Enlarge image

STOP: DO NOT USE FOR 2021 HOMESTEAD DECLARATION AND PROPERTY TAX CREDIT FILING This form is for last year’s filing and will not be accepted for tax year 2021 homestead declaration and property tax credit filing.

Enlarge image | STOP: DO NOT USE FOR 2021 HOMESTEAD DECLARATION AND PROPERTY TAX CREDIT FILING This form is for last year’s filing and will not be accepted for tax year 2021 homestead declaration and property tax credit filing. |

Enlarge image |

Be on Guard against Identity Theft and Tax Scams

Identity theft, tax refund fraud, and similar tax scams continue to target taxpayers in Vermont. Taxpayers have

reported emails and phone calls from people posing as employees of the Internal Revenue Service (IRS) and the

Vermont Department of Taxes. Some scammers are clever enough to pose as their victims’ tax preparers to obtain

private information. A common ploy scammers use is to falsely claim taxes are owed and demand immediate Page 1

payment using threats and bullying. Scammers often target the elderly using these tactics.

How to protect yourself from becoming a victim

• Never give out personal information unless you are sure of the identity of the person requesting it.

• If you suspect that an email or phone call is fraudulent, do not engage in conversation. Contact the

Department at 802-828-2865 or 1-866-828-2865 (toll-free) to verify an email or phone call.

How to report fraud

• Report suspected fraud immediately to the Vermont Department of Taxes and the IRS. Information about

how to report fraud is available on the Department website at www.tax.vermont.gov/identity-theft.

• Suspected fraud also should be reported to the Vermont Attorney General’s Consumer Assistance Program

at (800) 649-2424 (toll-free).

Online Options for Filers at www.myVTax.vermont.gov

You can do more online through myVTax. No log-on required!

• File extensions for personal income tax

• File Renter Rebate Claim (Form PR-141/HI-144)

• Complete and submit Landlord Certificate (Form LC-142)

• File the Homestead Declaration and Property Tax Credit (Form HS-122/HI-144)

• View account status and balances

• Set up third party access for your tax preparer

• Respond to correspondence

• Access “Where’s My Refund?” service to view information on your return and refund status

• Check your estimated payments and carryforwards

• Make payments via ACH Debit electronic payments for personal income tax

• File and pay Property Transfer Tax

• Enter into a payment plan

Please note: To e-file your IN-111 and associated schedules, you must use a commercial software vendor.

If you are eligible, you may file for free using one of Vermont’s Free File vendors. For eligibility guidelines,

visit www.tax.vermont.gov/free-file.

2020 Form HS-122 Instructions

www.tax.vermont.gov Page 1 of 10

|

Enlarge image |

Homestead Declaration and Property Tax Credit

FORM HS-122 SECTION A Vermont Homestead Declaration

THE HOMESTEAD DECLARATION must be filed each year by Vermont residents for purposes of the state education tax rate.

The Declaration identifies the property as the homestead of the Vermont resident. A Vermont homestead is taxed Page 2

at the homestead education property tax rate, while a different education property tax rate applies to nonhomestead

property (previously known as the “nonresidential” rate). Nonhomestead property is property used for commercial

purposes or property not used as the principal (primary) residence, such as a second home, camp, or summer cottage.

A property may be classified as both homestead and nonhomestead. This occurs when a part of the home is used

for commercial purposes or as a rental. The property tax bill will show a homestead education property tax rate and

a nonhomestead education property tax rate. For more information on the Homestead Declaration, see 32 V.S.A.

§§ 5401(7), 5410, and Reg. § 1.401(7).

You must file a declaration by April 15, 2020, if you meet all of the following eligibility requirements:

1. Own the Vermont property as your principal residence as of April 1, 2020, AND

2. Expect to physically occupy the Vermont property as your domicile. The declaration must be filed even if it is late.

NOTE: If you meet these requirements, except that your homestead is leased to a tenant on April 1, 2020, you may still

claim it as a homestead if it is not leased for more than 182 days in the calendar year. Other ownership circumstances

include the following:

• When there is more than one owner (joint ownership, only one owner occupant should file.

• Owners with a life estate interest who occupy the dwelling as their principal residence must file.

• Certain trusts may qualify as a homestead. For more information, read Reg. § 1.5401(7) Homestead on

our website. Please note that changes to this regulation are being proposed to conform to amendments made

to this statute.

• An estate holding a residence that was the homestead of the decased person at the time of death may file a

homestead if the residence is not rented.

• When the residence is owned by the estate of the deceased spouse, the widow or widower may file a

homestead declaration as long as it is likely that the residence will pass to the widow or widower when the

estate is settled.

Homestead Declarations filed by April 15, 2020, are considered timely, classified as homesteads on the grand list, and taxed at the

homestead education property tax rate.

Homestead Declarations filed after April 15, 2020, are classified as homesteads but may be assessed the following penalty by the

town:

• Up to 3% if the nonhomestead rate is higher than the homestead education property tax rate.

• Up to 8% if the nonhomestead rate is lower than the homestead education property tax rate.

Homestead Declarations filed after Oct. 15, 2020, will be classified as nonhomestead. The owner will be charged the higher of the

two rates, assessed a penalty, and must pay any additional property tax and interest due.

What if you SELL your property before April 1, 2020? If you filed a Homestead Declaration and Property Tax Credit Claim before

April 1, 2020, you must withdraw the declaration and claim using Form HS-122W, available on our website.

What if you rent your homestead on April 1 and occupy it yourself for fewer than 183 days in the calendar year? You must

withdraw the declaration using Form HS-122W, Vermont Homestead Declaration and/or Property Tax Credit

Withdrawal. Form HS-122W is available on our website. If you occupy your home fewer than 183 days, you are

disqualified from filing both the Homestead Declaration and the Property Tax Credit Claim.

