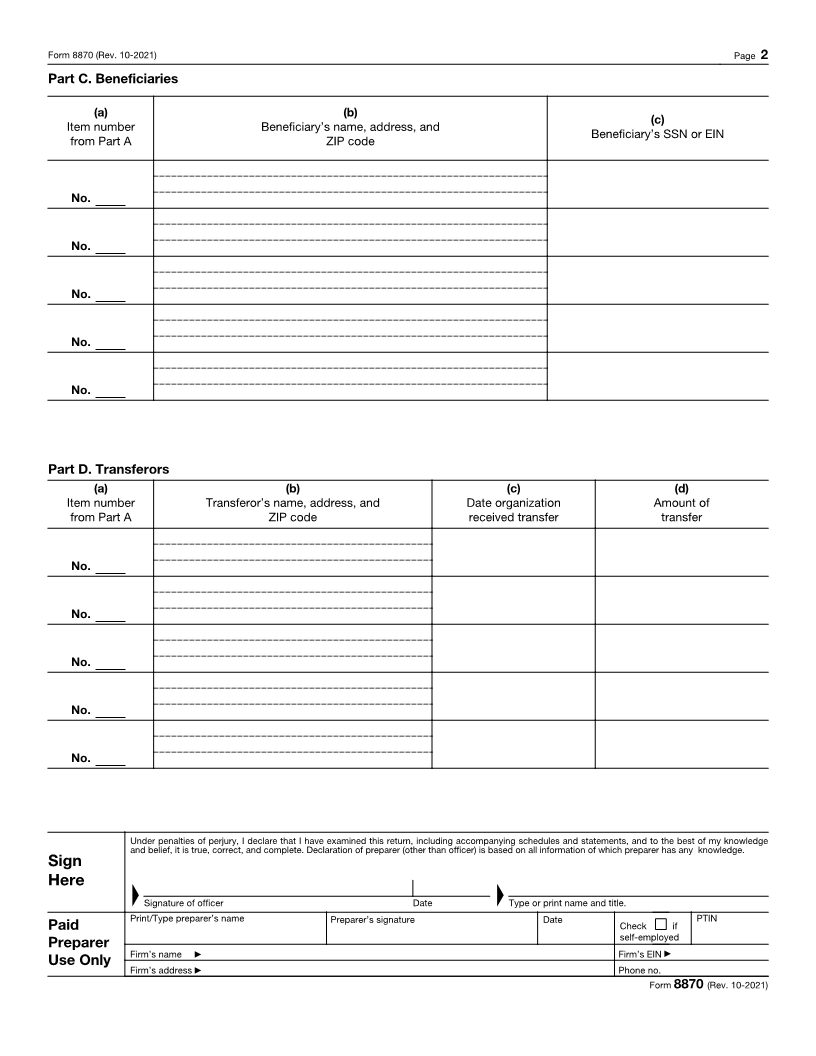

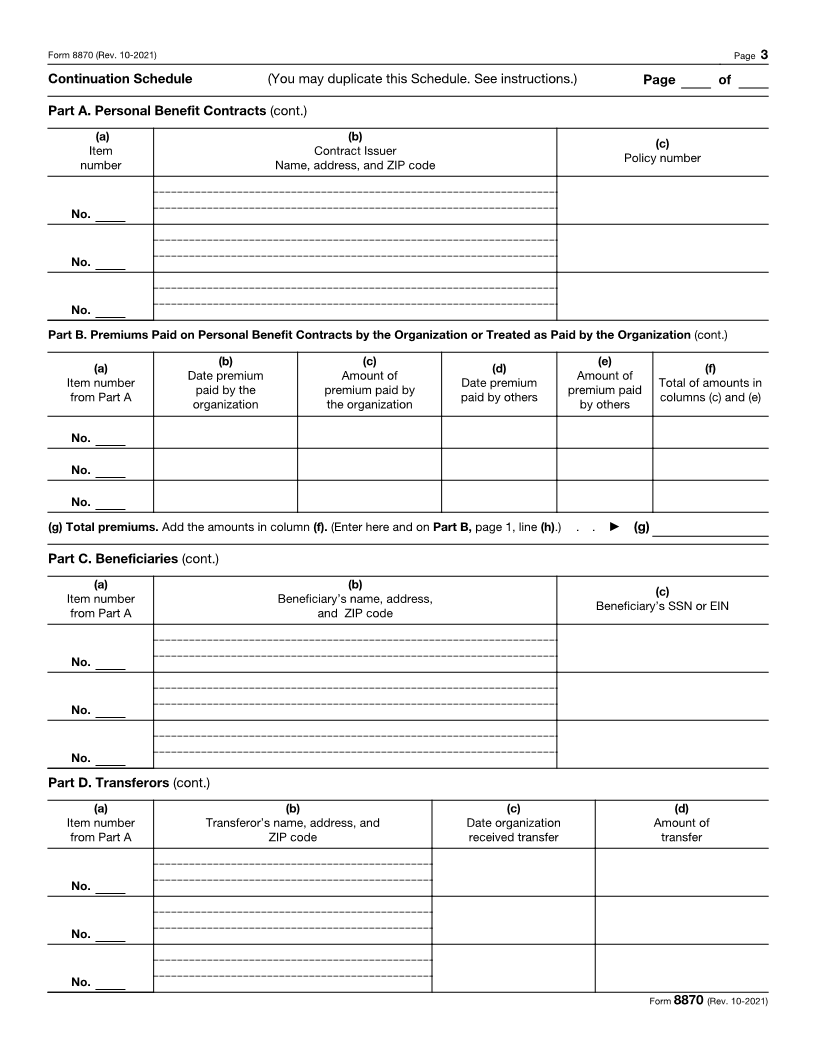

Part A. Personal Benefit Contracts

(a) (b)

(c)

Item Contract Issuer

Policy number

number Name, address, and ZIP code

No. 1

No. 2

No. 3

No. 4

No. 5

Part B. Premiums Paid on Personal Benefit Contracts by the Organization or Treated as Paid by the Organization

(b) (c) (e)

(a) (d) (f)

Date premium Amount of premium Amount of

Item number Date premium Total of amounts in

paid by the paid by the premium paid by

from Part A paid by others columns (c) and (e)

organization organization others

No.

No.

No.

No.

No.

(g) Total of amounts in column (f) . . . . . . . . . . . . . . . . . . . . . . . ▶ (g)

(h) Amount from line (g) of Part B of the Continuation Schedule . . . . . . . . . . . . . ▶ (h)

(i) Total. (Add lines (g) and (h). Enter total here and include this amount on line 8 of Part I of the

Form 4720.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ▶ (i)

For Paperwork Reduction Act Notice, see the instructions. Cat. No. 28906R Form 8870 (Rev. 10-2021)