Claimant Information: Enter your Social Security Number, name, and mailing address. If applicable, enter the Social Security

Number and name of your spouse/civil union partner. Enter your date of birth. Example: March 27, 1948, is entered

as 03 27 1948

SPAN (School Property Account Number): This is a unique 11-digit identification number assigned by the town or city and is

printed on the property tax bill. It is very important to verify your SPAN. The property tax credit is credited to the

property tax bill for this SPAN.

Location of Homestead: Enter the physical location (street, road name) Please do not enter a post office box or write “same,” “see

above,” or the city/town name. Examples: 123 Maple Street or 276 Route 12A

Legal Residence: Enter the town or city name of your legal residence as of April 1, 2020. If there is both a city and town with the same

name, please specify. Examples: Barre City or Barre Town, St. Albans City or St. Albans Town

Federal Filing Status: Enter the corresponding letter of the filing status used on your 2019 federal income tax return. If you are not

required to file a federal income tax return, leave the box blank.

2020 Form HS-122 Instructions

www.tax.vermont.gov Page 2 of 10

|

Enlarge image |

Line A1 Business Use of Dwelling: Enter percentage of the dwelling used for business. Leave blank if there is no business

use or the business use is 25% or less.

Line A2 Rental Use of Dwelling: Enter the percentage of the dwelling that is rented. All rental use is required to be reported

even if it is 25% or under.

Line A3 Business or Rental Use of Improvements and Other Buildings on the Property Check the applicable “Yes” or

“No” box. Check the “Yes” box if any improvements or other buildings are rented out or used for business. Page 3

Lines A4-A7 Special Situations: Check situation applicable.

FORM HS-122 SECTION B Property Tax Credit Claim

To be eligible for a Property Tax Credit, you must meet all of the following eligibility requirements:

1. The property must be declared as your homestead.

2. You were domiciled in Vermont for the entire 2019 calendar year.

3. You own the property as your principal residence on April 1, 2020.

4. You were not claimed as a dependent of another taxpayer for the 2019 tax year.

5. You meet the household income criteria of $138,250 or less.

Due Date - April 15, 2020

Claims for Property Tax Credits filed between April 15 and Oct. 15, 2020, will have a $15 late filing fee deducted

from the property tax credit.

2020 Property Tax Credits filed after Oct. 15, 2020, cannot be accepted.

Incomplete claims cannot be processed and are not considered filed.

Receipt Date Forms mailed through the U.S. Post Office are considered timely if received by the Vermont Department of Taxes

within three business days of the due date. If you file electronically, the receipt date is the transmission date. If you

bring the form to the Department in person, it must be on or before the due date.

HOMEOWNER DECEASED before April 1, 2020? The right to file for a Property Tax Credit ends if the homeowner dies before

April 1, 2020. If a single homeowner has filed a claim before April 1 but then dies before April 1, the claim must be

withdrawn using Form HS-122W. If, however, two homeowners have filed jointly before April 1, but then one of

them dies before April 1, the claim belongs to the surviving homeowner.

PURCHASED a home as your principal residence on or before April 1, 2020? You must file Form HS-122 Sections A and B to

make a property tax credit claim. You can file online on our website at www.myVTax.vermont.gov.

Amending Form HS-122 An error on the 2020 Form HS-122 may be corrected up to Oct. 15, 2020. After that date, only household

income may be amended.

INJURED SPOUSE CLAIMS: To make an “injured spouse” claim, send the following information prior to filing your claim:

1. Copy of federal Form 8379, Injured Spouse Allocation (if you filed this form with the IRS)

2. A signed letter of request for your claim

3. Documentation of your ownership interest, for example, your deed

Mail information to:

ATTN: Injured Spouse Unit

Vermont Department of Taxes

PO Box 1645

Montpelier VT 05601-1645

The Department will notify you if the property tax credit is taken to pay a bill. You have 30 days from the date on

the notice to submit the injured spouse claim to the Department.

Before you begin to file for the Property Tax Credit, you must first determine if you meet household income criteria. Complete

Schedule HI-144, Household Income, to see if you are eligible for a credit.

Schedule HI-144 must be submitted with Form HS-122. See instructions for Line B9 and B10, Mobile Home Lot Rent; Lines B11

and B12, Allocated Property Tax from Land Trust, Cooperative, or Nonprofit Mobile Home Park; and Lines B13

and B14, the education and municipal tax on a property whose housesite value is less than 2 acres and crosses town

boundaries. We may require additional documents.

Line A3 SPAN - Required: Be sure to use the correct School Parcel Account Number (SPAN) for your property. Entering

an incorrect SPAN may delay your Property Tax Credit. You will find the 11-digit number on your property tax bill.

It appears as XXX-XXX-XXXXX. If in doubt, contact your town clerk.

Lines B1 – B3 Eligibility Questions: Check the appropriate “Yes” or “No” box to answer the eligibility questions. ALL eligibility

questions must be answered.

2020 Form HS-122 Instructions

www.tax.vermont.gov Page 3 of 10

|

Enlarge image |

Information for Lines B4-B6 is found on your 2019/2020 property tax bill.

Line B4 Housesite Value: Enter the assessed housesite value shown on the 2019/2020 property tax bill. See the instructions

under “Special Situations” for information on new construction or purchase of a new home.

Line B5 Housesite Education PropertyTax: Enter the education property tax shown on the 2019/2020 property tax bill.

Line B6 Housesite Municipal Tax: Enter the municipal property tax shown on the 2019/2020 property tax bill. Page 4

Line B7 Ownership Interest: Any person who meets eligibility requirements to file a Homestead Declaration should be

included in the ownership interest. For example, if all owners are members of the household, occupying the property

as their principal residence, enter 100%. If some owners are not members of the household, meaning they do not

occupy the property as their principal residence, then ownership interest is the percentage of ownership for household

members only. For example, if there are four owners but only two of them occupy the property as their principal

residence, enter 50%.

Line B8 Household Income: Enter the amount calculated on Schedule HI-144, Line z. If you are amending your Household

Income Schedule, please mark the box with an “X.”

Line B9 E-file Certificate Number from Form LC-142: If applicable, enter the E-file Certificate Number located on

the Form LC-142 that you receive from your landlord. If the Form LC-142 you received does not have an E-file

Certificate Number, leave this line blank.

Line B10 Lot Rent for a Mobile Home: If you rent a lot in a privately owned mobile home park, obtain Form LC-142,

Landlord Certificate, from your landlord and enter the amount of Allocable Rent.

Lines B11 – B12 Allocated Tax from Land Trust, Cooperative, or Nonprofit Mobile Home Park: Enter the amount of education

and municipal property tax shown on the statement issued to you by the land trust, cooperative, or nonprofit mobile

home park.

Lines B13 – B14 Property Tax from Contiguous Property: If you own contiguous property, you may use the property taxes from

that parcel if the property tax bill for your dwelling has under two acres or part of the dwelling or a building, such as

a garage, is on the contiguous property.

Signature: Sign the property tax credit claim.

Date: Enter the date you sign the claim.

Disclosure Authorization: Check this box if you wish to give the Vermont Department of Taxes authorization to discuss this claim

with your tax preparer. Be sure the tax preparer’s name is included. This authorization will automatically end

April 15, 2025.

Preparer: If you are a paid preparer, you must sign this claim, enter your Social Security Number or PTIN, and if employed by a

business, include the Federal Employer Identification Number of the business. If someone other than the homeowner

prepared this claim without charging a fee, the preparer’s signature is optional.

If mailing this return, send to:

Vermont Department of Taxes

PO Box 1881

Montpelier, VT 05601-1881

The maximum 2020 Property Tax Credit is $8,000.

The Property Tax Credit will appear as a state payment on your 2020/2021 property tax bill.

SCHEDULE HI-144 Household Income Schedule

Domicile For a definition of “domicile,” please refer to Reg. § 1.5811(11)(A)(i)-Domicile on our website.

Homeowner You are the homeowner if you own and occupy the housesite as your principal residence.

Household Income means modified Adjusted Gross Income, but not less than zero (0), received in a calendar year by all persons of

a household while members of that household.

Household Members include you, your spouse/civil union partner, roommates, and family members (including children) even if they

file their own income tax returns and are not considered dependents. You must include a spouse/civil union partner

as a member of your household even if your spouse/civil union partner does not live with you in the same home. If,

however, your spouse/civil union partner does not live with you and you and your spouse/civil union partner are

legally separated by court order, then this person is not considered a household member.

2020 Form HS-122 Instructions

www.tax.vermont.gov Page 4 of 10

|

Enlarge image |

Exceptions - The following are not considered household members:

• A spouse/civil union partner who is at least 62 years of age and who has moved to a nursing home or other

care facility with no reasonable prospect of returning to the household

• A person who is not related to any member of the household and who is living in the household under

a written home sharing agreement with a nonprofit home sharing program authorized by the Vermont

Department of Disabilities, Aging and Independent Living

Page 5

• A person living in the household who is a bona fide employee hired to provide personal care to a member of

the household and who is not related to the person for whom the care is provided

• A person who resides with you (the person filing the claim) for the primary reason of providing attendant

care services or homemaker or companionship services with or without compensation that allows you to

remain in your home or avoid institutionalization. To qualify for this exception, you must be disabled or 62

years of age or older as of Dec. 31, 2019.

Members of the household for a portion of the year. You must include the income received by all persons residing in the home or

apartment during the period they resided in the home or apartment.

Household Income On Schedule HI-144, Lines a through n, list the items of income that are required to be reported for Household

Income.

• Report your income (if filing jointly, include the income of your spouse) under Column 1.

• Report the income of your spouse or civil union partner if filing separately, under Column 2.

Exceptions applying to spouse/civil union partner

1. You do not have to include your spouse/civil union partner when the person is not living with you

as a member of your household and you are legally separated by court order or previously

established protective/restraining order.

2. You do not have to include the income of a spouse who is age 62 or older and has moved permanently

to a nursing home or other care facility.

• You do not have to include the income of a spouse who has a court-ordered restraining order in place

prohibiting contact with you.

• Report the income of your spouse if filing separately, or civil union partner under Column 2.

Exclusions: The following are not part of household income:

• Payments by the State of Vermont for foster care under Vermont law at 33 V.S.A. Chapters 49 and 55

• Payments by the State of Vermont to a family for the support of an eligible person with a developmental

disability

• Payments by the State of Vermont or an agency for adult foster care payments (formerly “difficulty of care”

payments) found in 18 V.S.A. § 8907

• Surplus food or other relief in-kind supplied by a government agency

• The first $6,500 of income received (earned or unearned) by a person who qualifies as a dependent of the

claimant under the Internal Revenue Code and who is the claimant’s parent or disabled adult child

• The first $6,500 of income earned, such as wages, salaries, tips, etc., by a full-time student who qualifies as

a dependent of the claimant (all unearned income must be reported)

• The first $6,500 of gifts of cash and/or cash equivalents received by all household members

• Distributions from the contributions to a ROTH IRA (distributions from the earnings of the ROTH IRA are

to be reported in household income)

• Gifts from a nongovernmental source, such as aid provided by the Red Cross, Salvation Army, a church, to

assist paying a living expense (for example, fuel, utilities, rent)

• Any income that resulted from cancellation of debt. Refer to 32 V.S.A. § 6061(4)(B)

Household Income

Line a Cash public assistance and relief Enter all payments from the State of Vermont Agency of Human Services except

for foster care payments, difficulty of care payments, food stamps, and fuel assistance. The first $6,500 of refugee

settlement payment is excluded.

Line b Social Security, Social Security Income (SSI), Social Security Disability Income (SSDI), railroad retirement,

and veterans’ benefits (taxable and nontaxable) Enter payments from Social Security as reported in Box 5 of your

SSA-1099 (this box adjusts for any repayment of Social Security benefits you were required to make) or from federal

Form 1040, U.S. Individual Income Tax Return. Social Security benefits also include SSI and SSDI payments. Enter

all railroad retirement from RRB-1099 and veteran’s benefits.

Line c Unemployment compensation and workers’ compensation Enter the full unemployment compensation shown on

Form 1099-G, Certain Government Payments, plus any workers’ compensation you received.

Line d Wages, salaries, tips, etc. Enter the income shown in Box 1 of the W-2. Also report Form 1099-MISC, Miscellaneous

Income, issued for nonemployee compensation if this is income not included as part of Line i, Business Income. See

exclusions in Household Income section before completing this line.

2020 Form HS-122 Instructions

www.tax.vermont.gov Page 5 of 10

|

Enlarge image |

Line e Interest and dividends Enter the income reported on federal Form 1040, Lines 2b and 3b.

Line f Interest on U.S., state, or municipal obligations Enter the income reported on federal Form 1040, Line 2a, and all

interest income from federal, state or municipal government bonds. This includes interest taxed at the federal level

but exempted for Vermont income tax purposes and interest not taxed at the federal level.

Line g Alimony, support money Enter the total received for alimony and support money. Support money includes payment

of housing expenses for household member or other financial assistance that makes it possible for the household Page 6

member to live in the homestead or rental unit.

Line h Child support and cash gifts List all child support payments received in the calendar year as well as all cash gifts.

Cash gifts include any and all cash received by you or other household members, as well as cash equivalents. Cash

equivalents include gifted stocks, bonds, treasury obligations, certificates of deposit or other household instruments

convertible to cash.

Specify the type of income you are reporting on the indicated line.

Line i Business income Enter income attributable to a business. If there is a business loss, leave blank. For taxpayers

filing Married Filing Jointly, where both spouses have business income or loss from sole proprietorships, enter the

amount from federal Form 1040 or leave blank if a negative, in the Claimant column.

Line j Capital gains Report nontaxable gains from the sale of your home and gains from federal Schedule D, Capital

Gains and Losses: A capital loss carryforward cannot be used to offset a current year capital gain. Add back federal

Schedule D, Lines 6 and 14 to Line 16. This cannot be less than zero (0).

Exception: A business loss may offset a capital gain on the sale of the business’s property provided all three of the

following are true for the business: (1) the loss and capital gain are for the same business; (2) the IRS requires the

capital gain to be reported; and (3) the business loss and capital gain from the sale of the business’s property both

occurred in the 2019 tax year. If the offset of the capital gain by the loss creates a negative amount, leave blank. A

capital loss cannot offset business income.

Line k Taxable pensions, annuities, IRAs, and retirement fund distributions. Enter the income from retirement,

deferred compensation plans, and annuities as reported on federal Form 1040. Household income includes non-

qualified distributions from retirement and deferred compensation plans and both taxable and nontaxable federal

pension and annuity benefits.

Line l Rental and Royalty income Enter the income from each rental property you own as reported on federal

Schedule E, Supplemental Income and Loss, Part I. Each rental property stands on its own. A loss generated by

one property may not be used to reduce income from a different property. Refer to Technical Bulletin TB-56,

Reporting Business Income, K-1 Income, Rental Income and Capital Gain on Schedule HI-144 Household income,

on our website for the proper treatment of rental income and losses. Room and board payments received as difficulty

of care payments for a member of your household are rental income and must be reported on this line. Report royalty

income from federal Form 1099-MISC, Miscellaneous Income, 1099-S, Proceeds from Real Estate Transactions;

Schedule K-1, Share of Income Deductions, Credits, etc.; or federal Schedule E, Supplemental Income and Loss,

Part I.

Line m Income from Partnerships, S Corporations, LLCs, Farms, Trusts and Estates Federal Schedule K-1 pass-

through income as required to be reported on federal Schedules E and/or F, Profit or Loss from Farming. Report

ordinary business income, rental income and guaranteed payments from K-1 on this line. The loss from one K-1

cannot offset income from another K-1. A loss is reported as -0-. See Line j instructions for the only provision

allowing netting of a business loss.

Line n Other income Sources of other income include, but are not limited to, prizes and awards, gambling or lottery

winnings, director’s fees, employer allowances, taxable refunds from federal Form 1040, allowances received by

dependents of armed service personnel and military subsistence payments (Basic Allowance for Housing, flexible

spending arrangement or account), loss of time insurance, cost of living adjustment paid to federal employees, and

other gains from federal Form 1040. Report on this line income reported to you on federal Form 1099-MISC or

W-2G, Certain Gambling Winnings. For more information on military income, see the “Vermont Tax Guide for

Military and National Services” available on the Department’s website.

Line o Add items a through n by column. Carry those amounts over to the top of the next page.

Adjustments to Income:

The following adjustments to household income may be made for each member of the household.

Line p Social Security and Medicare Tax Withheld and Self-Employment Tax on Income Reported Social Security

and Medicare payroll tax payments are deducted from household income, but only to the extent that the salary and

wages are included in household income. Please see the examples that follow:

1. Deferred compensation – If you made a deferred compensation contribution for the tax year, the amount

of the contribution is not included in the federal Adjusted Gross Income as stated in Box 1 on your Form

W-2, Wage and Tax Statement. The Social Security and Medicare taxes on the W-2 must be reduced for

2020 Form HS-122 Instructions

www.tax.vermont.gov Page 6 of 10

|

Enlarge image |

the purposes of reporting household income on the HI-144. Generally, this amount is 7.65% of the amount

stated in Box 1 on the W-2.

2. Military pay – Multiplying the amount stated in Box 1 on the W-2 by 7.65% provides the correct value for

this deduction.

3. Allocated tips – In addition to the figures included on the W-2, add the Social Security and Medicare

payments you made as the result of completing federal Form 4137, Social Security and Medicare Tax On

Page 7

Unreported Tip Income.

Self-Employed Social Security and Medicare Taxes Paid Self-employed claimants may subtract from household

income the amount from federal Schedule SE, Self-Employment Tax, Section A, Line 5, or Section B, Line 12,

that represents the Social Security and Medicare taxes paid for 2018 for income reported on Schedule HI-144. For

income not required to be reported upon which Social Security and Medicare taxes were paid, multiply the income

not reported on HI-144 by 15.3% and subtract the result from the federal Schedule SE amount. The amount of Social

Security and Medicare taxes reported on this line includes the allowable deduction for one-half self-employment tax

on federal Form 1040, Line 27. You may be asked for a copy of your federal Schedule SE.

Line q Child support paid Report only those payments for which receipts or other evidence of payment is available. This

evidence may include cancelled checks or a statement from the Office of Child Support in addition to the name and

Social Security Number of the parent receiving the payment.

Line r Allowable Adjustments from federal Schedule 1. The following expenses may be subtracted from income.

r1. Certain business expenses of reservists

r2. Alimony paid

r3. Self-employed health insurance deduction

r4. Health savings account deduction

r5. Tuition and Fees as federally allowed

Line s Add Lines p, q, and the total of Lines r1 to r5 for each column.

Line t Subtract the total adjustments on Line s from the total income on Line o for each column. The adjustments for

any individual in your household cannot exceed the income of that individual. If Line o minus Line s is negative,

enter -0-.

Line u Add columns 1, 2, and 3 and enter sum. Entry cannot be less than zero (0).

Line v For claimants under the age of 65 as of Dec. 31, 2019, enter the total interest and dividends for all household

members reported on Lines e and f in each column.

Line w Add the three columns on Line v.

Line x For purposes of calculating the Property Tax Credit or Renter Rebate Claim, household income is increased by the

household total of interest and dividend income greater than $10,000. Refer to V.S.A. § 6061(e).

Line y Subtract Line x from Line w. If Line x is more than Line w, enter -0-.

Line z Household Income. Add Line u and Line y. Enter this figure on Form HS-122 or Form PR-141.

SPECIAL SITUATIONS

Deceased Homeowner

Property Tax Credit: An estate cannot make a Property Tax Credit Claim on behalf of a deceased homeowner. If

a homeowner files a Property Tax Credit Claim, but dies prior to April 1, 2020, the estate must withdraw the claim

using Form HS-122W. The estate is responsible to repay any credit issued. If the homeowner filed a Property Tax

Credit Claim between January and March 31 and dies after April 1, 2020, the commissioner may pay the credit to the

town on behalf of another member of the household with ownership interest.

An estate may continue classification of the property as a homestead until the following April provided the property

was the deceased homeowner’s homestead at the time of death and the property is not rented.

Delinquent Property Tax The 2020 property tax credit applies to the current year property tax. The municipality may use any

remaining credit towards penalty, interest, or prior year property taxes.

Nursing Home or Residential Care If the homeowner is age 62 or older and another owner who also lived in the homestead is the

homeowner’s spouse/civil union partner or sibling and has moved indefinitely from the homestead to a nursing home

or residential care facility, the homeowner makes the Property Tax Credit Claim with 100% ownership. This applies

only if the spouse/civil union partner or sibling does not make a Renter Rebate Claim or the spouse/civil union

partner or sibling does not make a Property Tax Credit Claim for the same homestead.

If the homeowner has moved to a nursing home or residential care facility, a Property Tax Credit Claim may be made

if there is a reasonable likelihood that the homeowner will be returning to the homestead and the homeowner does

not make a Renter Rebate Claim. The Department may ask for a doctor’s certificate to help determine whether the

nursing home or residential care facility is a temporary location.

2020 Form HS-122 Instructions

www.tax.vermont.gov Page 7 of 10

|

Enlarge image |

Renting at the End of the Year You may be eligible for a Renter Rebate Claim for rent paid in 2019 under the following

circumstances: 1)If you owned a Vermont homestead in 2019, 2) sold the homestead before April 1, 2019,

3) withdrew or did not file a 2019 Property Tax Credit Claim and 4) rented between the date of the sale and Dec. 31,

2019. To qualify for a renter rebate, your household income must be $47,000 or less. NOTE: This is the only

situation where a renter rebate can be claimed for fewer than 12 months.

OWNERSHIP SITUATIONS Page 8

Homeowner Age 62 or Older in 2019 If the homeowner shares ownership of the homestead with his or her descendant(s),

the homeowner may claim 100% ownership interest on the Property Tax Credit Claim, even if the other owners

(descendants) do not live in the homestead. The Department may request a letter of explanation.

Divorced or Legally Separated Joint Owners When the divorce decree or court order has declared a specific percentage of home

ownership for the purpose of property taxes, you must use that percentage if the following apply: 1) you are divorced

or legally separated from your spouse/civil union partner; 2) your name and the name of the spouse/civil union

partner from whom you are divorced or legally separated remain on the deed; and 3) you are awarded possession

of the home. If the divorce decree or court order does not specify responsibility for the property taxes, the person

residing in the homestead uses 50% ownership interest. The person not living in the homestead cannot make a

Property Tax Credit Claim.

The Department may ask for a copy of your court documents.

Duplex Housing Both owners occupy the building as their principal residence. The eligible housesite education property tax is the

tax on the portion owned by each homeowner. If the town issues a property tax bill to each homeowner for his or

her portion of the homestead, use the housesite value, housesite property tax, and 100% ownership interest. If the

property tax bill is for the total property, prorate the housesite value, housesite property tax, and ownership interest.

Only one owner occupies the building as his or her principal residence. The owner occupying the duplex as his or

her principal residence must prorate for the other owner’s interest.

Entity Ownership Property owned by a C or S corporation, partnership, or limited liability company cannot be claimed as an

individual’s homestead and is not eligible for property tax credit. The only exception is for a homestead located on

a farm. Read Reg. § 1.5401(7)-Homestead at www.tax.vermont.gov/regulations.

Life Estate A person who holds a life estate interest in a property that he or she occupies as a principal residence may make a

Property Tax Credit Claim as if the life estate holder was the owner of the property. The deed does not have to be

attached to the Property Tax Credit Claim but must be available for review upon Department request.

Trust Ownership A dwelling owned by a trust is not the homestead of the beneficiary unless the claimant is the sole beneficiary of

the trust and one of the following:

1. The claimant or the claimant’s spouse was the grantor of the trust, and the trust is revocable or became

irrevocable solely by reason of the grantor’s death;

OR

2. The claimant is the parent, grandparent, child, grandchild or sibling of the grantor; the claimant is mentally

disabled or severely physically disabled; and the grantor’s modified Adjusted Gross Income is included in

the household income calculation.

The term “sole beneficiary” is satisfied if the homeowner and the spouse/civil union partner are the only beneficiaries

of the trust. A property owned by an irrevocable trust cannot be a homestead except as stated in (1) above. The

trust document does not have to be attached to the Property Tax Credit Claim but must be available for review upon

Department request.

BUYING and SELLING PROPERTY

Buying after April 1, 2019 For property purchased as your principal residence, you need to file a 2020 Homestead Declaration. If

you are eligible to make a 2020 Property Tax Credit Claim and the property was declared as a homestead, use the

seller’s 2019/2020 property tax bill. If the property was not a homestead in 2019, ask the town for the housesite value

and the property taxes on the housesite as if it was a homestead in 2019.

Property Transactions after April 1, 2020 The property tax credit stays with the property. In the case of the sale or transfer of a

residence, any property tax credit amounts related to that residence shall be allocated to the seller at closing unless

the parties agree otherwise.

NEW CONSTRUCTION

New homestead construction that was built after April 1, 2019, and is owned and occupied as a principal residence

on April 1, 2020, must file Form HS-122 Homestead Declaration. Eligible homeowners may make a 2020 Property

Tax Credit Claim. The claim will be based on the value of the parcel as of April 1, 2019.

2020 Form HS-122 Instructions

www.tax.vermont.gov Page 8 of 10

|

Enlarge image |

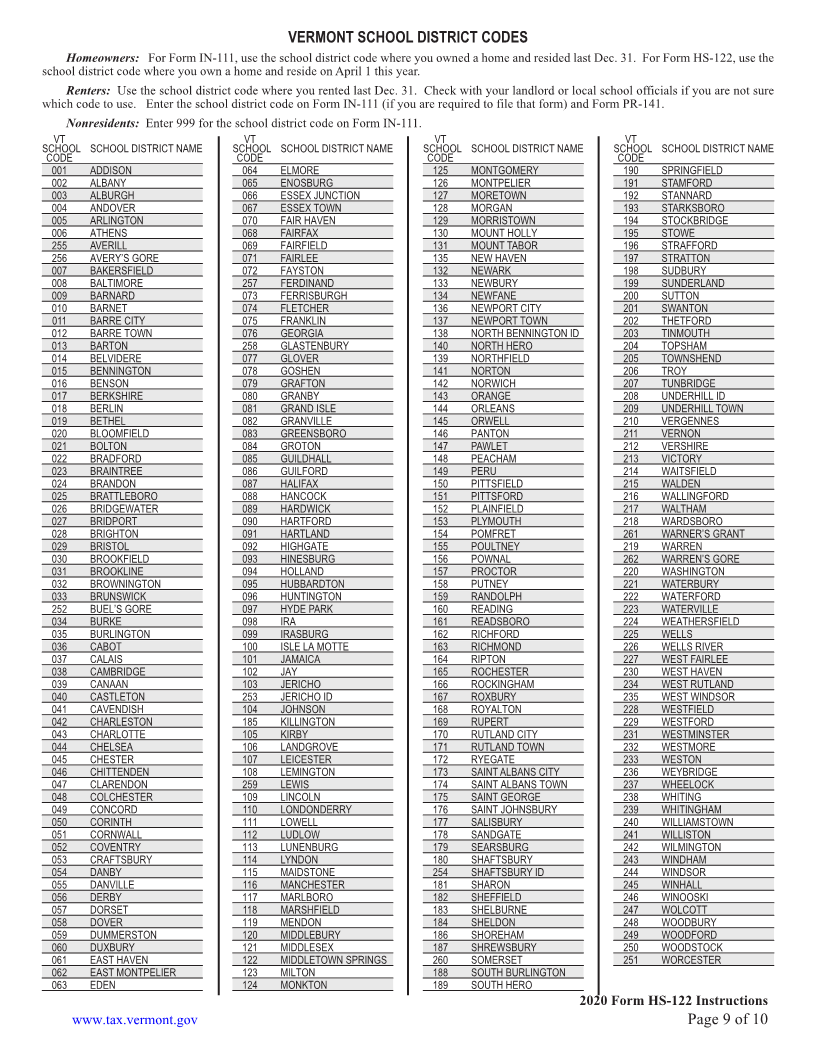

VERMONT SCHOOL DISTRICT CODES

Homeowners: For Form IN-111, use the school district code where you owned a home and resided last Dec. 31. For Form HS-122, use the

school district code where you own a home and reside on April 1 this year.

Renters: Use the school district code where you rented last Dec. 31. Check with your landlord or local school officials if you are not sure

which code to use. Enter the school district code on Form IN-111 (if you are required to file that form) and Form PR-141.

Nonresidents: Enter 999 for the school district code on Form IN-111. Page 9

VT VT VT VT

SCHOOL SCHOOL DISTRICT NAME SCHOOL SCHOOL DISTRICT NAME SCHOOL SCHOOL DISTRICT NAME SCHOOL SCHOOL DISTRICT NAME

CODE CODE CODE CODE

001 ADDISON 064 ELMORE 125 MONTGOMERY 190 SPRINGFIELD

002 ALBANY 065 ENOSBURG 126 MONTPELIER 191 STAMFORD

003 ALBURGH 066 ESSEX JUNCTION 127 MORETOWN 192 STANNARD

004 ANDOVER 067 ESSEX TOWN 128 MORGAN 193 STARKSBORO

005 ARLINGTON 070 FAIR HAVEN 129 MORRISTOWN 194 STOCKBRIDGE

006 ATHENS 068 FAIRFAX 130 MOUNT HOLLY 195 STOWE

255 AVERILL 069 FAIRFIELD 131 MOUNT TABOR 196 STRAFFORD

256 AVERY’S GORE 071 FAIRLEE 135 NEW HAVEN 197 STRATTON

007 BAKERSFIELD 072 FAYSTON 132 NEWARK 198 SUDBURY

008 BALTIMORE 257 FERDINAND 133 NEWBURY 199 SUNDERLAND

009 BARNARD 073 FERRISBURGH 134 NEWFANE 200 SUTTON

010 BARNET 074 FLETCHER 136 NEWPORT CITY 201 SWANTON

011 BARRE CITY 075 FRANKLIN 137 NEWPORT TOWN 202 THETFORD

012 BARRE TOWN 076 GEORGIA 138 NORTH BENNINGTON ID 203 TINMOUTH

013 BARTON 258 GLASTENBURY 140 NORTH HERO 204 TOPSHAM

014 BELVIDERE 077 GLOVER 139 NORTHFIELD 205 TOWNSHEND

015 BENNINGTON 078 GOSHEN 141 NORTON 206 TROY

016 BENSON 079 GRAFTON 142 NORWICH 207 TUNBRIDGE

017 BERKSHIRE 080 GRANBY 143 ORANGE 208 UNDERHILL ID

018 BERLIN 081 GRAND ISLE 144 ORLEANS 209 UNDERHILL TOWN

019 BETHEL 082 GRANVILLE 145 ORWELL 210 VERGENNES

020 BLOOMFIELD 083 GREENSBORO 146 PANTON 211 VERNON

021 BOLTON 084 GROTON 147 PAWLET 212 VERSHIRE

022 BRADFORD 085 GUILDHALL 148 PEACHAM 213 VICTORY

023 BRAINTREE 086 GUILFORD 149 PERU 214 WAITSFIELD

024 BRANDON 087 HALIFAX 150 PITTSFIELD 215 WALDEN

025 BRATTLEBORO 088 HANCOCK 151 PITTSFORD 216 WALLINGFORD

026 BRIDGEWATER 089 HARDWICK 152 PLAINFIELD 217 WALTHAM

027 BRIDPORT 090 HARTFORD 153 PLYMOUTH 218 WARDSBORO

028 BRIGHTON 091 HARTLAND 154 POMFRET 261 WARNER’S GRANT

029 BRISTOL 092 HIGHGATE 155 POULTNEY 219 WARREN

030 BROOKFIELD 093 HINESBURG 156 POWNAL 262 WARREN’S GORE

031 BROOKLINE 094 HOLLAND 157 PROCTOR 220 WASHINGTON

032 BROWNINGTON 095 HUBBARDTON 158 PUTNEY 221 WATERBURY

033 BRUNSWICK 096 HUNTINGTON 159 RANDOLPH 222 WATERFORD

252 BUEL’S GORE 097 HYDE PARK 160 READING 223 WATERVILLE

034 BURKE 098 IRA 161 READSBORO 224 WEATHERSFIELD

035 BURLINGTON 099 IRASBURG 162 RICHFORD 225 WELLS

036 CABOT 100 ISLE LA MOTTE 163 RICHMOND 226 WELLS RIVER

037 CALAIS 101 JAMAICA 164 RIPTON 227 WEST FAIRLEE

038 CAMBRIDGE 102 JAY 165 ROCHESTER 230 WEST HAVEN

039 CANAAN 103 JERICHO 166 ROCKINGHAM 234 WEST RUTLAND

040 CASTLETON 253 JERICHO ID 167 ROXBURY 235 WEST WINDSOR

041 CAVENDISH 104 JOHNSON 168 ROYALTON 228 WESTFIELD

042 CHARLESTON 185 KILLINGTON 169 RUPERT 229 WESTFORD

043 CHARLOTTE 105 KIRBY 170 RUTLAND CITY 231 WESTMINSTER

044 CHELSEA 106 LANDGROVE 171 RUTLAND TOWN 232 WESTMORE

045 CHESTER 107 LEICESTER 172 RYEGATE 233 WESTON

046 CHITTENDEN 108 LEMINGTON 173 SAINT ALBANS CITY 236 WEYBRIDGE

047 CLARENDON 259 LEWIS 174 SAINT ALBANS TOWN 237 WHEELOCK

048 COLCHESTER 109 LINCOLN 175 SAINT GEORGE 238 WHITING

049 CONCORD 110 LONDONDERRY 176 SAINT JOHNSBURY 239 WHITINGHAM

050 CORINTH 111 LOWELL 177 SALISBURY 240 WILLIAMSTOWN

051 CORNWALL 112 LUDLOW 178 SANDGATE 241 WILLISTON

052 COVENTRY 113 LUNENBURG 179 SEARSBURG 242 WILMINGTON

053 CRAFTSBURY 114 LYNDON 180 SHAFTSBURY 243 WINDHAM

054 DANBY 115 MAIDSTONE 254 SHAFTSBURY ID 244 WINDSOR

055 DANVILLE 116 MANCHESTER 181 SHARON 245 WINHALL

056 DERBY 117 MARLBORO 182 SHEFFIELD 246 WINOOSKI

057 DORSET 118 MARSHFIELD 183 SHELBURNE 247 WOLCOTT

058 DOVER 119 MENDON 184 SHELDON 248 WOODBURY

059 DUMMERSTON 120 MIDDLEBURY 186 SHOREHAM 249 WOODFORD

060 DUXBURY 121 MIDDLESEX 187 SHREWSBURY 250 WOODSTOCK

061 EAST HAVEN 122 MIDDLETOWN SPRINGS 260 SOMERSET 251 WORCESTER

062 EAST MONTPELIER 123 MILTON 188 SOUTH BURLINGTON

063 EDEN 124 MONKTON 189 SOUTH HERO

2020 Form HS-122 Instructions

www.tax.vermont.gov Page 9 of 10

|

Enlarge image |

Taxpayer Assistance

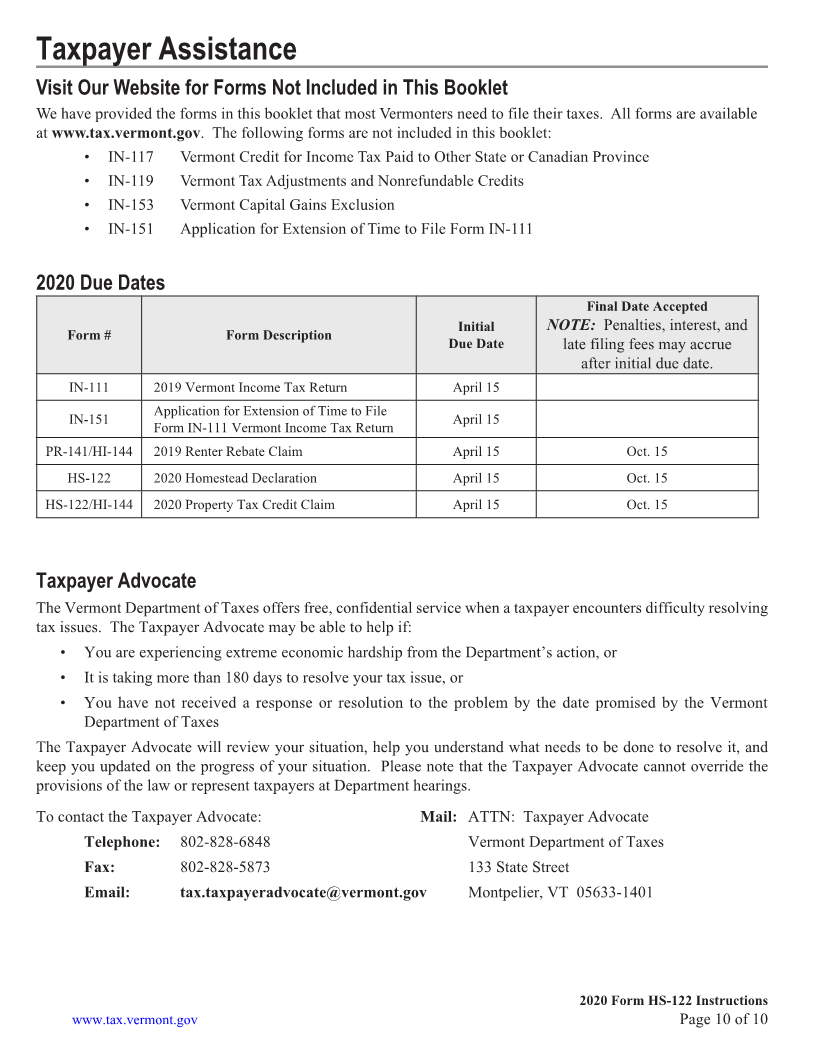

Visit Our Website for Forms Not Included in This Booklet

We have provided the forms in this booklet that most Vermonters need to file their taxes. All forms are available

Page 10

at www.tax.vermont.gov. The following forms are not included in this booklet:

• IN-117 Vermont Credit for Income Tax Paid to Other State or Canadian Province

• IN-119 Vermont Tax Adjustments and Nonrefundable Credits

• IN-153 Vermont Capital Gains Exclusion

• IN-151 Application for Extension of Time to File Form IN-111

2020 Due Dates

Final Date Accepted

Initial NOTE: Penalties, interest, and

Form # Form Description

Due Date late filing fees may accrue

after initial due date.

IN-111 2019 Vermont Income Tax Return April 15

Application for Extension of Time to File

IN-151 April 15

Form IN-111 Vermont Income Tax Return

PR-141/HI-144 2019 Renter Rebate Claim April 15 Oct. 15

HS-122 2020 Homestead Declaration April 15 Oct. 15

HS-122/HI-144 2020 Property Tax Credit Claim April 15 Oct. 15

Taxpayer Advocate

The Vermont Department of Taxes offers free, confidential service when a taxpayer encounters difficulty resolving

tax issues. The Taxpayer Advocate may be able to help if:

• You are experiencing extreme economic hardship from the Department’s action, or

• It is taking more than 180 days to resolve your tax issue, or

• You have not received a response or resolution to the problem by the date promised by the Vermont

Department of Taxes

The Taxpayer Advocate will review your situation, help you understand what needs to be done to resolve it, and

keep you updated on the progress of your situation. Please note that the Taxpayer Advocate cannot override the

provisions of the law or represent taxpayers at Department hearings.

To contact the Taxpayer Advocate: Mail: ATTN: Taxpayer Advocate

Telephone: 802-828-6848 Vermont Department of Taxes

Fax: 802-828-5873 133 State Street

Email: tax.taxpayeradvocate@vermont.gov Montpelier, VT 05633-1401

2020 Form HS-122 Instructions

www.tax.vermont.gov Page 10 of 10

|